Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- Duration and magnitude of the oil shock will determine the severity of the economic fallout.

- The US economy is better prepared for uncertainty than many realize, and earnings continue to impress.

- Inflation bears watching going forward, but is less threatening than feared.

As we outlined last week, a quick and tidy conclusion to the war in Iran looks increasingly unlikely — which means markets are likely to remain volatile for the foreseeable future. What matters most is the magnitude and duration of the global oil price spike – currently around $112/barrel. Econometric analyses from Goldman Sachs, Moody's, and others place the 'danger zone' somewhere above $125/barrel sustained for more than a month or two.

Since the primary driver of oil prices — transit availability through the Strait of Hormuz — is largely outside investors' control, markets will naturally tend to assume the worst. Respecting the ‘message of markets’, we have reduced equity exposure in our shorter-horizon portfolios. Our risk processes remain on high alert in these portfolios, particularly after the S&P 500 violated the lower end of our 'decision box' near 6,500 late last week.

Amid the media war blitz, however, one key point is being obscured: the US is entering this period of uncertainty in a uniquely solid position — both in absolute terms and relative to Europe and Asia. We urge investors to exercise caution before concluding that the war's fallout will inevitably spell the end of the US economic cycle.

Recession Risk Appears Low — Many Have Underestimated US Resilience

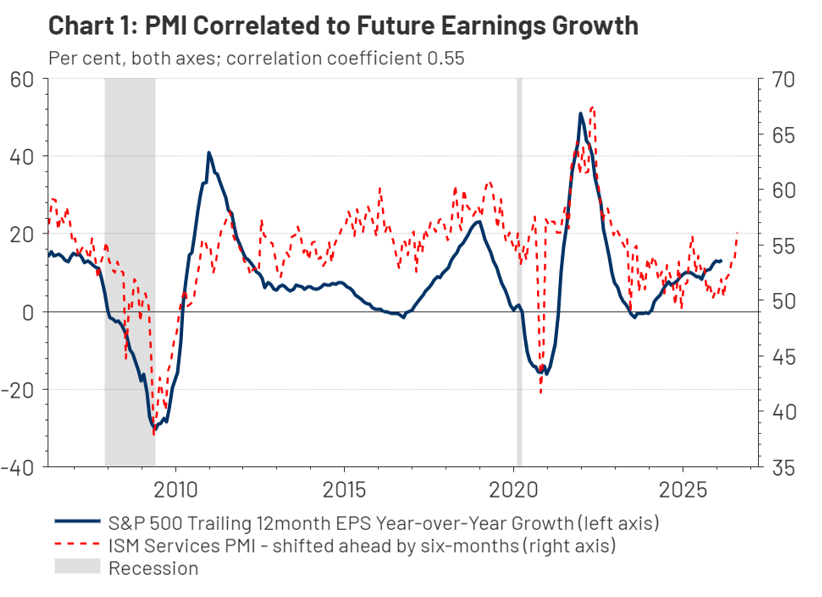

We track a broad range of US recession indicators — both proprietary and from organizations like the Conference Board and NDR Research — spanning credit conditions, money supply, consumer and CEO confidence, housing starts, unemployment, financial conditions, and PMI surveys (Chart 1, below). Very few, if any, are signaling high recession risk, in stark contrast to some economists' 40–50% probability estimates over the next 12 months.

While we recognize that early war effects may not yet be showing up in the data, we would remind investors that traditional economists have consistently underestimated US economic resilience over the last decade. COVID-19, the Ukraine War, and last year's 'Tariff Tantrum' all come to mind. This resilience is structural, and partly rooted in the US' energy independence and its economy's declining energy intensity: our modern economy runs on less oil per dollar of GDP than in decades past.

US Corporate Earnings Continue to Strengthen

US corporate earnings remain a bright spot. Earnings estimates over the next 12 months were revised up another $5 over the past two weeks to $330 — suggesting over 20% year-over-year growth, even against the backdrop of the Iran war. S&P 500 aggregate earnings for Q4 came in 6.8% above analyst expectations, with only the utilities sector missing. Technology earnings were even stronger, surpassing expectations by 7.6%. Referring back to the PMI data above, the ISM Services PMI (red dotted line, Chart 1, above) tends to have a high positive correlation to future S&P 500 earnings over the succeeding six months (solid blue line). The recent strength in PMI portends well for earnings going forward, in our view.

