Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- We believe international stocks are not as ‘cheap’ as they first appear.

- The outperformance of the US has been due to superior earnings growth, in our view.

- There are 3 potential themes that could shift returns in favor of international… but currently we still prefer US stocks.

Our Framework: ‘Price Matters’… but So Does Macro and Earnings Data

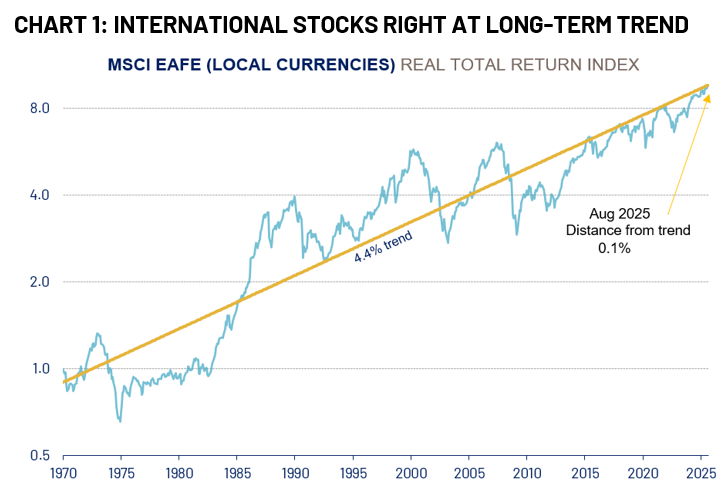

A question RiverFront often gets is when we will go ‘overweight’ on international equities, after almost fifteen years of disappointing returns. Emerging Markets (EM) and Developed International (EAFE) indices are both beating US markets year-to-date, which has only happened 3 years in the last decade. It is a fair question, given continued all-time highs and the concerns some have over elevated valuations in the S&P 500. Using our Price Matters® framework, which attempts to draw a long-term total return trend through equity prices, we can see that as of Aug 2025, developed international equities (as represented by the MSCI Europe, Australasia and Far East Index – aka EAFE) are right at their long-term trend of 4.4% (see Chart 1, below), which is 2.1% lower per annum than their US Counterpart. With US Stocks +47% above their much faster trendline, the relative valuation argument for international appears compelling, although there are a lot of caveats we would make; trend analysis is as much ‘art’ as ‘science’, especially as international does not have nearly as much data to analyze as the US. Thus, today’s Weekly View is a deeper exploration of what conditions we think will be necessary in order for International to outperform US Markets.

Valuations do matter… but we also believe that the more favorable economic environment, combined with stronger profitability and earnings growth, can justify higher valuations in the US versus international. Thus, we believe the US’ valuation gap versus peers is justified when we take a step back and look at the complete picture. Simply put, a much stronger profit trend can justify a premium valuation when viewed through the following lenses:

- The Macroeconomic Environment: In our view, most economic data is like “blood pressure;” any reading that is too high or too low requires action by a fiscal or monetary authority. We believe there is a sustainable level of economic growth and inflation at which well-run companies can thrive. For example, inflation growth rates of 2-3%, along with positive trending leading economic indicators, is a good combination for equity returns, in our opinion.

- Evidence that Earnings Are Capturing Economic Growth: Using a combination of historic and consensus earnings analysis, we attempt to identify stable and growing earnings patterns that are consistent with current economic activity.

- A Reasonable Starting Valuation: We see valuation as a long-term sentiment gauge of a market’s earnings power and profitability. Without a view of this earnings power – and the economic forces that drive these earnings - we can easily overpay for growth, or buy assets that appear ‘cheap’ but fail to generate consistent earnings. Thus, we view valuation as a ‘condition’… and not necessarily a ‘catalyst’ to generate outsized returns.

US and International Markets Thrive in Different Business Climates… and the Last Decade Favored the US

One major difference between the composition of US large-caps and EAFE is that the US has a much higher weighting towards ‘growth’ companies, whereas EAFE is dominated by ‘value’ companies. Specifically, stocks of growth companies tend to thrive in lower-interest-rate environments, where GDP growth tends to be lower. In these environments, their organic growth provides attractive levels of profitability, and they can utilize low interest rates to repurchase shares (and thus reduce their share count), using cheap debt. Put simply: growth companies are adept at squeezing attractive earnings growth out of a slow and steady economy such as the one that we’ve seen for the last half-decade. Luckily for the S&P 500, the US large-cap space is stocked with growth companies in areas like technology, consumer discretionary and communication services.

