Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- US large-cap earnings results remain strong, and small-caps improved more than expected.

- European results were mixed, and Japan seems to be struggling.

- The impact of tariffs on US markets is not yet fully evident.

With over 90% of S&P companies now having reported, we feel we have enough data to perform our quarterly earnings season ‘checkup’. In order to complete this checkup, we will use our three ‘earnings principles’:

- Earnings/Revenue Surprises: Were corporate results out of alignment with market expectations?

- Analyst Adjustments: What was the direction and magnitude of analysts’ estimate revisions after forward guidance was issued?

- Earnings/Revenue Trends: What is the long-term earnings trend after the announcement?

While it may be too early for tariffs to show their full impact, we are on alert for any deterioration in any of our readings as we examine US large-cap through our earnings framework. Starting with the first principle, we are encouraged that so far tariffs have not put a dent in US earnings relative to expectations; the S&P 500’s earnings were +8% higher than anticipated (source: Bloomberg), with every sector but Materials beating expectations. These results seem to corroborate our view that the combination of stable interest rates and sustained inflation levels between 2-3% percent has created an environment whereby business models with high fixed costs but low variable ones (a feature called ‘operating leverage’) can thrive.

From a revenue perspective, we were also encouraged by sales coming in +2.1% higher than analysts expected, with all 11 sectors showing positive revenue surprises. This also allays our fears that tariff impact might be worse than the analyst community feared.

Moving to our second principle, future earnings expectations for the S&P 500 over the next 12 months have ticked upward in response to positive earnings surprises (see Chart 1, above). Similar to our take on surprises, analysts have continued to see a way for US large-cap to continue growing earnings.

Finally, the annualized trend of US large-cap earnings continues to be a positive +12.38% year over year overall, supported by revenue growth of +6.25%. At a sector level, Energy, Materials and Staples all had negative earnings growth over the period, and Energy was the only sector to have negative revenue growth. If we are looking for tariff warning signs in this data, there do not seem to be many we can fully attribute to them. We partially expected this outcome for energy given the decline in oil prices in 2025, and materials to a similar drop in commodity prices. Staples is likely due to higher rates squeezing margins.

This healthy checkup for growth themes is critical for US large-capitalization stocks, as our constructive view of US returns is predicated on a continuation of strong earnings. Given the rebound in US large-cap stocks post “Liberation Day”, we are hopeful earnings can continue on their current pace in the quarters ahead. We view continued earnings growth as necessary to support further returns, given elevated valuations (as discussed in last week’s Weekly View).

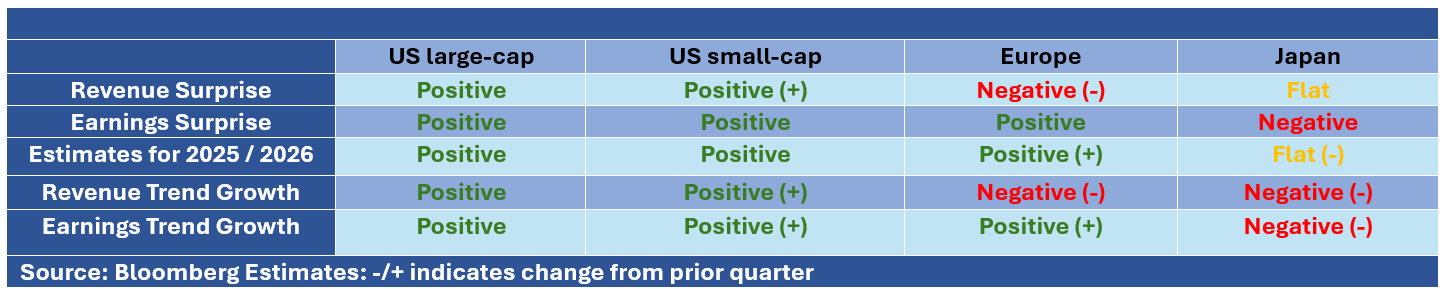

Small-Cap Improving, International is Deteriorating

The table above summarizes RiverFront’s view of the earnings picture for four different market segments. Relative to US large-caps - which have a clear growth/technology bias – US small-caps, Europe and Japan all have a greater weighting in the more value-oriented sectors. Again, due to operating leverage, we believe these themes should begin to respond positively to a macro environment of falling short rates and modest (2-3%) US inflation. As such, while we look for continued strength in larger US companies, in these other markets we instead are looking for improvement. In the table above, the “+” and “- “signs indicate our view of how things have changed since the previous quarter.

Beyond Large-Cap: Other ‘Value-Led’ Market Segments Mixed… US Small-Caps Faring Better than Europe or Japan

- US Small-Cap: Small-cap earnings have seen quite a positive turnaround in all of our earnings principles. While the sector-by-sector revenue and earnings story is more mixed versus large-caps, overall small-caps’ improvement is apparent. What is not yet clear is if a single encouraging quarter is an aberration or a start of a new trend. However, taking this improvement in tandem with the increasing potential for interest rate cuts, investors could begin to make a case for small-cap as an investment. Some potentially attractive sectors in our view include technology, industrials and healthcare. Compared to Europe and Japan, there is little evidence of tariffs having a negative impact, at least thus far.

- Europe: Looking through our framework, European equities are somewhat of a mixed bag. Positive trends are emerging in earnings strength and improving analysis revisions. Our primary area of concern with European earnings is that revenue numbers are not faring as well. This is particularly troubling for European indices since their business models tend to have more operating leverage than US companies, in that they tend to require more top-line growth to cover higher fixed costs. A particular concern is that Industrials, Consumer Discretionary and Materials are all weak, which could be early areas impacted by tariffs. Meanwhile European Financials, which are largely immune to tariff impacts, are holding up well on earnings and revenue. While it is premature to draw any conclusions, a hopeful international investor would have liked to see stronger overall results in Europe – we will watch for improvement here as the “re-armament” plans are implemented across the continent.

- Japan: Unfortunately, Japan’s earnings have deteriorated across the board using our analytical framework. While technology and communication services companies in Japan seem to have bucked the general trend of earnings and revenue deterioration, in general Japan experienced a tough earnings quarter. It is also likely that tariffs are having an impact on export-oriented discretionary industries such as automobiles. We will watch in the quarters ahead of either reversals or confirmation of these negative trends.

Conclusion: Still Favoring US Large-Cap Stocks; Want More Data for the Other Segments

The continuation of strong US large-cap earnings is a reminder of our view that American corporate earnings are exceptional – even small-cap companies were able to post improved numbers amidst the myriad of tariff-related and macro challenges. However, this is only one quarter of earnings. For small-caps, the potential combination of rate cuts and another quarter of improvement would likely warrant serious investment consideration, especially in our more risk-tolerant, longer-horizon portfolios. Given the uneven earnings trends, this potential investment would likely be directed towards specific sectors or themes, as opposed to broad vehicles.

RiverFront portfolios are positioned consistently with the takeaways of this analysis, in our view. We are overweight US large-cap stocks across our balanced portfolios, driven by the S&P 500’s demonstrated earnings strength. We have also made selective investments in Europe and Japan, with distinct tilts towards Value and Financials. With the impact of tariffs creating uncertainty, we will be monitoring corporate surveys, business confidence, earnings guidance and analyst revisions to assess whether the risk of recession has increased.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 09.03.2025 | Weekly View

Authored by

-

Adam Grossman CFA®

Global Equity CIO | Partner