Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- We believe the Fed is on the investor’s side as it continues to prioritize the labor market.

- The Trend remains positive, giving us confidence to overweight domestic equities.

- The Crowd’s neutral stance continues to signal opportunistic buying of stocks, in our opinion.

Since the last update of our Three Tactical Rules on September 23rd, equity markets have continued to grind higher, as the S&P 500 has continued its ascent towards 7000. During this period, our tactical signals have kept us bullish despite tariff uncertainty between the US and China, and a government shutdown creating uncertainty and limiting economic data flow to investors and policymakers like the Fed.

As we turn to preview the three ‘Tactical Rules’, the Fed continues to prioritize employment over inflation in the short term, having lowered interest rates now for two consecutive meetings. We believe this means monetary policy remains on the equity investors’ side via easing financial conditions. The Trend is positive, and we believe it will remain strong through the end of the year. Finally, the Crowd has tempered some of its enthusiasm. Taken as a whole, the Three Rules still appear to be a “flashing green light” - remaining where they have been anchored over our last three updates.

‘Don’t Fight the Fed’: Prioritizing Labor Market in the Short Term - GREEN LIGHT

On October 29th, the Federal Open Market Committee (FOMC) lowered interest rates for the second time in two months. The FOMC lowered the fed funds rate by 25 basis points, bringing the effective fed funds rate down from 4.11% to 3.87%. A rate cut was expected by financial markets, as fed fund futures two days prior to the meeting predicted a 97% probability of a rate cut. In our view, the latest rate cut fully aligns with the Fed’s apparent stance of prioritizing employment over inflation in the short term. It remains to be seen whether the Fed’s rate cuts will continue much past 2025. It’s possible that these cuts have primarily been for risk management purposes to preserve labor market stability, and thus further cuts may not be needed if employment stabilizes.

The conundrum the Fed faces is that it is trying to navigate using mostly instinct, due to the lack of economic data being produced during the ongoing government shutdown. This is like driving a car at night without headlights. In the Fed’s case, it is having to rely on private alternative data providers and their own anecdotal information gathered by talking to individuals and companies within each of the twelve Federal Reserve districts. While some data is better than none, it is not the official government data that has withstood the test of time...complicating the Fed’s job, in our view.

Currently, financial markets are expecting an additional 25 basis point cut in December. With core CPI stuck at around 3% since the summer of 2024, we are not sure that the Fed will prioritize the labor market over employment for an extended period. However, recent lay-off announcements at some of the country’s largest companies could help keep a lid on rising wages and in turn slow inflation. This could be the cover the Fed needs to cut further.

However, Chairman Powell warned against jumping to conclusions regarding future Fed moves, stating “a further reduction in the policy rate at the December meeting is not a foregone conclusion” in his press conference following the FOMC decision. Powell’s statement highlights the division brewing inside the Fed regarding the appropriate policy moving forward, as some members want additional cuts and others want to hold rates steady. Only time and more data will determine the outcome. In the context of our Tactical Rules, however, the current circumstances place the Fed still on the side of the investor as it is cutting rates to ease financial conditions. Thus, we maintain our rating of a “green light.”

Internationally, the Bank of England (BOE) has been gradually lowering rates as it tries to normalize its policy rate. The BOE last lowered rates by 25 basis points in August and then paused at its September 18th meeting, holding the policy rate to 4.00%. The BOE is expected to hold its policy rate steady into 2026 to combat inflation, based on the information derived from the interest rate swaps market. Meanwhile, the European Central Bank (ECB) is also expected to hold its deposit rate steady into next year as well, after leaving its deposit rate unchanged at 2% at its October 30th meeting. While the speed of monetary policy easing is different at each of the major central banks, we believe these central banks are fully aligned with “Don’t Fight the Fed” and are thus on the investor’s side. The Bank of Japan (BOJ) is the one exception, as it is currently raising interest rates after leaving them artificially low for an extended period.

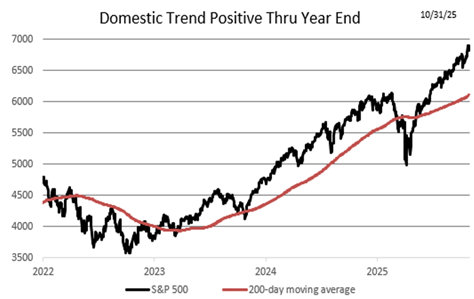

'Don’t Fight the Trend’: The US Trend Will Likely Remain Positive Through Year-End - GREEN LIGHT

The trend on the S&P 500, which we define as the 200-day moving average, has continued to move higher over the last five weeks. Since our last update, the index has risen by nearly 200 points and in the process set a series of closing all-time highs. Since our last update, the technology sector has reclaimed its dominance and has been the driving force behind the index’s move higher as both consumer discretionary and communication services have cooled. Currently, the trend is rising at an 18% annualized rate, and we believe it will remain positive through year-end even if the index pulls back to 6428, the 23% retracement of the rally from of the April 7th low. The 23% retracement is up from 6238 in our last update. Hence, the positive trend gives us the confidence to continue to hold US equities. Using history as our guide, the odds of positive return over the next 3 months are on the investor’s side. We believe that ‘American Economic Exceptionalism’ is not dead, and corporate America will continue to adjust as highlighted by the year-over-year growth of S&P 500 earnings of 10% for those companies that have reported thus far for Q3. Hence, domestically our rule of “Don’t Fight the Trend” continues to signal a “green light.”

International Trend: Reached an Inflection Point as Acceleration is Unsustainable - FLASHING RED

Internationally, the trend of the MSCI All Country World ex-US index (ACWX) has also accelerated over the last five weeks. The run rate of the primary trend is currently rising at a 33% annualized rate, compared to a 24% annualized rate in our previous update. During this period, international equities underperformed domestic equities by roughly 66 basis points. The international trend has accelerated so much this year that its’ current pace is unsustainable, in our view. Our tactical work has shown that a positive trend increases the odds of a positive return over the next three to six months. However, when the trend gets too high, the odds no longer improve. We believe that we have reached that inflection point. Hence, we are downgrading the international trend to a “flashing red light” from the “green light” rating that we initiated back in mid-March.

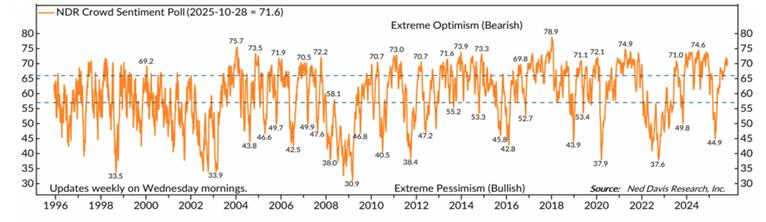

Beware of the Crowd at Extremes: Sentiment Continues to Have a Small Impact on Expected Returns - YELLOW LIGHT

We regard Crowd Sentiment as the ‘contrary’ indicator of the Three Tactical Rules. The chart below shows a measure of investor sentiment as calculated by Ned Davis Research (NDR). When the line is high it shows excessive optimism, and when it is low, extreme pessimism. NDR research suggests that historically, extreme pessimism can create attractive entry points for tactical investors. This is our preferred data source to measure investor psychology, though we use our own analytical framework from which to draw conclusions on sentiment.

Currently, the NDR Daily Sentiment and the NDR Weekly Sentiment Polls are giving slightly different signals. The Daily sentiment remains in the middle of the neutral zone, while weekly sentiment remains at the lower end of the excessive optimism zone. This is the same condition we experienced in the September 23rd update. Historically, we have given more weight to the Weekly for this publication despite incorporating both measures of sentiment in our overall rating. The Daily tends to be a good indicator of the investor’s ‘real time’ view of financial markets, while the Weekly gives longer term perspective of the Crowd. Given the current levels of the polls, we believe that the Crowd maintained its cautious optimistic view over the last five weeks, as the economic data has become more nuanced. The Crowd continues to signal opportunistic buying of equities, in our opinion. Hence, we have maintained our rating for the Crowd of a “yellow light.”

Conclusion: The Tactical Rules are More Bullish for Domestic Equities - FLASHING GREEN

The tactical rules signal a “flashing green light” as the Fed navigates the macroeconomic environment without the benefit of the government data it has grown to depend on. The Fed is taking the pre-emptive step of lowering rates to avoid tipping the scales too far in the direction of labor, at the expense of letting inflation pick up too much. The good news for investors is that the Fed is willing to ease financial conditions in the short term. Additionally, the trend remains strong, and the crowd has avoided reaching an optimistic extreme that would warrant reducing equity exposure, in our opinion. Hence, our Tactical Rules are giving us an overall bullish signal domestically. Over the next 3 to 6 months, we believe that market conditions favor domestic over international equities, as the international trend has risen at an unsustainable level.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 11.04.2025 | Weekly View

Authored by

-

Kevin Nicholson CFA®

Global Fixed Income CIO | Partner