Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- The Fed is on hold as inflation concerns continue.

- The US Trend remains positive and has regained short-term momentum.

- The Crowd is optimistic but has not reached an extreme level.

Since our last ‘Three Tactical Rules’ update on April 14th, equity markets are up 6.2%, led by the technology sector and semiconductors specifically. The move higher the last eight weeks has not been without some volatility, but the market has looked past the Iran War and inflation fears. Instead, the focus has been on the upward earnings revisions that have propelled the S&P 500 to new all-time closing highs. However, the speed of the rally has impacted our tactical rules.

The Three Rules are currently a ‘flashing yellow light’ a one notch downgrade from the ‘flashing green light’ in the last update. Much has transpired underneath the surface over the last 8 weeks in each of the individual rules. Fed members have become more concerned about fighting inflation, the Trend has regained short-term momentum, and the Crowd has become highly optimistic. While the Fed’s rating was unchanged at a ‘flashing yellow light,’ the Trend was upgraded to a ‘green light,’ and the Crowd was downgraded to a ‘flashing red light.’ While the Three Rules have deteriorated since our last update, they are still giving a cautiously optimistic signal overall.

'Don't Fight the Fed': Inflation Will Keep the Fed on Hold - FLASHING YELLOW

Fed funds futures markets suggest to us that investors expect rates to be on hold into 2027, as Iran war aftershocks could raise stagflation fears. Despite Chairman Warsh’s easing bias — based on the use of the Dallas Fed’s Trimmed Mean PCE, which cuts the top 31% of items that increased in price and the bottom 24% of items that decreased in price from the inflation basket — geopolitical forces may prove more consequential. Core PCE remains elevated at 3.3% and unemployment remains low at 4.3%, leaving little room to focus on labor market downside. In our view - and many FOMC members’ views as well - the Fed's attention should instead be on upside inflation risks, particularly the second and third-order effects of high oil and gas prices.

June 17th will be Kevin Warsh’s first FOMC meeting as the Fed chair, and his first opportunity to begin shaping monetary policy. We do not expect much change right away, but based on messaging from Warsh’s confirmation hearing, investors should expect less communication regarding the path of interest rates in the future. We believe that higher yields experienced in the bond market since the beginning of the Iran War has sufficiently tightened financial conditions, giving Warsh cover not to have to raise rates. Given the heightened attention to inflation by Fed members, we no longer see the Fed squarely on the investor’s side — the war has changed that calculus. Fed funds futures have begun pricing a larger probability of rate increases starting at the end of the year into 2027. However, with a potential peace deal on the table to end the war, and lower oil and gas prices, we are maintaining our Fed rating of a 'flashing yellow light.'

Internationally, the Bank of England (BOE) and the European Central Bank (ECB) have held rates steady thus far this year. However, without an immediate end to the Iran war, both are faced with higher inflation expectations due to their economies’ energy dependence. The Overnight Index Swap (OIS) markets are now pricing in multiple hikes for each through year-end into 2027. We believe further delays in ending the war will cause both the BOE and ECB to raise rates in the coming months. Additionally, the Bank of Japan (BOJ) finds itself on the cusp of hiking rates, amid rising inflation from wages and energy costs. Globally, we now view central banks as neutral rather than on the investor’s side.

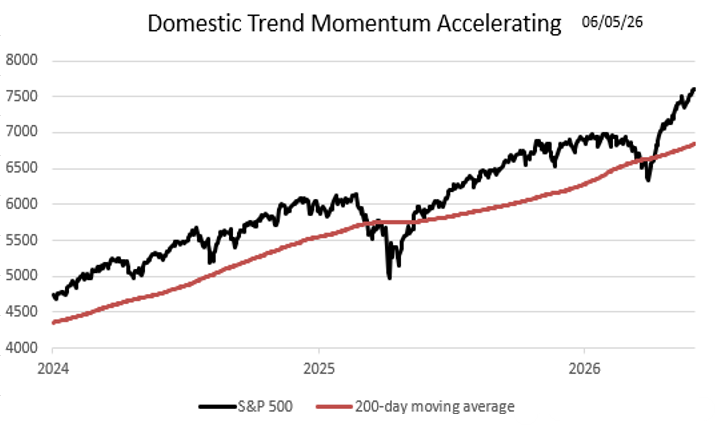

‘Don’t Fight the Trend’: Positive US Trend Regains Short-Term Momentum - GREEN LIGHT

