Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Note to reader: this Weekly View will provide a recap of Q1 returns. If you are curious about our most recent thoughts on the conflict in the Middle East, please refer to last week’s commentary.

SUMMARY

- The Energy sector led global Markets.

- US markets lagged due to growth sectors.

- We believe earnings provide a strong fundamental foundation, should tensions ease.

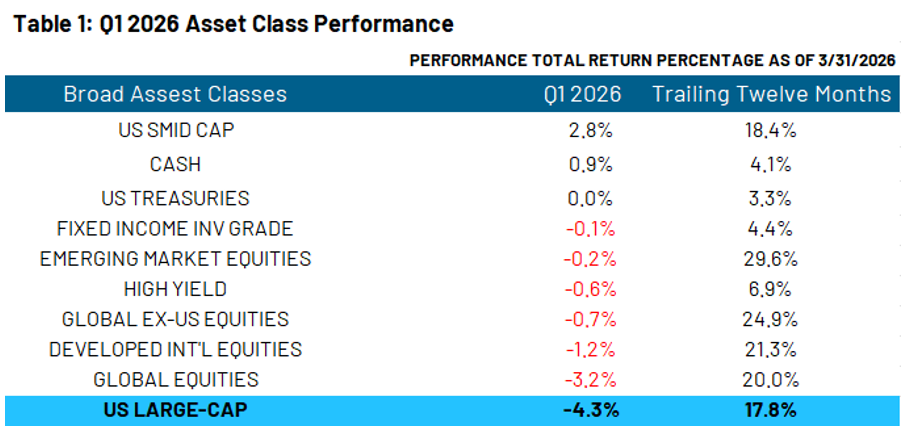

Q1 2026 began as a continuation of the market broadening and strong returns of the second half of 2025. However, markets are not insulated from geopolitical shocks, and the Iranian conflict created meaningful headwinds that pushed most segments into negative territory by quarter's end. Let's take a deeper dive into the quarter that was.

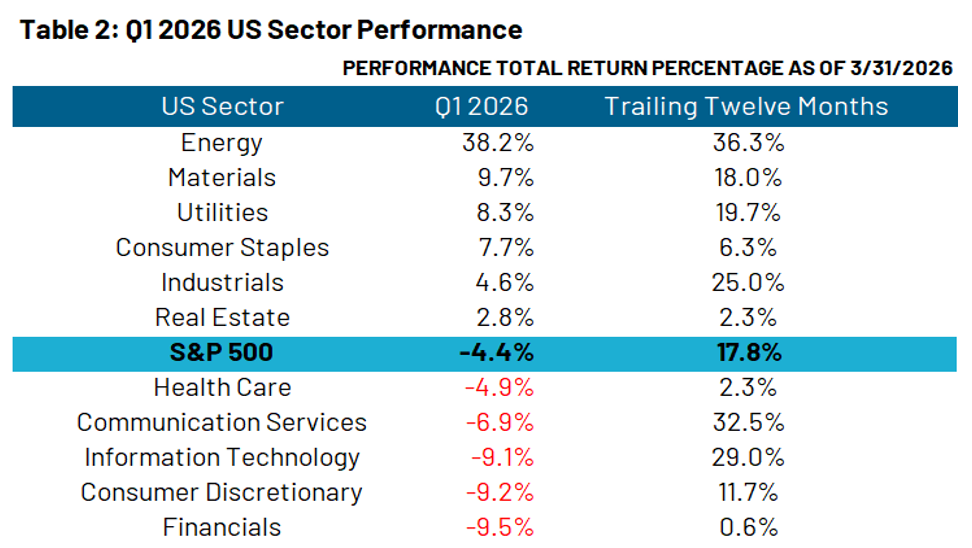

US Sectors: Value Rises; Growth Falls

Table 2 below shows US sector performance. Energy led by a wide margin, driven by the spike in oil prices over the past month — its first quarter outperforming the broad S&P 500 since Q1 of last year. This quarter illustrates our long-held view on Energy's role in a portfolio: while the sector can 'walk in the woods,' detached from broader market returns for quarters at a time, it also provides a valuable hedge against risks that are difficult to protect against — including geopolitical conflict and inflation.

Both the materials and industrials sectors also produced positive returns this quarter. Both sectors had strong January and February before March trimmed some of their gains — a potential sign that the market broadening we have discussed was underway prior to the Middle East conflict. Our earnings analysis supports the case for this trend to continue if geopolitical headwinds ease.

