Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- RiverFront believes asset allocation is the dominant driver of investment returns.

- No asset class wins every year — and that's exactly why diversification works.

- RiverFront believes asset allocation should be dynamic, not static.

- RiverFront believes in combining ‘strategic’ (long-term) views of an asset class’s value with ‘tactical’ opinions of shorter-term drivers.

No asset class wins every year — and that's exactly why diversification works. Because performance leadership rotates unpredictably across asset classes year- to- year, a well-diversified portfolio captures broad market returns, reduces volatility, and enables the power of compounding. Trying to pick winners annually is a losing game, in our view; owning the right mix consistently is not.

Asset allocation — determining the appropriate mix of stocks, bonds, and cash in a portfolio — is the foundation of portfolio management. The right mix should minimize volatility and risk while allowing investors to work toward their objectives. RiverFront believes this is best achieved using robust return estimates for stocks and bonds, known as capital market assumptions (CMAs), to determine the optimal allocation. We further believe that once set, this allocation must be dynamically updated.

The Study That Binds Investors to Asset Allocation

Forty years ago, researchers Gary Brinson, L. Randolph Hood, and Gilbert Beebower1 set out to explain the importance of asset allocation versus manager selection as it pertained to pension fund returns. This influential study suggested that 93.6% of the variability in portfolio returns were explained by asset allocation over the sample of ninety-one large US pension funds. In the years since the study, there has been discussion about the validity of asset allocation accounting for so much of the investor’s portfolio return.

In 2000, Ibbotson and Kaplan published a paper in the Financial Analysts Journal entitled, “Does Asset Allocation Policy Explain 40, 90, or 100 Percent of Performance?2” The duo found that asset allocation policy explained 90% of the period-to-period variability of mutual funds returns, while it only explained 40% of the variability of returns between funds. The variability of returns between funds was mostly explained by active decisions, style preferences, and fees. In the twenty-six years since the Ibbotson and Kaplan paper, asset allocation has been influenced by globalization. Globalization may have dampened some of the diversification benefits due to domestic and international equities becoming more correlated. However, asset allocation still accounts for most of the investor’s return, in our view.

The RiverFront Approach: Strategic and Tactical Unite

At RiverFront, we view asset allocation as the primary driver of returns in our portfolios, while looking at the process through several different lenses, including a 'strategic' (long-term, i.e., seven years or longer) lens and a 'tactical' (shorter than one year) lens. Capital market assumptions (CMAs) aim to find the optimal asset allocation investment mix for a portfolio. At Riverfront, we create our own CMAs and adjust the asset mix depending on the time horizon for which we are optimizing the portfolio. At the other end of the spectrum, tactical asset allocation focuses on a time horizon of less than a year, typically 3 to 6 months. While we do not believe that investors can time the market, implementing strategic and tactical asset allocation together in our investment process allows for a smoother investment experience. We believe history has shown that equities have positive returns over long periods, so it is important that clients do not abandon their investment strategy after a period where they have experienced a large drawdown because it locks in the losses. Large losses jeopardize the investor’s ability to meet their financial goals. Hence, why we feel it is important to combine strategic and tactical asset allocation to try to mitigate large drawdowns in the stock market and keep our clients invested throughout market cycles.

Our strategic asset allocation process begins with developing capital market assumptions for stocks over a seven-year time horizon. Using historical market returns for each asset class, we assess how far they deviate from their long-term trend as one of several inputs. For stocks, we build bottom-up discounted cash flow models to evaluate future earnings and cash flow. Finally, we model path-dependent interest rate outcomes to determine the appropriate allocation to bonds and cash. Together, these inputs produce the asset class weightings for stocks, bonds, and cash.

RiverFront's tactical process underscores that asset allocation is not a "set it and forget it" exercise. Designed as a dynamic shock absorber, it adjusts the stock, bond, and cash mix for short periods to keep investors invested during uncertainty. The process allows the stock/bond allocation to swing up to twenty percentage points in either direction — becoming more bullish when undervalued assets gain upward momentum, and more bearish when overvalued assets encounter downward momentum.

While our strategic process seeks long-term value, our tactical asset allocation targets asset classes with sustainable momentum over 3-to-6-month horizons. Our research going back to 1927 found that the S&P 500 produces positive 3-month forward returns 64% of the time — meaning stocks go up more often than they go down. Long-term investors should therefore maintain a bias toward owning stocks to benefit from this positive payoff profile.

The Importance of Diversification

We believe that the asset allocation process is important because it allows us to build diversified portfolios that seek to limit idiosyncratic risks that can create undue volatility that inhibits investors from hitting their investment goals. By limiting the volatility through strategic asset allocation, year-to-year portfolio returns are more predictable, which creates the ability for portfolios to grow through compounding. Simply put, asset allocation helps to mitigate large drawdowns that require taking additional risk to stay on target of hitting a financial plan.

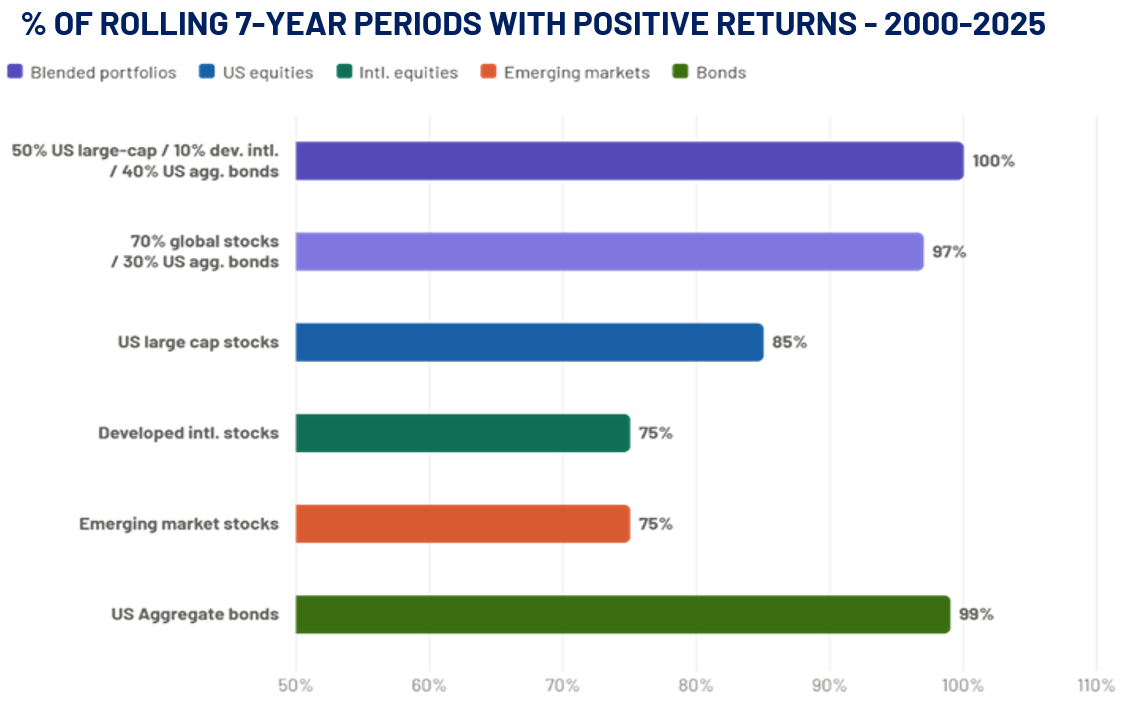

To put this concept in perspective, we looked at rolling 7-year returns for the major equity and bond indices to analyze the percentage of time over the past 25 years that the asset class had a positive return (see chart, right). The benefits of diversification become clear when examining blended portfolios. A portfolio combining 50% US large-cap stocks, 10% developed international stocks, and 40% US Aggregate bonds produced positive returns in 100% of rolling 7-year periods between 2000 and 2025 (see top purple bar on chart). Similarly, a broadly diversified portfolio of 70% global stocks and 30% US Aggregate bonds (2nd purple bar down on chart) was positive in 97% of those same periods. These percentages are higher than all of the equity asset classes in isolation. These figures reinforce a simple but powerful truth: diversification doesn't just reduce risk — it dramatically improves the consistency of outcomes for long-term investors.

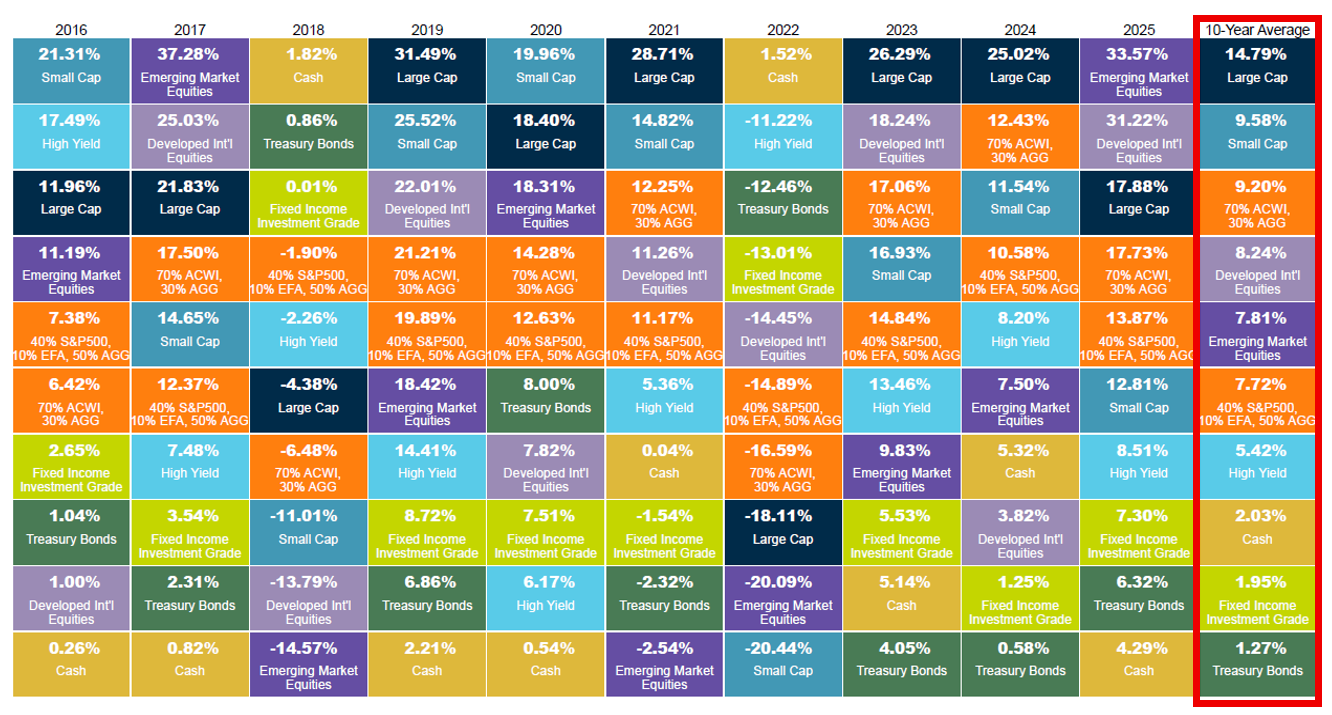

LEADERBOARD CHANGES BY YEAR, BUT DIVERSIFICATION POWERS THROUGH OVER THE LONG-TERM

Focusing on the last ten years, the accompanying chart below highlights the importance of asset allocation…because no two years are the same. For example, we can focus on the path of Emerging Market Equites (dark purple box) in the table below over the past 10 years. As you can see, it fluctuates widely throughout the chart, spending two years atop the leaderboard as the best asset class and two years at the absolute bottom. The chart emphasizes the importance of the asset allocation process being continuous and not a one-and-done proposition, because no asset class dominates every year.

Diversified portfolios tend to benefit from compounding over long periods of time, which makes the subtle changes between asset classes important to the asset allocation returns. You can see a simple blended portfolio of 70% ACWI (global equities) and 30% Aggregate bonds (orange box)…it’s never at the top in any given calendar year. However, through a decade-long market cycle (2016-2025), it ends up having a 10-year average performance (see right column on table, highlighted) similar or better than everything on the table except US stocks… despite possessing a meaningful volatility ‘shock absorber’ in the form of US bonds. This is what we’d call the power of diversification.

Conclusion:

Asset allocation remains the primary driver of portfolio returns forty years later, because each asset class (stocks, bonds, and cash) inherently has characteristics that set both a floor and ceiling for returns based on their perceived risk level. By creating an asset allocation, investors get an investment mix that captures the bulk of the overall return before security selection is considered due to the asset level return profile.

As previously stated, no asset class wins every year — and that's exactly why diversification works. Because performance leadership rotates unpredictably across asset classes year- to- year, a well-diversified portfolio captures broad market returns, reduces volatility, and enables the power of compounding. Trying to pick winners annually is a losing game, in our view; owning the right mix consistently is not.

Asset allocation should be dynamic, not static. RiverFront's dual approach — combining long-term strategic allocation (7-year horizon) with short-term tactical adjustment (3–6 months) — is designed to keep investors in the market through turbulent periods. The biggest risk is not a bad year; it is abandoning a sound strategy at exactly the wrong moment and locking in losses that derail a long-term financial plan.

At RiverFront, we partner with financial advisors that determine the client’s investment objectives and risk tolerances, and we use our asset allocation process across our portfolios to help reach those objectives. We believe asset allocation should be dynamic, combining strategic and tactical to adjust for the different market environments.

1 Brinson, Gary P., L. Randolph Hood, and Gilbert L. Beebower. "Determinants of Portfolio Performance." Financial Analysts Journal, vol. 42, no. 4, July–Aug. 1986, pp. 39–44.

2 Ibbotson, Roger G., and Paul D. Kaplan. "Does Asset Allocation Policy Explain 40, 90, or 100 Percent of Performance?" Financial Analysts Journal, vol. 56, no. 1, 2000, pp. 26–33.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 05.19.2026 | Strategic View

Authored by

-

Kevin Nicholson CFA®

Global Fixed Income CIO | Partner