On the other hand, value companies tend to perform well in times of elevated economic growth. The higher growth helps cover their higher fixed costs, which then allows for higher margins on sales; we call this “operating leverage." Put simply: when economic growth is high, operating leverage tends to allow value-oriented companies’ earnings to outgrow more stable, less economically sensitive sectors. International Markets like EAFE tend to be much more value-oriented, with larger weightings to sectors such as industrials, energy and financials.

While there are also more defensive companies in international markets than in US markets, such as consumer staples or utilities, the major difference is in value and growth, in our view. This generally holds true with international markets as well, with the notable exception of China, which has similar technology companies to the US that emerged in the middle of the last decade.

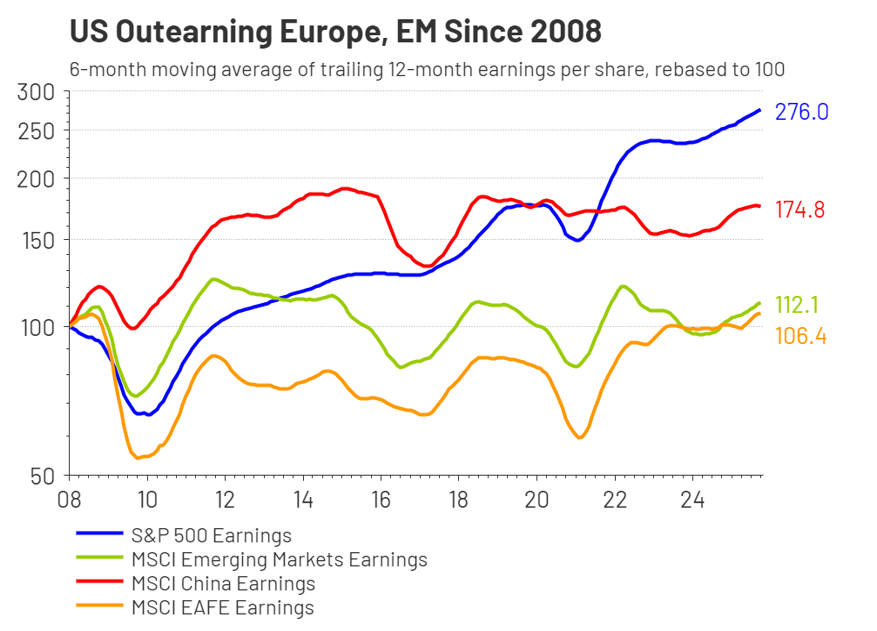

We can see the cumulative impact of low interest rates and lower economic growth on earnings in global markets from 2008-2025 (see Figure 2, above), an era that strongly favored US markets over international. This era was marked by disinflation and even occasional deflation in various economies, which led to much slower nominal economic growth. This economic dynamic hurt earnings for the value sectors and benefitted the growth ones, in our view.

Overlaying that was a secular technology revolution, which has continued to this day through the proliferation of Artificial Intelligence (‘AI’). This dynamic is why the S&P 500 has dramatically outearned EAFE since 2008, in our opinion. While the interest rate and inflation environments have shifted in a way that should favor value-oriented companies, the AI theme is proving to also be a durable source of earnings for technology and growth companies. The question of which type of companies (“Growth-Oriented” or “Value-Oriented”) will perform better going forward will come down to a combination of three themes, which we will explore a little below.

Three Possible Themes That Could Cause International to Outperform the US Going Forward

Theme #1: The Artificial Intelligence Race Becomes a Broader Boom… or a Bubble-and-Bust

The vast majority of the investment in AI is occurring in the United States and China. While there are other countries with specialized semiconductors and software niches, it is likely that a boom in this area will continue to galvanize macroeconomics and earnings in these countries. Our current belief is that we are still in the early innings of the AI trade, and our current preferences for large cap technology themes in our portfolios reflect that. We are also bullish on US companies that provide the infrastructure for AI – these are companies that provide the power and equipment needed to run the software.

