Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Summary

- Declining money market yields make sitting in cash increasingly costly.

- Treasuries offer attractive real yields and lower volatility than equities.

- Strong equity gains create an opportunity to rebalance into bonds.

Now that the book has been closed on the first half of 2026 - a period propelled by the AI-driven technology trade - investors are searching for what to do next. For those investors that have ridden the stock market up to near all-time highs, they may be thinking about reducing their equity exposure and adding fixed income to their portfolio. Others that have sat paralyzed on the sidelines, looking for the right time to enter the market, may simply want their money to work for them. We will walk through how both types of investors should view bonds moving forward.

Investors Sitting in Cash are Facing Declining Money Market Rates

For the investor that has been sitting in cash, the last few years have been manageable due to money market funds paying competitive rates. Prior to 2022, money market rates were pinned near zero, so there was an incentive for investors to allocate to equities. Post-2022, after interest rates moved higher, some conservative investors sold stocks and retreated to the sidelines as they were able to receive yields just above 5% in money market funds. However, since peaking in 2023, money market fund yields have steadily declined… and currently are just below 3.50%. Investors that choose to stay in cash will face further reinvestment risk if money market yields continue to decline.

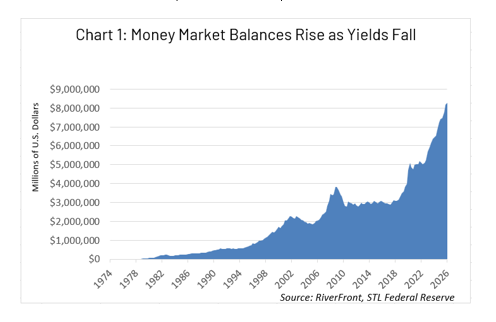

According to the St. Louis Federal Reserve Bank, at the end of Q1 there was over $8.2 trillion held in money market funds, as shown in Chart 1. The steady decline in money market yields should be a call to action for investors sitting in cash and cash equivalents, in our opinion.

From our perspective, despite the Fed currently taking a ‘hawkish’ tone to fight inflation, we do not believe that they will hike interest rates in 2026. The upward movement of yields since the beginning of the Iran War has tightened financial conditions for all bond maturities from two to thirty years (the yield curve). For conservative investors that are in cash and cash equivalents, the focus should be on the front-end of the yield curve, as it is more sensitive to changes in monetary policy that impact money market fund rates.

Currently, the 2-year Treasury is yielding 4.21%, which is 0.83% higher than where it was at the end of February… while money market yields have only fallen further. By investing in short-term bonds, investors that have been risk-adverse can gradually re-enter the market without meaningfully changing their risk profile.

Equity Rally Did Heavy Lifting; Now Fixed Income Can Help Ease the Load

Reflecting on our 2026 Outlook entitled Riding the Wave: The Anatomy of Booms & Bubbles, our base case forecast for the year was for the S&P 500 to return between 8 and 12%, and the 10-year Treasury to yield 4.20%. Through the first half of the year, the S&P 500 returned just over 10% and the 10-year Treasury was yielding 4.47%. Therefore, while the equity market is on pace to exceed our base case forecast, treasuries have underachieved…leaving potentially some room for capital appreciation in the 2nd half of the year should risk appetite decrease. In our view, the 10-year Treasury is giving investors a better opportunity to enhance the total return in a balanced portfolio due to higher yields and a lower volatility profile than its equity alternatives.

