Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Important Information about RiverFront’s Placement of Wrap Fee Account Client Trade Orders and Our “Trade Away” Practices

July 9, 2026

The following disclosure is published in an effort to provide RiverFront wrap fee account clients with more information regarding our trading practices, specifically the use of trade away transactions (as described below) and certain costs relevant to these practices. It is not a comprehensive description of all RiverFront trading policies and procedures. Additional information and disclosures are available in our Form ADV Part 2A.

RiverFront offers asset allocation portfolios for a range of investment objectives and risk tolerances that can be bought through wrap fee programs at dually registered brokerage and investment advisory firms (referred to throughout this document as “Sponsor Firms”). RiverFront has trading discretion over these asset allocation portfolios if they are purchased as separately managed accounts (“SMAs”); RiverFront does not have trading discretion over portfolios purchased in unified managed accounts (“UMAs”) and model delivery programs (“MDPs”). The information below pertains only to SMA wrap fee clients that have granted RiverFront trading discretion over their account(s).

Presently, “Maintenance Trades,” which we define as trading that result from new accounts, liquidations, cash/security addition or withdrawals, tax harvesting, or any other client-requested transactions, are typically processed through the client’s Sponsor Firm’s managed-money desk. Portfolio management-driven model changes (across-the-board or “ATB” trades) are typically aggregated and submitted via a block trade to a third-party brokerage firm in order to seek best execution (a “Trade Away Transaction”). RiverFront does not currently execute Trade Away Transactions with its Sponsor Firms.

We have determined that best execution on our ATB trades is generally achieved through Trade Away Transactions, even though our SMA clients will incur additional brokerage costs related to the Trade Away Transactions (see the table below for additional information on these costs). While the Sponsor Firms’ managed money desks have proven very capable, we often have complicated execution strategies that require greater timing flexibility, or in the case of exchange-traded products (“ETPs”), which include both exchange-traded funds and exchange-traded notes that demand direct access to an authorized participant for a single block execution. Based on our trading experience, trading away has many advantages, including, without limitation, eliminating price dispersion, limits exposure to information leakage and high frequency traders, and allows us to be more nimble in our trading, thereby avoiding potential delay costs.

We have considered executing these ATB transactions via a trade rotation among the Sponsor Firms; however, based on our trading experience and analysis, we currently believe that trading away enables us to achieve best execution for our clients. RiverFront’s Brokerage Committee will continue to periodically evaluate our trade execution strategy in order to ensure that we continue to provide best execution for our clients.

We have considered executing these ATB transactions via a trade rotation among the Sponsor Firms; however, based on our trading experience and analysis, we currently believe that trading away enables us to achieve best execution for our clients. RiverFront’s Brokerage Committee will continue to periodically evaluate our trade execution strategy in order to ensure that we continue to provide best execution for our clients.

By trading away our ATB trades, we believe that we can obtain best execution for our clients and decrease price dispersion across different Sponsor Firms. Furthermore, we have been able to identify other avenues of liquidity away from our Sponsor Firm managed money desks. For example, we have the ability to anonymously source multiple bids and offers from dealers for ETPs. We can also use a variety of algorithms to optimize each unique trading objective. Finally, for ETP securities that may appear to less liquid, we can use brokers that are able to source liquidity in an alternative manner to minimize price impact and ensure execution near the ETP’s net asset value (“NAV”). We regard the ability to create and redeem the ETP basket as a critical requirement to achieve our best-execution requirements.

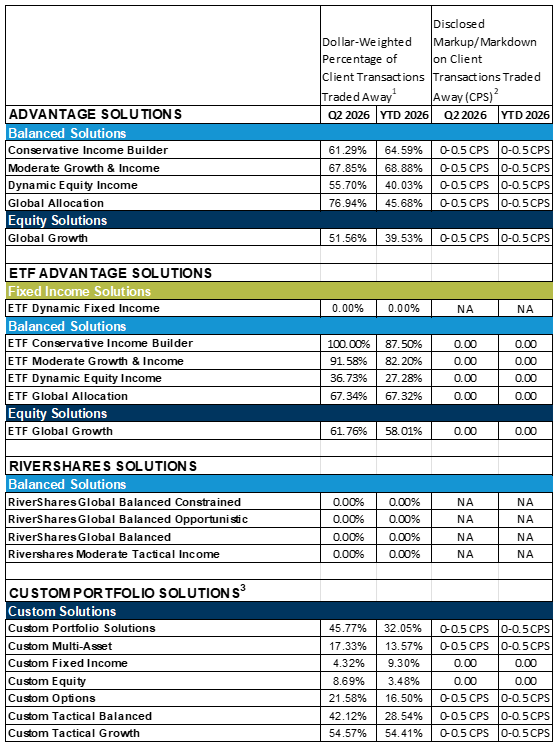

For the reasons stated above, RiverFront has determined that best execution should be achieved differently for ATB trades than for Maintenance Trades. RiverFront believes that ATB trades are in most cases better executed through Trade Away Transactions, while Maintenance Trades are usually better executed through the clients’ Sponsor Firms. The chart below provides the volume of wrap fee trades by market value executed via Trade Away Transactions, and the average disclosed markup/markdown on client transactions traded away which are costs charged by non-designated broker dealers that are netted into the price of the security and passed onto wrap fee clients as a result of these trades (see the chart below and footnote no. 2 for more information). This information is provided for each RiverFront investment strategy available to wrap fee clients.

We have disclosed these trading practices in our Form ADV Part 2A, which is provided to clients upon opening a RiverFront account and, at a minimum, offered annually thereafter. Our Form ADV Part 1A and Part 2A is also publicly available at: https://www.adviserinfo.sec.gov/. Please contact RiverFront at 804-549-4800 and/or [email protected] if you would like a copy of our most recent Form ADV Part 2A sent to you or if you have any questions regarding our trading practices.

Wrap Fee Program Trade Away Transaction Information 2026

1. All percentages are approximate. For purposes of this calculation, we divided (a) the total dollar amount of wrap fee client transactions (including all stock, bond and ETP transactions) in securities that were placed with broker-dealers other than the clients’ Sponsor Firms (Trade Away Transactions) by (b) the total dollar amount of wrap fee client transactions (including all stock, bond and ETP transactions) that RiverFront placed with all broker-dealers, in each case during the relevant period. For example, assume RiverFront placed a total of 1,000 transactions for wrap fee clients during Q1, having an aggregate dollar amount of $1,000,000. Of that total, RiverFront placed 700 of those transactions with broker-dealers that were not the clients’ Sponsor Firms (Trade Away Transactions), and the aggregate dollar value of those 700 transactions was $850,000. Thus, in this example, the percentage dollar amount of trades in securities traded away in Q1 would be reflected as 85% ($850,000/$1,000,000).

2. For many, if not all Trade Away Transactions, there will likely be no disclosed markup/markdown. In these instances, the undisclosed markup or markdown is netted into the price the client receives. Since the executing broker does not provide data to us regarding the dollar amount of the markup or markdown in these instances, we cannot disclose an amount to the client, and will list “0” in this column until such time as we are able to provide additional information, if any. These types of trades include, but are not limited to, transactions in shares of ETPs in which an Authorized Participant or market maker is providing RiverFront with a two-sided market for execution. Once a trade is complete, however, we will send a written request to the executing broker to confirm, in writing, trade information, including markup/markdowns. To the best of our ability, therefore, we will seek to obtain and provide to clients the markup/markdowns disclosed to us from the executing broker, either through trade confirmations or in other written form.

3.Certain Custom Portfolio Solutions are not managed to a specific RiverFront investment model, but rather are based on specific client instructions. Please see our ADV 2A for more information on these accounts.