At the bottom of the returns table above sit three traditional growth sectors — Communication Services, Technology, and Consumer Discretionary — along with Financials. These growth sectors entered the quarter with historically stretched valuations; in a market selloff, it is typically the most expensive segments that have the furthest to fall. That appears to be the case here, as underlying earnings — particularly in Technology — remain strong despite the price declines. Within Financials, every industry posted negative returns, with Consumer Finance, Capital Markets, and Financial Services contributing most to the shortfall.

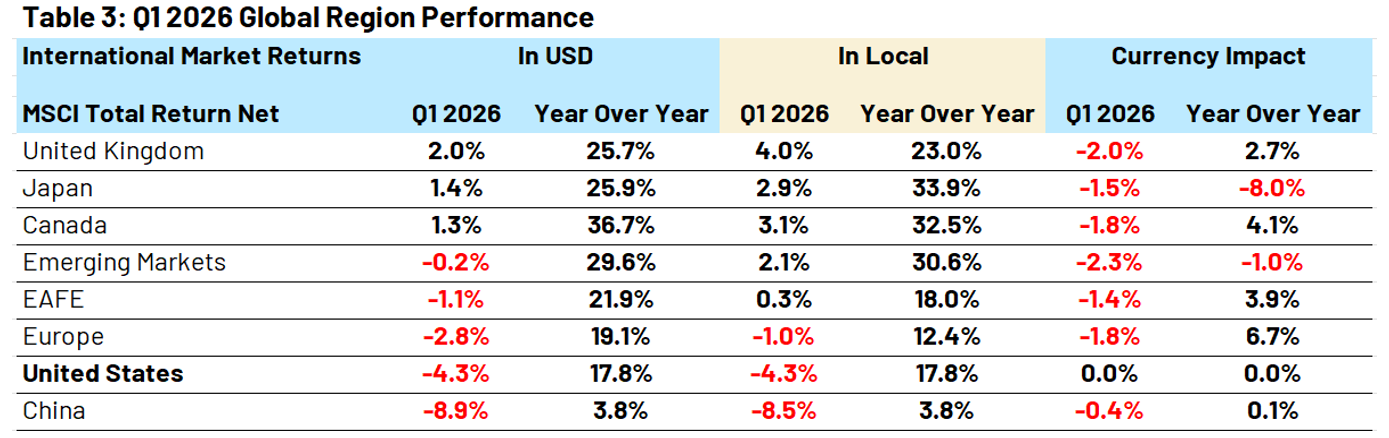

International Stocks: Overseas Returns Mirror US Themes

Moving to Table 3 below, we see similar themes internationally as we saw in the US. Both the UK and Canada posted positive returns on the back of their energy sectors. Energy is the second biggest sector in Canada and the fourth biggest in the UK. These larger concentrations of overseas energy stocks had returns that were comparable to US energy, which allowed these countries to avoid negative returns. Japan was the other country that posted positive returns and similarly was driven by value sectors, though the primary driver was their industrial sector.

The notable laggard was China, the only international market in our universe with a Technology weighting comparable to the US. In a quarter where growth underperformed, China predictably lagged its international peers — for the second consecutive quarter.

On the currency front, no single currency moved dramatically, but a clear trend emerged: a strengthening US dollar. This reverses the weakening trend we saw in 2025, and if it persists, it will represent an additional headwind for international equities from the perspective of a US-based investor.

Looking Forward: Not The Start to 2026 We Had Hoped For…but No Reason to Panic

In this section last quarter, we opined about the potential for market broadening in 2026. As we mentioned above, we saw some of this broadening early in the quarter before the current conflict in the Middle East derailed markets. However, as we discussed last week, it is important not to lose the forest through the trees: earnings remain broadly strong, and that matters. Earnings will ultimately dictate both the longevity of any value-oriented broadening and the durability of the technology mega-trend that has defined the past decade. If geopolitical tensions ease, there is ample support for a resumption of the strong returns we have seen in recent years, in our view.

In the meantime, RiverFront's risk management process remains on alert, as evidenced by a second reduction in equity weighting in our two shortest-horizon balanced portfolios since the Iran war began. To be clear: in our shorter-horizon portfolios, our risk processes emphasize technical analysis and price momentum; in our longer-horizon portfolios, the risk focus is more heavily-weighted towards deterioration in market fundamentals — though all portfolios draw on a mosaic of both disciplines.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 04.07.2026 | Weekly View

Authored by

-

Dan Zolet CFA®

Associate Portfolio Manager