Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Summary

- Our ‘Intrinsic Value’ framework helps us to avoid overpaying for growth or falling into value traps.

- In the AI trade, price appreciation has outrun earnings for some names — and lagged badly for others.

- While prices for recent IPOs are likely too high, there remain buying opportunities in AI-related stocks, in our view.

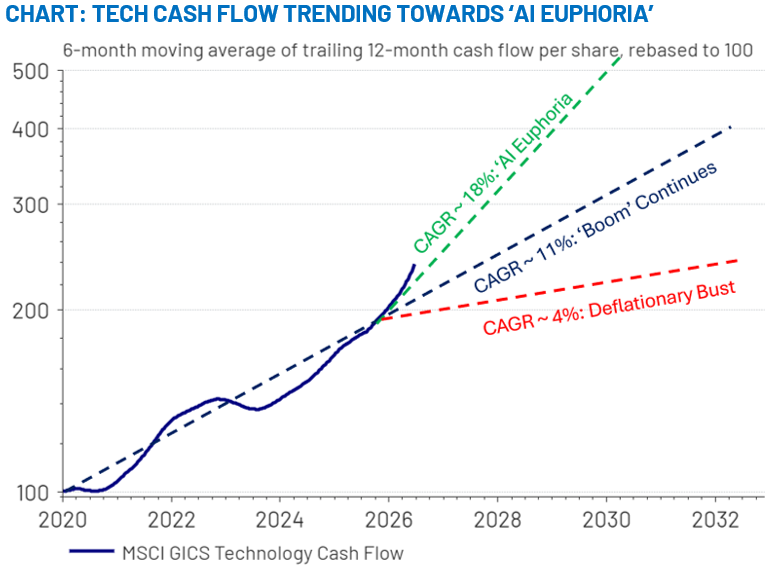

After a wild last 12 months in a technology stock boom - and more recent volatility - the question du jour, in our view, is not whether AI is transformative. The significant increases in economic productivity and huge corporate cash flows generated by AI-related hardware companies confirm this, as both have accelerated since the release of Chat-GPT in late 2022. Across the Technology sector, we are seeing the most optimistic cash flow outcome from our 2026 Outlook come to pass so far this year.

So, the question, at least for now, is not whether there will be big earnings growth – there already is, and we are trending towards “AI Euphoria”. The more important question for investors now is whether all these positive fundamentals and future earnings have already been fully priced into the return.

We approach investment questions like these using a framework we call ‘Intrinsic Value’. Looking at the AI trade through this lens, we see five themes, each with very different earnings trajectories and current valuations. Sorting through it all, we see opportunities in a number of segments – hyperscalers, some semiconductors, and industrial components all seem to have enough upside if the earnings materialize as we expect. However, AI model providers and some of the recent high-profile stock offerings in AI-related names have prices that far exceed realistic growth scenarios, in our view. This week we are diving deep into our Intrinsic Value framework to divine what it is telling us about some of the major themes in the market right now.

Intrinsic Value: A Framework to Avoid Overpaying for Growth…and to Avoid Value Traps

We believe that a traditional ‘value’ discipline – simply looking at relative valuation multiples in isolation- can underestimate the future earnings power demonstrated in an established growth theme like AI. We also know that a pure ‘growth’ mindset – assuming the current momentum will persist without any regard to valuation - could leave us overpaying for strong earnings that, even if realized, were already reflected in the current prices.

Our preferred method, therefore, is our Intrinsic Value process - our best estimate of what a company is worth today, based on its likely future earnings trajectory. We formulate our view of Intrinsic Value in four steps in order to decide whether to add to a position, hold and monitor, or trim and exit.

- Assess the Macro Backdrop: Interest rates, credit availability, fiscal policy, and the economic growth backdrop help determine what any company can realistically earn, and what multiple the market may pay for it.

- Analyze the Competitive Framework: This involves assessing durable earnings quality, capital allocation decisions, and competitive threats in order to determine the level of profitability achievable for the company.

- Project Earnings and Identify Catalysts: This consists of identifying the precise growth driver(s) for your thesis, as well as the evidence that would prove it wrong. If the thesis cannot be validated in earnings or corroborated by analysts, it is a hope, not a thesis.

- Assess Valuation Relative to Earnings: Does today’s price already reflect the earnings scenario? If not, it may be a buying opportunity. If fully reflected, hold and monitor the position. If the price implies more than the scenario can deliver, trim or exit. A theme can be fundamentally intact, and the stock can still have appreciated too much. Walking away from a party still going strong is the hardest call in active management…this framework helps give us the discipline to do that.

Applying the Framework to Five Themes Within One Overarching ‘AI’ Trade

We are focused on five key themes (listed and summarized below) within the AI ecosystem. The macro environment is favorable for all the themes, so the table lays out the case for each of the other parts of our Intrinsic Value framework. We are generally seeking opportunities where valuations are not elevated, and our view of earnings is more positive than the markets.

Theme 1: AI Model Providers: Great Companies, Wrong Price. Many of the recent high-profile listings and outsized market movers carry compelling narratives but less clear earnings history. They have either been the companies that are the primary engines of AI (such as Anthropic or OpenAI), or quick adopters that have gone ‘all in’ on AI (like Palantir and SpaceX). Price discovery is at the mercy of sentiment, as the earnings and growth rates necessary to justify the valuations will take years or even a decade to materialize. The opportunity cost of not owning them as benchmarks reprice upward is real — as is the absolute downside when sentiment shifts. We will lean on intrinsic value to signal when to leave the party.

Theme 2: Hyperscalers and Semiconductors: The Sweet Spot for Stock Pickers. Hyperscalers and semiconductors have delivered revenue growth and consistently strong earnings guidance. We see this segment as having the most durable earnings, making many of them still attractive, in our view. However, this is precisely where complacency becomes a risk. There are many semiconductors and hyperscalers whose price appreciation has recently begun to outrun the pace of their earnings growth. We also have seen companies in this space experience significant price slowdowns even as their earnings have continued to come through. So, while we consider this sector to be a sweet spot for investors, we caveat that with the understanding that security selection will become increasingly important as the AI Trade unfolds. We think there are some companies in this theme that might not ultimately have the capital discipline to earn profits sustainably, and others where the prices simply outgrow the earnings. We also expect there to be a lot of volatility in this theme – even if earnings ultimately come through, we think the market will express its views on these companies through rapid multiple compression and expansion along the way. We will be sizing up our positions as best we can to accommodate this volatility.

Theme 3: AI Physical Infrastructure: Still Attractive. Industrial components, utilities, and power infrastructure are the physical backbone of the AI buildout, providing the grid capacity, cooling systems, and equipment that data centers require. Valuations are elevated but not extreme, especially with supply constraints being structural. The earnings case is visible and tangible, not narrative-driven. You cannot add power generation or transmission capacity overnight, and the demand signal from hyperscalers is locked in for years. Key risks are a sudden capex pivot by the hyperscalers, a faster-than-expected easing of supply constraints, or an unforeseen regulatory backlash on AI or on the power usage itself. This theme is directly exposed to macro credit and rate shocks as well as sentiment shifts, making stock selection and position sizing especially important.

Theme 4: Early Disrupted Industries: The Hidden Opportunity (and Risk) in Software. Since we wrote our original piece, companies that have been threatened existentially by AI have emerged as a distinct category. The first industry to acutely feel this pressure is Software companies, and they have been broadly de-rated on AI disruption fears. What the 'dot-com' era taught us is that many of the businesses targeted for extinction successfully incorporated the Internet as a core part of their model. Many of the Software companies in the cross hairs today are embedding AI into durable models with proven revenue and customer relationships a new entrant cannot easily replicate. A lot of the “AI Hype” in our minds is the underestimation of the complexity of enterprise software. This leads us to believe that the disruption thesis is overpriced. Neither analyst earnings estimates nor management guidance have confirmed a slowdown in earnings. Our watch signal will be a broad decline in earnings expectations, or a pattern of earnings misses and weakening guidance.

Theme 5: Early Non-Technology Enterprise Adopters. Industrial, healthcare, and consumer companies using AI to expand margins, cut costs, or accelerate revenue represent the next potential wave as the earnings impact could be significant. While some anecdotes exist, the aggregate earnings data has not confirmed it. Broad margin expansion has not yet manifested itself, and our general view is that layoffs attributed to AI could be related to post-COVID over hiring. If the data confirms the trend or the narrative shifts, the entry point could prove attractive.

Conclusion: Key Takeaways

- Intrinsic value is not a one-time screen. It is an ongoing assessment of price against realistic earnings potential. This provides the most important edge an active manager can apply when enthusiasm and macro risk are rising together.

- The AI trade is not monolithic. Some names, including recent high-profile listings, are running on an optimistic narrative with no earnings anchor. Others have genuinely grown into their premium valuations, while others still have arguably been overly punished for expected future earnings issues that have yet to manifest. Knowing the difference is the entire game.

- Software incumbents are our most intriguing opportunity. The market has priced in disruption that the earnings data has not confirmed. That gap between narrative and reality is where patient capital finds its return opportunities.

- We will be wrong about parts of this. A macro shift, earnings miss, a competitive threat moving faster than expected: any of these can upend a well-founded thesis. The framework does not eliminate errors in judgment, but it does clarify their source. It forces us to define in advance what evidence would change our mind and to act on it.

- Active management means freedom to rotate between growth and value, into defensive instruments, or into lower-risk asset classes when the environment deteriorates. As AI names grow in benchmark weight, passive investors absorb concentration without choosing to. Intrinsic value provides the signal to act.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 06.30.2026 | Strategic View

Authored by

-

Adam Grossman CFA®

Global Equity CIO | Partner