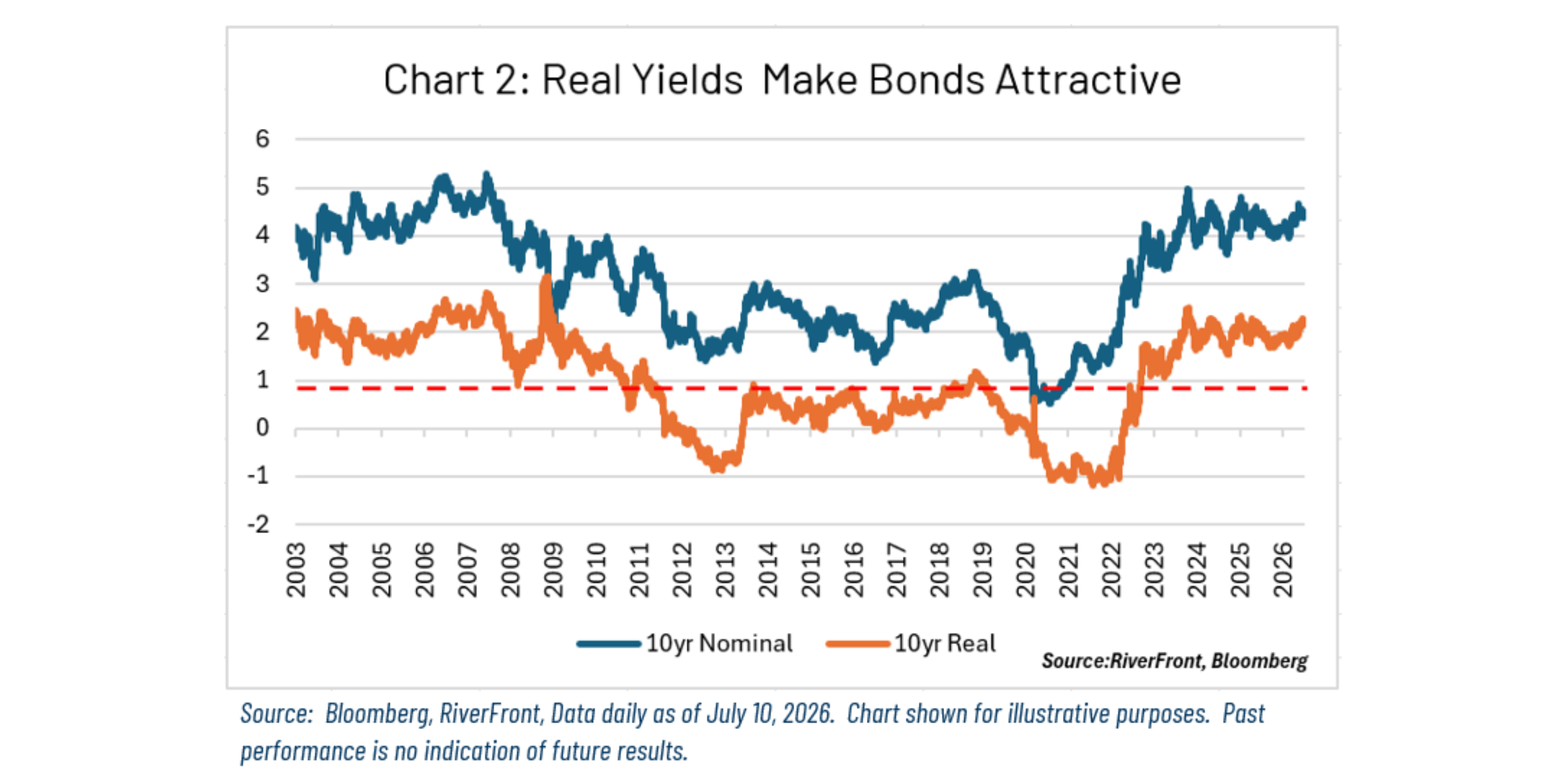

As we wrote in our fixed income-focused Weekly View in May, we believe that fair value on the 10-year Treasury is around 4.3%, making investing at higher yields attractive. Additionally, real’ yields (yields adjusted for inflation) remain above 2%, after averaging nearly 1% over the last 23 years (Chart 2, right). Given that equities did a lot of heavy lifting in the first half of the year, it would make sense that balanced investors that have ‘ridden the wave’ in stocks would consider reducing their equity exposure to dial down the level of risk in their portfolios. Furthermore, these investors can move up in priority in the capital structure as they shift from stocks to bonds, as interest payments will be prioritized over dividends or stock buybacks if the economic circumstances deteriorate.

Conclusion: Why We're Looking to Add Bonds Here

Bonds offer value on two fronts: they can help de-risk balanced portfolios after a strong first-half equity rally, and they provide a compelling alternative for investors still parked in cash. Whether viewed through the lens of ETFs or individual bonds, we believe the asset class is attractive — particularly the short end of the yield curve, where 1-to-5-year Treasuries yield between 4% and 4.30%. Investors willing to take on credit risk can pick up an additional 0.50% by moving into corporate bonds. We would avoid longer maturities at this time, given inflationary pressures from higher oil prices driven by the Middle East conflict. That said, if the 10-year Treasury rises above 4.75%, we would view that as a buying opportunity. As we are income. As we are currently underweight fixed income, we are actively looking for opportunities in our shorter-horizon portfolios to add bond exposure and enhance income generation.Download 07.14.2026 | Weekly View

Authored by

-

Kevin Nicholson CFA®

Global Fixed Income CIO | Partner