Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

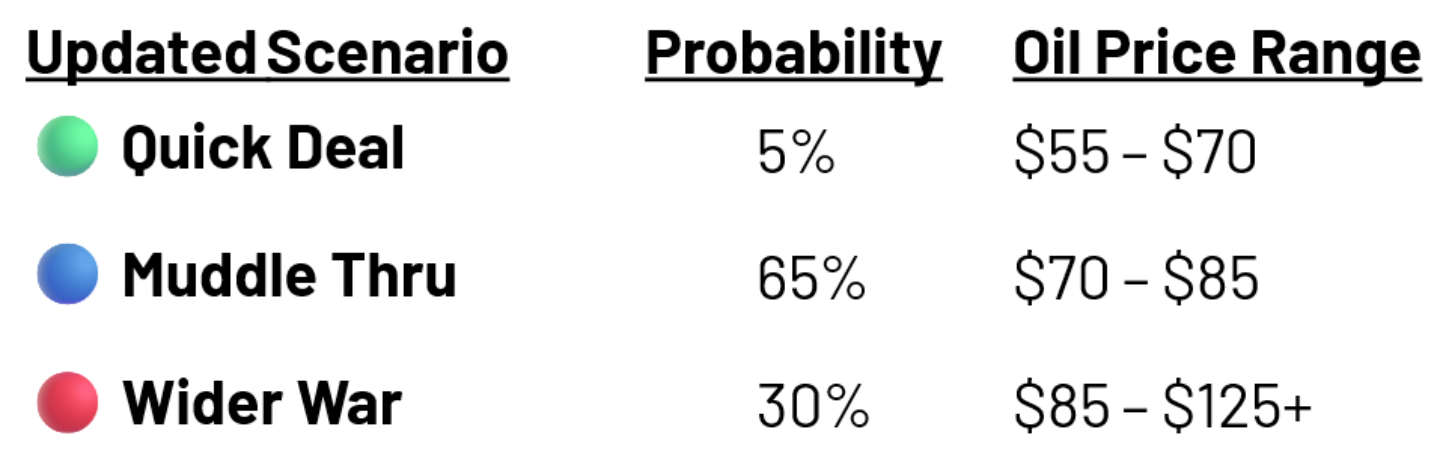

- We have revised down our probability of a ‘Quick Deal’ from our last publication.

- US economic and earnings data is still resilient, in our view.

- Risk management for our various portfolios is being dictated by the risk tolerance and time horizon of the strategy.

A couple of weeks ago, we published our Iran scenario analysis to dimension out war probabilities and their implications for markets and portfolio strategy. Today we update our views with new information gleaned since our last piece.

