Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- We believe AI will drive gains in US productivity and GDP over the next 5-to-7 years.

- Investors should remain humble and flexible, given the uncertainty surrounding AI adoption and scalability.

- RiverFront remains overweight tech companies levered to AI, but we expect significant price swings from here.

Every once in a long while, an investment theme comes along that has the potential to change the way we think about everything…with incalculable political, societal, economic and investment implications. For the last few years, we have been thinking about, writing about and investing in just such a theme: Artificial Intelligence (‘AI’). This month we will be publishing a two-part AI ‘deep dive;’ today we will be covering AI’s broad implications on the US economy. Next week, we will dive deeper into more specific corporate earnings and cash flow, sector, and industry implications for stock investors.

Simply put, we believe AI - in both its current and future iterations - is a technological advance as significant as the internet, cloud computing and the personal computer. It is also potentially even more significant, since its end game - Artificial General Intelligence, or ‘AGI’ - when computers can understand, learn and apply knowledge at a human-like level of intelligence - will likely have profound implications for society.

There is a race among US and Chinese technology companies to advance the capabilities of AI for geopolitical and economic advantage. We believe that since the major US companies have so much cash, and Chinese companies have the backing of the government, spending on this ‘race’ will continue for the foreseeable future at a breathtaking pace.

It appears to us that the US currently has the technological edge, but victory is far from assured and the stakes are high. Thus, the mindset of big US tech companies appears to be both: ‘If we build it, they will come’ and ‘we can’t afford to be left behind.’ This could lead to overbuilding in the early years… as happened with miles of railway in the Industrial Revolution, or fiber optic cable in the ‘Dot.com’ era. For investors, the explosive growth of AI is now widely known and priced into shares, so the critical judgement from here is whether the buildout will match or exceed the pace of adoption. After a deep dive into the available research from academics, technologists, and Wall Street, it is clear to us that the range of forecasts is extremely wide, and we likely won’t have clearer answers for several years. Humility and flexibility will be our friends as we navigate this rollercoaster of investor excitement and potential disappointment.

TABLE 1: RiverFront’s Base, Bear and Bull Cases of AI’s Impact

For this reason, we are choosing to apply a scenario framework that allows for three potential outcome ranges through the next business cycle, defined by RiverFront as the next 5-to-7 years: 'Base’, ‘Bear’ and ‘Bull’ Cases, (see Table 1 above). Currently our highest-probability ‘Base Case’ is a relatively optimistic one. This optimism is reflected in RiverFront’s portfolio positioning, as we are overweight large-cap, highly-profitable tech companies that we believe benefit directly and indirectly from the explosive growth of AI. However, we acknowledge that from here, the ride is likely to be a volatile one for investors.

AI’s Potential Effect on US GDP Growth: A View into Capital, Labor, And Productivity Impacts

Understanding the potential impacts AI may have on US economic growth over the next 5 to 7 years is crucial for investors, in our view. Economic growth has high long-term correlations to corporate earnings trends… and thus to stock prices.

As background, GDP growth calculations generally are sensitive to changes in input factors such as capital (infrastructure like machines or factories) and the size of the labor force. However, productivity – how efficiently this labor and capital can be combined - is arguably the most crucial long-term question to answer with regard to AI’s ability to reshape the global economy.

Changes in Capital: A positive effect for now. Currently capital in the AI world is expanding rapidly, as AI requires huge investments in physical infrastructure like data centers. A Reuters article from October 31 quotes Goldman Sachs estimates of $3 trillion to $4 trillion AI-related infrastructure spending globally by 2030. This spending is necessary because the power required for generative AI demands a massive increase in our nation’s electricity generation grid. An April 2025 estimate by McKinsey suggests that close to $7 trillion in data center capacity will need to be built by 2030 to keep up with the demand for computing power...with over $5 trillion in capacity just due to AI. In 2025 alone, AI ‘hyperscalers’ such as Microsoft, Amazon, Meta, and Alphabet are expected to spend roughly $350 billion combined on data centers.