What is less clear to us is whether investment in Chinese equities is attractive long term, as we remain wary of the Chinese government’s grip over wealth creation and entrepreneurship. We recognize that the nature of the AI race is one of US/China adversarial competition, so there the government of China could squelch AI returns from reaching US shareholders either by restricting the profitability of the companies, or restricting US access. Either way, that dynamic represents a major negative for US investors in Chinese assets, in our view.

If the AI trade rolls over, Europe, Japan and other regions will likely be relative winners over the US. However, we would argue that withholding investment in AI globally would also likely cause a global economic slowdown, a condition that likely would be negative for stocks generally in all geographies. That backdrop would likely shift our portfolio strategy into considering more defensive positions - like bonds - in our portfolios, rather than increasing international stocks.

Theme #2: The Trade War, Foreign Currency, and the Path of Interest Rates in the US

It is still too early to be certain of the impact of the significant US trade policy shifts that occurred in 2025 – it is not yet clear if they are putting recessionary or inflationary pressure on markets. What is becoming clearer is that economic growth is softening enough for a handful of US rate cuts to be justified. This will help with another growing problem on the horizon for the US, which is financing its burgeoning deficits without reigniting inflation. That tightrope is going to be very challenging to navigate, and the current likely path (i.e., lower rates, continued deficit concerns, and an uptick in inflation) would all put downward pressure on the US dollar versus other currencies. Since buying international equities is also implicitly a bet on the foreign currencies the companies are domiciled in, there is a case to be made for international returns to improve based on this impact. When we look at the outperformance of international markets relative to the US in 2025, foreign currency strength is one of the primary contributors. Thus, we would need to see greater follow-through on US rate cuts for this policy to continue.

One other thing to consider if this scenario plays out is that lowering interest rates is also very favorable to US small-cap equities, as we covered in detail a few weeks back. That fulcrum could help us decide to rotate to US Small Caps instead of International. In order to judge the relative attractiveness of these ‘value’-oriented asset classes, we will likely be comparing earnings on our earnings framework. We believe that corroboration of earnings trends would be a powerful confirmation that our theories around operating leverage businesses and the impact of rates are showing up (or not) in the earnings of those smaller companies; that is ultimately what we want to see for sustainable investments, whether in the US or abroad.

Theme #3: The ‘European Re-Armament’ Trade

One of the side effects of Trump Administration policies has been a demand for NATO members to increase their spending in defense and infrastructure. The combination of this mandate and the re-routing of global supply lines to navigate the tariffs and trade restrictions imposed could create a positive cycle of stimulus in Europe, and the infrastructure needs could also help cyclical companies globally begin to spin up their operating earnings.

Since we are not yet sure this is a durable theme, we are waiting for earnings confirmation, as well as policy guidance from European nations to become a little clearer. We also see regulations and non-market-friendly labor laws as headwinds that investors in Europe likely face, so we do not believe that one event or policy in one country will be enough to have a sustained impact – this theme will require a sequence of favorable policy developments.

CONCLUSION: International is Not Compelling Enough to go “All-In” Yet

The three themes we laid out will take a few years to play out, if at all. Our portfolio positioning reflects our belief in the economic strength and momentum of the US Tech / AI trade, and we would want to see more policy clarity and earnings confirmation before we make any large shifts into international. Our current positioning is to be roughly in line international with global benchmarks, with a preference towards European Banks, Japan and value-oriented themes… and avoiding Chinese equities. We believe this is sufficient exposure to capture the upside of these markets while we wait for more concrete earnings evidence to emerge.

It is also important to note that there are companies and countries that might behave differently than the broad market. We will continue to use our security selection disciplines to identify potential early leaders or areas that may have attractive opportunities. We feel this flexibility is one of the advantages that having deep expertise in bottom-up stock research can bring to portfolio management, and it is possible we might make smaller trades into narrow international themes, even if we do not see the macro story of American ‘Economic Exceptionalism’ deteriorating.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 10.28.2025 | Strategic View

Authored by

-

Adam Grossman CFA®

Global Equity CIO | Partner