Oil May Take Longer to Normalize…But An ‘Off-Ramp’ Possible

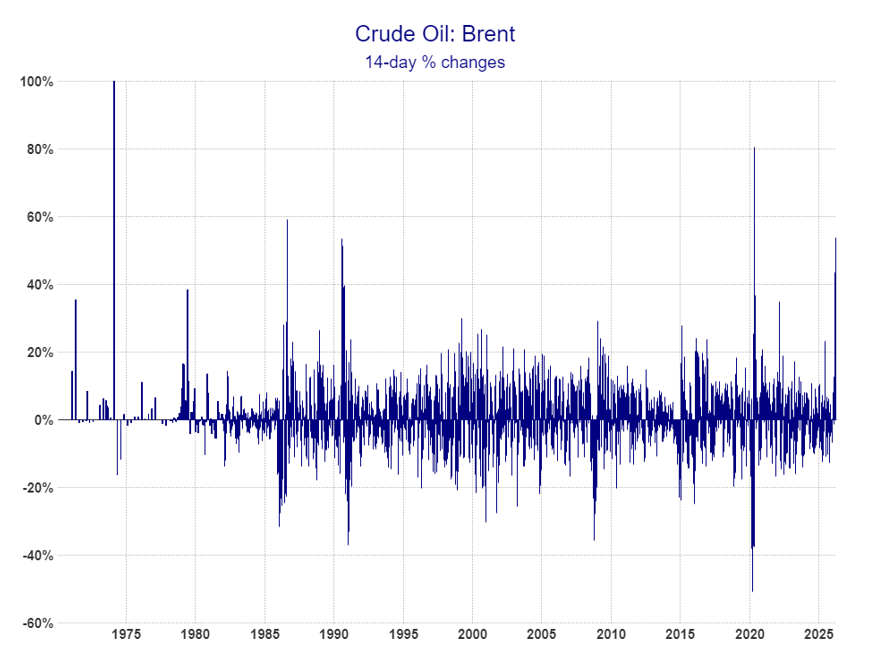

Oil prices have remained well above $100/barrel as the war has intensified. The ~54% trough-to-peak spike in Brent crude since late February is beginning to resemble past historic oil shocks (chart, right). Damage to neighboring nations' oil and gas facilities suggests energy supply normalization may take longer than expected even once the Strait of Hormuz is cleared. We have therefore reduced our 'Quick Deal' probability — characterized by oil quickly returning to the $55–70 range — from 10% to 5%, shifting that weighting into our 'Wider War' scenario, now at 30%.

That said, we are loath to rule out a 'Quick Deal' pivot (see Appendix at the end of this piece) over the next couple of months. In a midterm election year, committing ground troops is politically unpopular, as are inflation spikes — both increasing the potential for the Trump Administration to seek an 'off-ramp' before summer. This is why we have not dramatically altered our probabilities yet.

RiverFront Scenario Analysis Update For 3/20/26

Fed Action Complicated by War; Recession Still Unlikely for Now

The specter of war clearly hung over last week's Fed meeting. Despite one dissent, the Fed kept rates unchanged, citing solid growth and near-term inflation uncertainty. Fed funds futures now price in no cuts in 2026 — a notable shift from pre-conflict expectations. With Jerome Powell signaling he intends to serve until the government investigation concludes, a rate cut before the second half of 2026 seems unlikely.

All of these factors are complicating the forward view for economic growth and Fed action. However, with US GDP annualizing above 2%, solid PMI data, unemployment below 5%, and strong earnings momentum, we believe the US economy is well-positioned to weather a near-term energy spike. We view $100+ oil lasting six weeks or less as painful but manageable. If oil stayed at the high end of our ‘Wider War’ range for 2 months or more, we would likely raise our recession risk to significantly above 30%, in turn causing us to reevaluate our positive outlook on the US corporate earnings cycle - a major pillar of our constructive view of US stocks.

Beyond oil, the following would cause us to reconsider our sanguine stance: an Arab state attacking Iran, coordinated Iran-linked attacks on Western soil, or Russian and/or Chinese military intervention. As none of these 'gamechanger' events have occurred, we continue to view this episode as similar to past Middle Eastern conflicts, which have generally had only temporary effects on US stocks, as discussed two weeks ago.

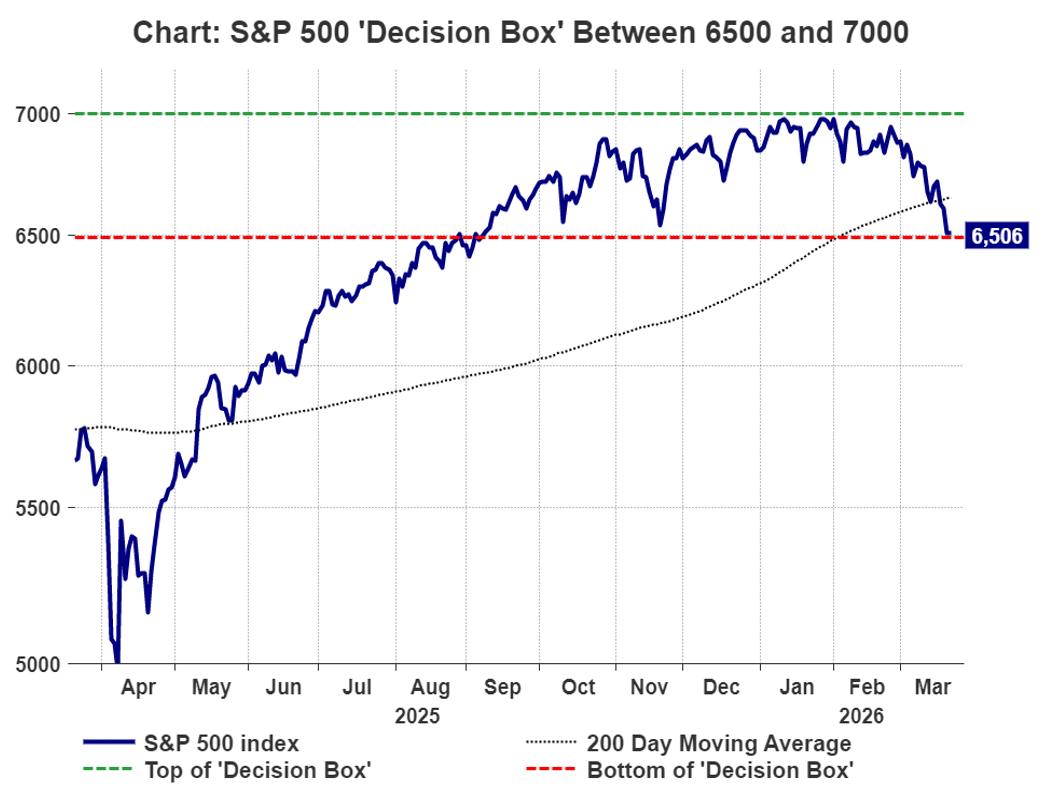

CHART: S&P 500 Pullback Nearing Support at Bottom End Of ‘Decision Box’

Two weeks ago, we suggested a ‘decision box’ was shaping up for the S&P 500 as investors placed probabilities on various war endgames. In a ‘Muddle Through’ scenario, we think the S&P 500 will generally remain within this ‘box’ between roughly 6500-7000. A ceasefire sometime between now and late spring could see a break to new highs, but in the ‘Wider War’ scenario, stocks could break down significantly through the bottom of the box. Our next key support level exists near the 23% retracement of the April 7th low at 6,490, where we have drawn the bottom of the decision box. A meaningful breach of the latter could potentially trigger a more significant asset reallocation in our lower-risk balanced portfolios.

Conclusion: A Pullback, Not A Contagion Yet

Our technical risk processes remain on alert, particularly for shorter-horizon portfolios (five-to-seven years and under), which tend to react more quickly to technical deterioration. These portfolios recently reduced equity exposure by roughly 7%, trimming individual US stock holdings that had grown large during the multi-year rally. Longer-horizon portfolios are less likely to react to geopolitics unless we see meaningful fundamental deterioration. All balanced portfolios remain overweight equities, though shorter-horizon portfolios are now much closer to neutral.

We are watching events in the Middle East with humility and intellectual flexibility — geopolitics can change on a dime. It's easy to forget that volatility, while unpleasant, is consistent with midterm years and Fed Chair transition periods. The current -7% S&P 500 pullback is worth contextualizing: periodic 5–10% pullbacks are common in cyclical bull markets, often acting as a 'pressure release valve' that resets expectations. Sentiment — as measured by the NDR Daily Crowd Sentiment poll and net flows into US equity ETFs — is approaching extreme pessimism, though we do not believe we have seen a tradable level of capitulation yet. Our risk management triggers remain on high alert, but our portfolio team is also sizing up potential additions to equity themes we will want to add to when this conflict shows signs of resolution.

APPENDIX - DESCRIPTIONS OF RIVERFRONT’S THREE IRAN WAR SCENARIOS

🟢‘QUICK CEASEFIRE/DEAL’: Less Likely

- Definition: Short duration war, opening of Strait of Hormuz, no OPEC production loss, regime change friendly to US and accepted by Iranian people

- Eventual Oil Range: $55-70

- Inflation: Lower

- Fed Action: >2 cuts in ‘26

- Favored Assets: International, US Tech, longer-duration fixed income

🔵‘MUDDLE THRU’: More Than Likely

- Definition: 100-120 day duration air war; largely contained to Iran

- Eventual Oil Range: $70-85

- Inflation: Stable, after initial spike

- Fed Action: At least 1 cut in ‘26

- Favored Assets: US stocks, cyclicals, covered calls

🔴‘WIDER WAR’: Unlikely, but Taking It Seriously

- Definition: Strait of Hormuz remains effectively closed, other Middle Eastern countries joining the fray, US ground troop commitment, conflict goes global (China or Russia commit to supporting Iran)

- Eventual Oil Range: $85-125+

- Inflation: Significantly higher

- Fed action: No cuts in ‘26; possible hike in ‘27

- Favored Assets: Cash and T-bills, commodity-related instruments, covered calls

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 03.23.2026 | Weekly View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist