Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- AI spending has driven US markets in the face of macro uncertainty.

- US Large-Cap earnings continue to accelerate.

- Small-Cap and Japan are showing signs of strength, while Europe remains a relative laggard.

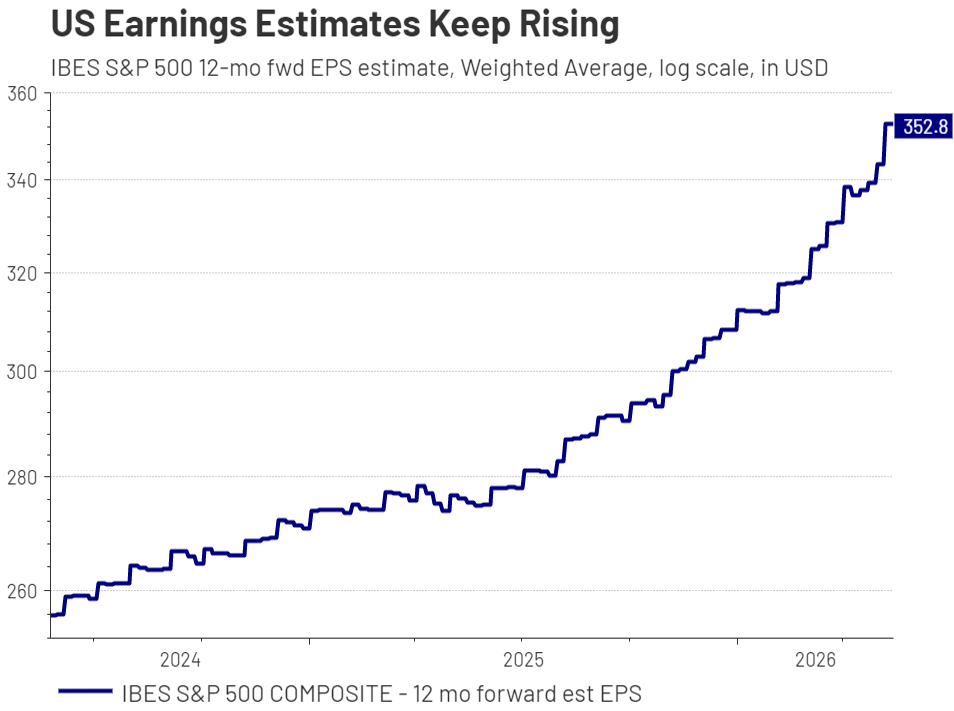

While headlines are focusing on geopolitical conflict and mixed macroeconomic data, the S&P 500 has powered to new highs, on the back of exceptional earnings, in our view. Looking at the chart below, we see that earnings expectations have not just remained resilient in the face of economic headwinds, they have actually accelerated this year.

We believe analysts are balancing the effects of the Iranian conflict, rising headline inflation, and bond yields spiking, with the tailwinds of AI (both infrastructure build and productivity gains from adoption) and the remarkable resilience of US consumers. This recent strong earnings season has demonstrated that the positives currently outweigh the negatives, with estimates expecting this to continue. The bigger point here: macroeconomic and geopolitical risks matter most when they start to erode earnings — and right now, that simply isn't happening.

With this context in mind, let’s again perform our quarterly earnings analysis, leaning on our three ‘earnings principles’:

- Earnings/Revenue Surprises: Were corporate results out of alignment with market expectations?

- Analyst Adjustments: What was the direction and magnitude of analysts’ estimate revisions after forward guidance was issued?

- Earnings/Revenue Trends: What is the long-term earnings trend?

US Large-Cap: The Standard Gets Stronger

Put simply, US Large-Cap results were exceptional this quarter, improving on an already strong prior period.

Starting with our first principle: S&P 500 aggregate earnings were 16.3% higher than analyst’s expectations, with every sector posting earnings higher than expectation. On the revenue front, aggregate revenue was 2.0% higher than expectations. Both of these numbers were better than last quarter.

Moving to our second principle, forward earnings expectations for the S&P 500 over the next 12 months have ticked upward, as the chart on page 1 illustrates.

Finally, the S&P 500 continues to shine when viewed through our final principle with year-over-year earnings growing 27.5% and sales growing 11.1%. This growth was well spread between the sectors with all eleven growing sales and only health care having negative earnings growth.

When considering equity themes, we are seeing positive results for both AI-driven equites and a potential ‘value rotation.’ Starting with AI, we continue to see strength in the Technology sector with a 50.1% year-over-year earnings growth. This figure even surpassed analyst expectations by 29.0%. Both Consumer Discretionary and Communications Services (two other growth-oriented sectors) had strong results. From a ‘value rotation’ standpoint, Materials and Financials earnings grew 39.6% and 23.5% year-over-year, respectively. These two sectors are both tied to our ‘value rotation' scenario, which we have laid out in the past.

Beyond Large-Cap: Small-Cap and Japan Improving; European Revenues Struggling

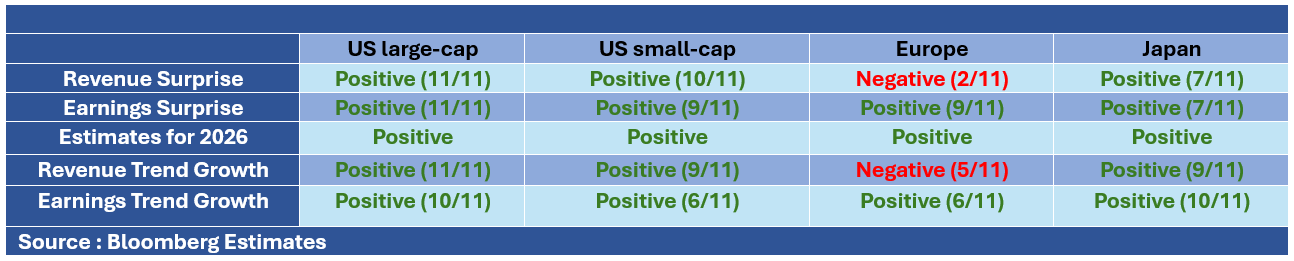

The table above summarizes RiverFront’s view of the earnings picture for four different market segments: US large-cap, small-cap, Europe and Japan (the numbers in brackets are the 11 sectors). Comparing these segments can help answer our question about value vs growth. US Small-cap, European, and Japanese equities tend to have a greater weighting in more value-oriented sectors, meaning they can provide us insight into whether earnings can provide a catalyst to a value rotation. Additionally, we can compare how each of these markets has changed from last quarter, in order to determine if there is a trend forming. Here is a quick ‘checkup’ for the three non US large-cap market segments:

- US small-cap: Small-cap earnings look strong across all three principles when looking at the aggregate level. The only cause for concern is the lack of breadth in the earnings trend, with only 6 of the 11 sectors having positive growth. While this is the same proportion as last quarter, the fact that financials have swung back to a positive trend is heartening, as this sector is often viewed as a bellwether for the broad small-cap market. Of the three other markets, US small-cap seems a cut above the other two, though the earnings breadth concern may point towards selection-led investments.

- Europe: After taking a step back towards the end of last year, the first quarter was not as clear for European earnings. After being flat to analyst expectations in the fourth quarter, earnings beat expectations, while revenue surprised to the downside. Earnings beats and revenue misses were widespread in Q1, impacting nine different sectors each. From a trend perspective, revenue continues to shrink year-over-year. Echoing our concern from last quarter, this sales growth (or lack thereof) is particularly concerning given we had hoped the foundation for a value rotation would be elevated, but moderated inflation driving revenues higher.

- Japan: Japan completes its turnaround, now scoring positively across each principle. The lone straggler from last quarter, earnings surprises, turned positive, while keeping its strong breadth across sectors. Additionally, both its earnings and revenue trends are robust, being positive in ten and nine sectors, respectively.

Conclusion: US Large-Cap Continues Strength Though US Small-Cap and Japan Beginning to Look Attractive

The first quarter earnings season was impressive for the US large-cap, as the S&P 500 improved off an already strong foundation. Additionally, US small-cap and Japan are showing strong earnings across our three metrics, though we would like to see these regions build on this in future quarters, given the up-and-down nature of the past few quarters.

As we mentioned in the intro and last quarter’s recap, as geopolitical tensions and global macro concerns create unease amongst investors, it is important to use earnings to ground ourselves. Unless these headwinds cause earnings deteriorations, we view price volatility as more of a short-term phenomenon. However, our previous discussion on the Iranian conflict remains reflective of our house view for those seeking a deeper dive into the geopolitical risks.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 05.27.2026 | Weekly View

Authored by

-

Dan Zolet CFA®

Associate Portfolio Manager