Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

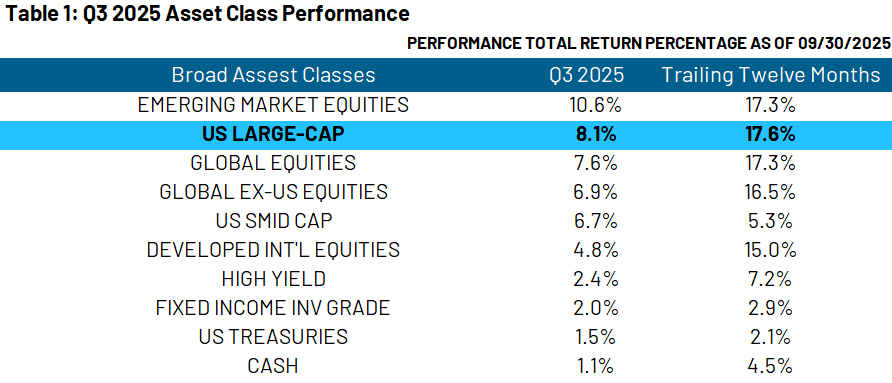

- ‘Growth’ remains king in the US.

- China posts best return in our global universe.

- Earnings continue to be key input for future investment.

In the third quarter of 2025, ‘growth’ themes1 that started to regain their mojo in the 2nd quarter reclaimed their leadership for the year. Growth-heavy markets of China and the US saw strong returns, while the more value-oriented European markets posted weaker returns compared to the previous quarter. In RiverFront’s view, this strength is primarily related to corporate earnings. Growth-leaning sectors continue to see strong earnings trends, while despite an improving macro environment for value stocks, value companies’ earnings growth has yet to come to fruition. Let’s take a deeper dive into these returns to see how these themes played out.

1 At Riverfront, we generally categorize the Technology, Communication Services, and Consumer Discretionary sectors as 'growth' sectors and the Energy, Industrials, Materials, and Financials sectors as 'value' sectors.

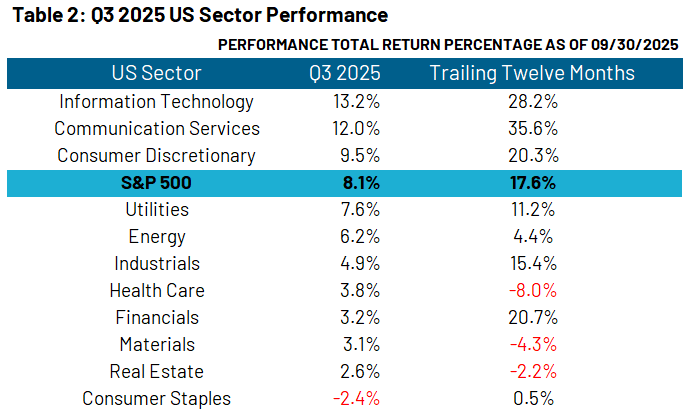

US Sectors: Growth Continues to Drive the Market

Table 2 (below) shows US sector performance. As we discussed last quarter, while the quarter-to-quarter returns may feel like a tug-of-war between ‘growth’ and ‘value’, when we zoom out it can be viewed more as volatility around a secular ‘growth’ mega trend. This pattern is further displayed in the third quarter’s returns, with three of the primary ‘growth’ sectors (tech, communication services and consumer discretionary) posting returns above the index. Furthermore, these returns are backed up in strong earnings trends, in our view. As such, we remain overweight US ‘growth’ themes relative to our global benchmarks across each of our model portfolios.

Looking at the bottom of the table, we see several ‘defensive’ sectors which posted a negative return, led on the downside by consumer staples. We believe that this underperformance was driven by two factors. First, these sectors had strong returns earlier in the year, as the market attempted to hedge against market volatility caused by tariffs. As the market continues to look past tariffs, investors become more willing to move on from these hedges. Second, we believe that there are specific macro headwinds that these sectors face. For staples specifically, our view is that the past year of elevated inflation has begun to eat into margins and with tariffs still looming, we do not see any reprieve on the horizon. Again, this is a trend that we see corroborated in earnings, with staples being one of three US sectors that had negative year-over-year earnings growth (the other two being Energy and Materials).