Inflation — A Growing Problem, But Wage Pressures Offer Some Mitigation

In our view, the oil price shock's impact on inflation is perhaps the biggest issue facing US stock and bond investors, given interest rates' effect on both asset classes. This is further complicated by uncertainty around the Fed transition from outgoing Chair Jay Powell to incoming nominee Kevin Warsh. Higher rates are particularly problematic for smaller companies' creditworthiness and for the growth equity valuations that dominate US large-cap indices — as well as for the bond market broadly.

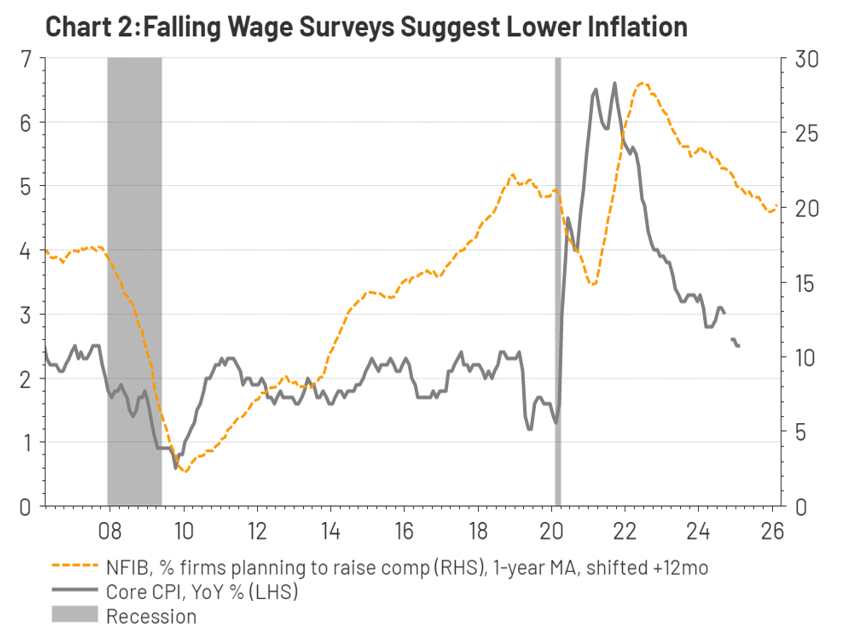

That said, another 'forest through the trees' point: oil's direct impact on consumer inflation is considerably lower than it once was. According to a recent Goldman Sachs sensitivity analysis, every 10% rise in oil prices only contributes about 0.04% rise in core PCE inflation - the Fed’s preferred metric. And the growing anxiety around AI-driven job displacement appears to be dampening upward wage pressure — historically one of the most persistent channels through which inflation works its way into Corporate America's cost structure. According to our analysis, wage gain surveys have tended to have high correlation to core CPI inflation readings over the subsequent year, (see Chart 2, above).

Conclusion: US Economy Entering into War Uncertainty in Solid Shape

The noise surrounding the Iran conflict is loud, but investors should resist the urge to extrapolate near-term market volatility into a broader economic collapse. We believe the US economy is fundamentally well-positioned: recession indicators remain subdued, corporate earnings continue to impress, and structural factors — from energy independence to moderating wage pressures — provide meaningful buffers against the current shock. We are not dismissing the risks; our recent risk reductions in our shorter-horizon portfolios reflect that vigilance. None the less we are equally committed to seeing the forest through the trees — and right now, that forest looks healthier than the headlines suggest.

APPENDIX - DESCRIPTIONS OF RIVERFRONT’S THREE IRAN WAR SCENARIOS

🟢‘QUICK CEASEFIRE/DEAL’: Less Likely

- Definition: Short duration war, opening of Strait of Hormuz, no OPEC production loss, regime change friendly to US and accepted by Iranian people

- Eventual Oil Range: $55-70

- Inflation: Lower

- Fed Action: >2 cuts in ‘26

- Favored Assets: International, US Tech, longer-duration fixed income

🔵‘MUDDLE THRU’: More Than Likely

- Definition: 100-120 day duration air war; largely contained to Iran

- Eventual Oil Range: $70-85

- Inflation: Stable, after initial spike

- Fed Action: At least 1 cut in ‘26

- Favored Assets: US stocks, cyclicals, covered calls

🔴‘WIDER WAR’: Unlikely, but Taking It Seriously

- Definition: Strait of Hormuz remains effectively closed, other Middle Eastern countries joining the fray, US ground troop commitment, conflict goes global (China or Russia commit to supporting Iran)

- Eventual Oil Range: $85-125+

- Inflation: Significantly higher

- Fed action: No cuts in ‘26; possible hike in ‘27

- Favored Assets: Cash and T-bills, commodity-related instruments, covered calls

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 03.31.2026 | Weekly View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist