Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Summary

- Technology drove strong US returns.

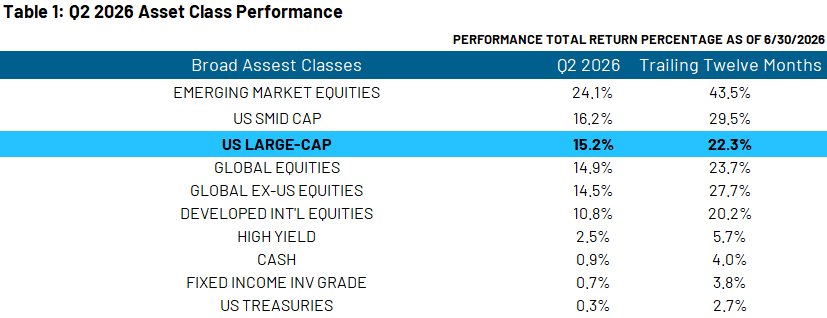

- Emerging Markets lead global returns, despite negative Chinese returns.

- Strong earnings have allowed market to climb the “wall of worry”.

In financial markets, there is a concept known as “the wall of worry.” Put plainly, this concept describes how markets often see past short-term concerns to post positive returns, essentially climbing over the proverbial wall of worry. The second quarter was a great demonstration of this concept, as geopolitical and global macro concerns were not enough to stop global stocks from rebounding and posting strong returns. This rally has gained even more steam as the Iranian conflict appears to be clearing up, and oil markets have responded accordingly. With this background let’s take a deeper dive into Q2 returns.

US Sectors: Technology Back in a Big Way

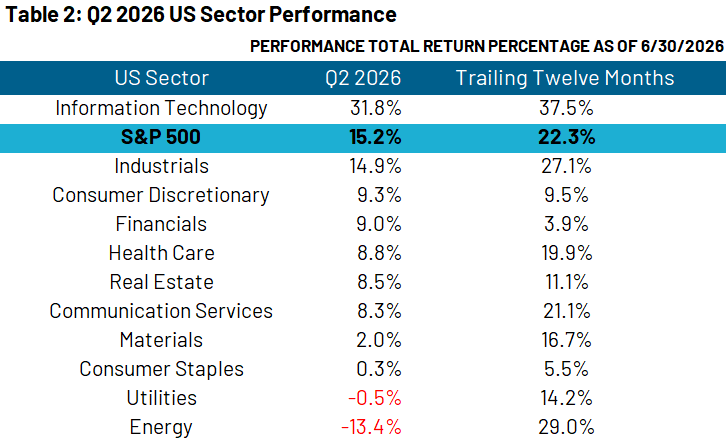

Table 2 (below) shows US sector performance. Technology was the leader by a wide margin, after posting close to a double-digit negative return last quarter. As we discussed in our most recent earnings recap, Technology earnings have continued to be very strong, driven by AI spending and efficiency gains. Similarly, the Industrials sector had a strong quarter, riding similar tailwinds as the Technology sector.

At the bottom of the returns table sits Energy. In the first quarter, the Energy sector was able to generate market-leading returns with oil prices peaking above $100 per barrel. However, as oil prices fell in the second quarter, oil returns also lagged the remainder of the market. Even with this negative quarter, the sector only trails technology from a trailing twelve-month standpoint.

The only other negative sector for the quarter was Utilities. There are two dynamics working here, in our view. First, due to the steady cash flows of the sector, Utility equities often behave like bonds. As such, in a quarter where rates rise, as they did in Q2, utilities will struggle to produce positive returns. Second, Utilities are often viewed as a defensive sector. In a quarter when investors begin to take a more risk-on posture, we would expect the sector to lag.

International Stocks: Emerging Markets Lead the Way, Despite Poor Chinese Returns

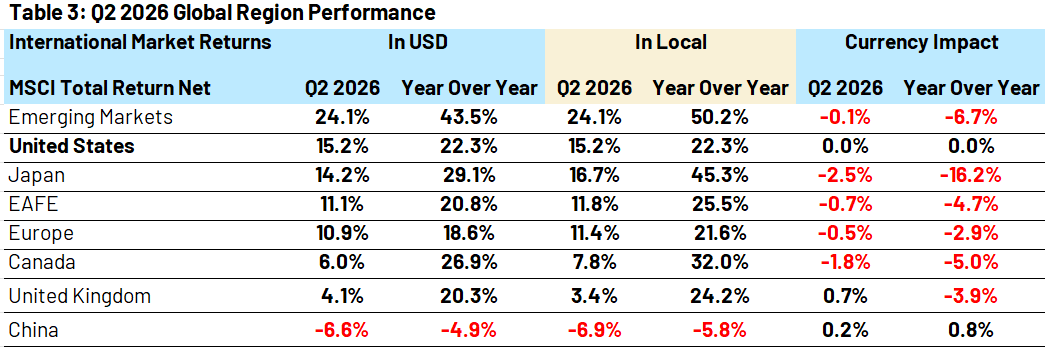

Moving to Table 3 below, we see Emerging Markets (EM) leading all global equities. This result is somewhat surprising, especially when peeking at the bottom of the table and seeing China posting a negative return for the second quarter in a row. Over the past decade, China has been viewed as the growth engine of Emerging Markets, with the broad regional returns following China. However, both South Korea and Taiwan have stepped in as growth-oriented market drivers for EM. Both of these countries posted returns over 50% this quarter, allowing EM to overcome negative Chinese returns, as well as sluggish returns in Latin America.

On the currency front, we saw a continuation of dollar strengthening. Specifically, the yen and Canadian dollar lagged the most. For the yen, this currency cross is often seen as a risk-on/risk-off measure. The dollar strengthening here could be a reflection of the market’s more risk-on stance this quarter. For the Canadian dollar, we believe weakening oil prices was the culprit, with the Canadian economy being heavily tied to commodities. In our view, this dollar strengthening is a double-edged sword for US-based investors; a strengthening dollar is a lag on returns for US investors, but for more export-focused countries, a weaker local currency could represent a tailwind for local equity returns.

Looking Forward: We Continue to be Cautiously Optimistic

In this section of our quarterly recap, we have been continuously championing the importance of earnings analysis. This quarter will be no different. Tying back to the “wall of worry,” in our view, earnings are what allows the market to climb this wall. While headlines can often focus on potential market headwinds, unless those headwinds are able to cause earnings deterioration, the market will often continue to climb. We believe that this is what we saw in the second quarter; in spite of soft macro data and geopolitical worries, earnings remain broadly strong, allowing the market to climb the wall.

Even with this constructive view on earnings, we remain vigilant in our risk processes. As a refresher from last quarter, in our shorter-horizon portfolios, our risk processes emphasize technical analysis and price momentum; in our longer-horizon portfolios, the risk focus is more heavily weighted towards deterioration in market fundamentals — though all portfolios draw on a mosaic of both disciplines. Currently, both technical and fundamental momentum remain broadly positive by our measures; however, a Federal Reserve likely on hold and elevated investor sentiment after such a strong quarter have our shorter-horizon team cautiously monitoring tactical indicators.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 07.07.2026 | Weekly View

Authored by

-

Dan Zolet CFA®

Associate Portfolio Manager