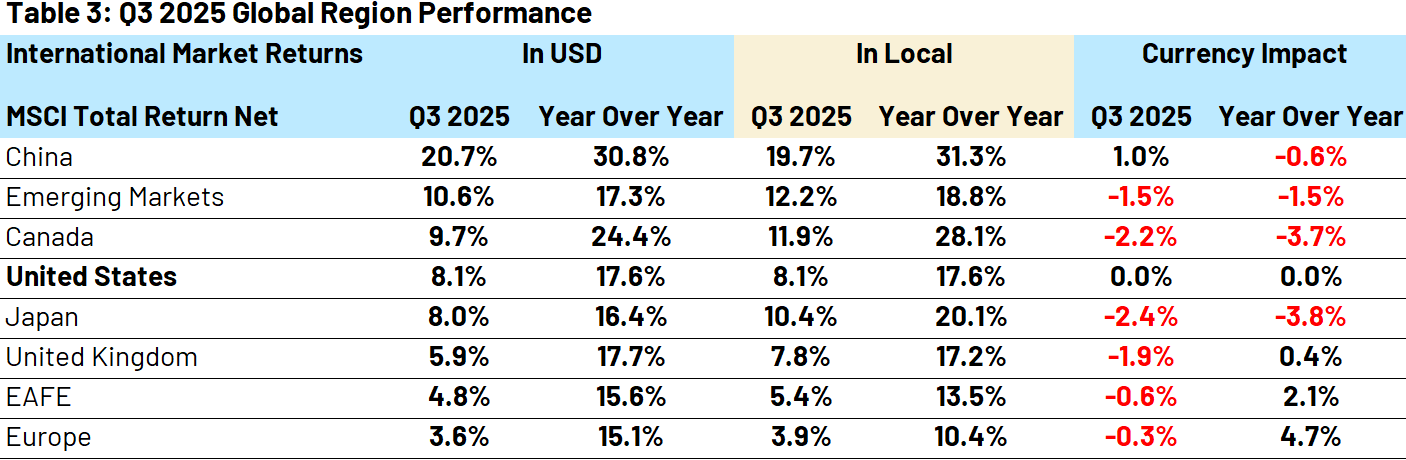

International Stocks: China Leads, While the Dollar Stabilizes

Moving to Table 3 (below), Chinese equities led the way for international markets. This is another example of the ‘growth’ rally we saw in the US, with China being one of the rare technology-heavy indices in the international space. Despite these strong returns, we remain cautious about Chinese equities. We view the risks caused by China’s geopolitical posturing and the China Communist Party (CCP’s) track record of market-negative actions (especially towards foreign investors) as legitimate and believe that a discount should be applied to China’s market multiples. Taking all of that into consideration, we remain long-term cautious on Chinese stocks.

The other international market that had returns above the US was Canada. While the Canadian dollar continued to weaken relative to the US dollar, local equity returns made up most of the US investor’s return. This rally in Canadian equities is a continuation of strong returns from the second quarter and, in our view, is a result of strong precious metal prices.

Finally, on the currency front, the US dollar seems to have found some stability, at least for the moment. After two strong quarters for foreign currencies, the dollar strengthened against each currency in our universe apart from the Chinese Yuan, which notably did not participate in the rally.

Looking Forward: Continuing to Watch Earnings

Running the risk of sounding like a broken record, when we consider the past quarter of market returns in the context of looking forward, earnings remain the predominant catalyst for further upside in markets. When we look at the current macro-economic environment and the general dovishness of central bank policy, there are reasons to believe ‘value’ equities, including small-cap and international, should start to see tailwinds in the coming quarters. Specifically, we believe a backdrop of moderately elevated inflation and expansionary global central bank policy should both be big boosts to the cyclical ‘value’ business model.

However, we continue to see stronger earnings in ‘growth’ themes than in ‘value’ ones so far. When we combine these strong earnings with strong market returns, it is hard to argue against ‘growth’ equities right now. However, we are also aware that growth equities will not sustain their earnings growth or their rates of returns indefinitely. Thus, we must remain vigilant in our earnings framework and continue to be receptive towards a ‘value rotation’ if we begin to see it burgeoning in earnings data.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 10.07.2025 | Weekly View

Authored by

-

Dan Zolet CFA®

Associate Portfolio Manager