The S&P 500's primary trend, defined as the 200-day moving average, is rising at a 23% annualized rate, up from 12% during our last update. The trend’s acceleration in pace is due to the increase in short-term momentum, as the index has increased by roughly 6% in the last 8 weeks. To put a finer point on the strength of the trend, if the index just remains steady at its current level, the trend will remain positive for the next 9 months, in our view.

Historically, the S&P 500 has risen over any given three-month period two-thirds of the time. Given the trend’s positive slope and short-term momentum, the odds of having a positive return over the next 3 to 6 months are higher than average. We believe the trend is once again the investor’s friend. This is why we prefer US stocks over bonds in our balanced portfolios. We have upgraded the Trend to a ‘green light’ due to strong short-term momentum.

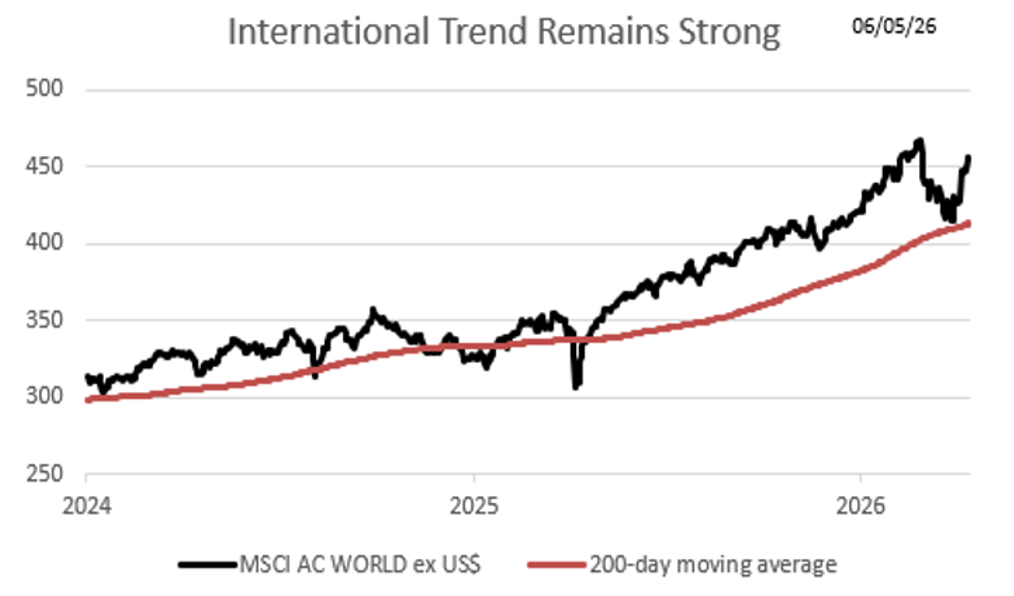

International Trend: Will Likely Remain Positive for at Least 9 Months - GREEN LIGHT

Internationally, the MSCI All Country World ex US (ACWX) trend has accelerated over the past eight weeks; ACWX’s primary trend is now rising at a 29% annualized rate, up from 18% at our last update. Like the US trend, during this period the international trend has had a burst of short-term momentum. However, it has not been able to regain the relative outperformance that it had versus the US prior to the onset of the I ran war. Over the last eight weeks, international equities have underperformed domestic equities by nearly 3%, narrowing the year-to-date edge to just 4.1%.

To illustrate the trend's strength, ACWX could remain at its current level for over nine months before turning negative — an encouraging sign, as our tactical work suggests that a trend above zero increases the odds of a positive return over the next three to six months. We are therefore maintaining its ‘green light' rating.

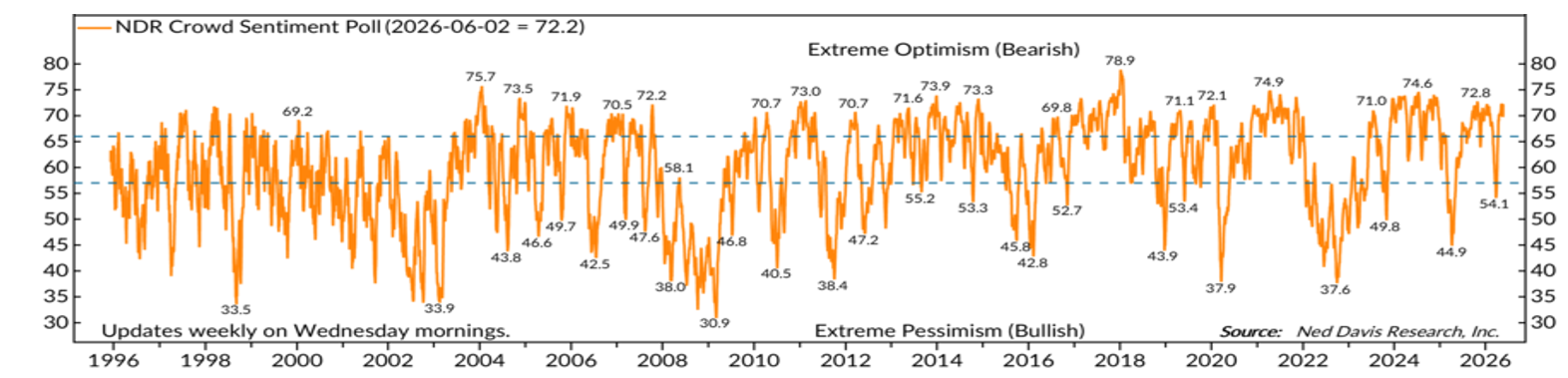

Beware of the Crowd at Extremes: Poll Extremes Gives Signal to Reduce Equities - FLASHING RED

Crowd Sentiment serves as the 'contrary' indicator within the Three Tactical Rules. The chart below reflects investor sentiment as measured by Ned Davis Research (NDR), where elevated readings signal excessive optimism and depressed readings signal extreme pessimism. Historically, NDR research suggests extreme pessimism has created attractive entry points for tactical investors. While NDR is our preferred data source for measuring investor psychology, we apply our own analytical framework to draw conclusions.

Daily and Weekly NDR Sentiment Polls are currently in the extreme optimism zone. This is a big reversal from our previous update when daily sentiment was near the bottom of the extreme pessimism zone and weekly sentiment had barely crossed back into neutral. The optimism has been fueled by the AI led rally that caused the S&P 500 to set new all-time highs. While optimism helped to give the rally momentum, it has now reached levels that warrant caution. Historically, we have weighted the Weekly more heavily in this publication, as it provides longer-term perspective, while the Daily better captures investors' real-time views. However, when the two polls send the same message we pay close attention.

The Crowd’s current optimism is elevated by historical standards, but it has not reached the euphoric levels seen in periods like 2018 as shown in the chart above. The Crowd is optimistic due to the earnings potential of AI-related companies. However, as a contrarian indicator, this optimism is signaling it is time to begin reducing equities after a strong rally. While we are not ready to sell equities when we view the Three Rules collectively, we have become more cautious regarding equity positioning through the Crowd’s lens. Thus, we are downgrading our rating for the Crowd to a ‘flashing red light’ from a ‘green light’ in our previous update.

Conclusion: Despite a Downgrade, Our Rules Still Suggest Opportunistically Buying Equities - FLASHING YELLOW

Viewed through three distinct lenses — a Fed on hold, a trend that has picked up momentum, and optimistic crowd sentiment — our Tactical Rules collectively signal a ‘flashing yellow light.’ While we have downgraded our rating from our last update, we continue to believe that the market will go higher this year. Given the fluidity of economic data, earnings guidance, and investor mood, the Three Rules will likely shift further in the weeks ahead. Over the next three to six months, we believe market conditions will continue to favor domestic and international equities over bonds, with yields remaining rangebound.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 06.09.2026 | Weekly View

Authored by

-

Kevin Nicholson CFA®

Global Fixed Income CIO | Partner