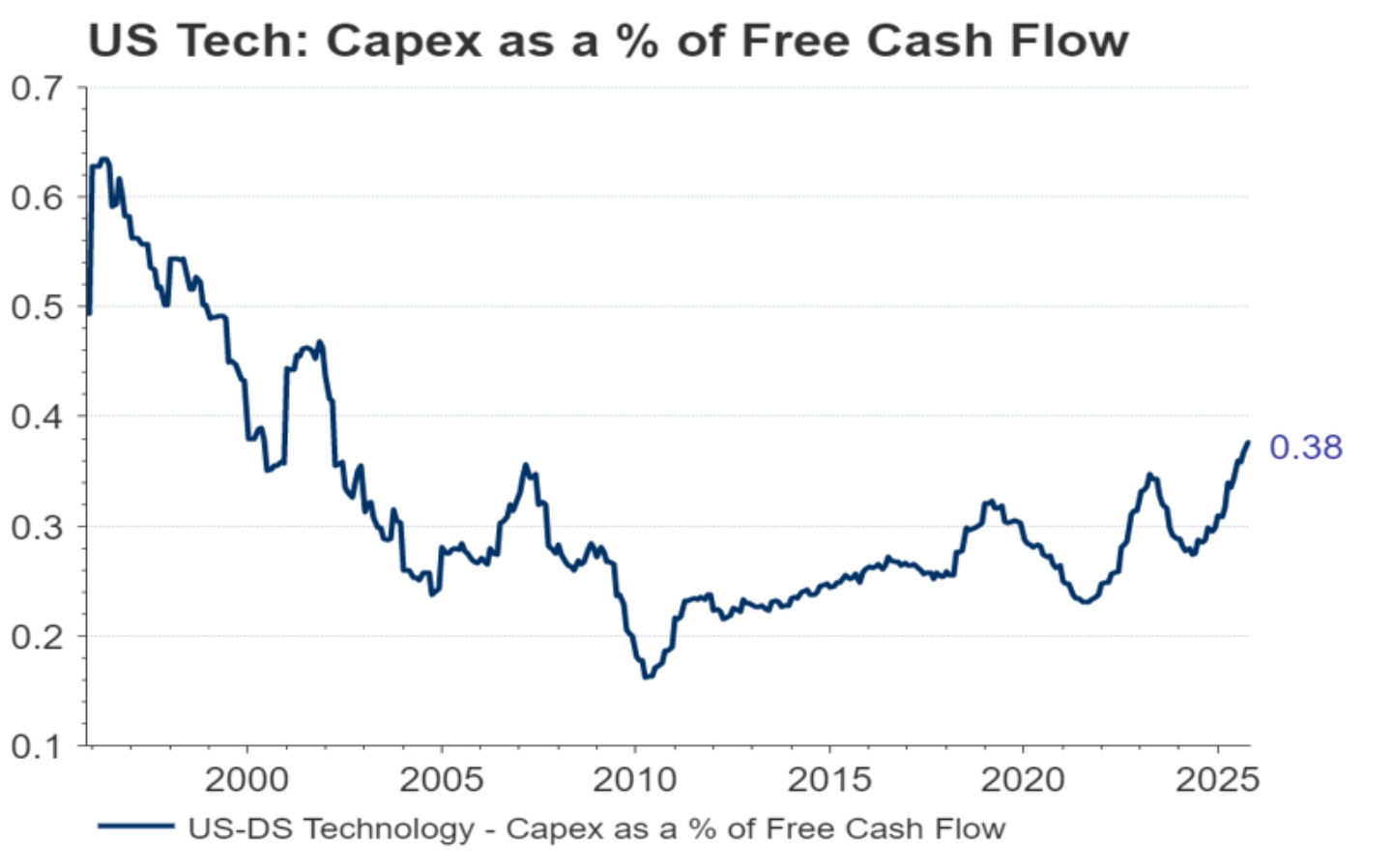

CHART 1: Tech Cash Flows Strong Enough to Fund AI Buildout

All of this spending acts as a money ‘multiplier’ as it works its way through the economy. Thus, we believe capital spending is likely to be stimulative to GDP in the near-term, though longer-term questions remain for this trend should AI adoption not continue to scale. Goldman Sachs estimates AI investment is currently less than 1% of U.S. GDP, well below the 2% to 5% seen during the peak of the electricity and dot-com booms. This suggests to us that, despite concerns from investors around an ‘AI spending bubble’, there is room for the AI spending boom to continue or even accelerate in the near-term.

How is this investment being funded? To this point, the buildout has primarily been funded by well-heeled tech companies via their enormous balance sheets and cash flow generation. These have included AI ‘hyperscalers’ such as Microsoft, Google, and Amazon, as well as by software and chip manufacturers themselves, in moves that resemble vendor financing.

While the ‘circular’ nature of these deals raises some eyebrows, the nature of the funding source – strong cash flow - gives us confidence that the AI buildout won’t lead to a debt crisis like the housing boom in 2008. The US public tech sector capex-to-free-cash flow ratio, while growing rapidly, is still reasonably low relative to history (Chart 1, above).

However, the buildout ecosystem has grown more opaque recently, with increased debt funding sourced via private credit deals and special purpose vehicles (SPV) from smaller companies, private equity, and asset managers. This part of the buildout bears more scrutiny and close monitoring, in our view.

For all of those reasons, we view capital formation as generally positive to GDP growth across our 5-to-7-year forecast horizon, but not necessarily uniform. Some years capital spending may be bigger than others, dependent not only on AI demand, but also US credit conditions, monetary supply and overall economic health.

Changes in the Labor Force: Likely to be slightly negative in the near-term. We must also take potential labor force changes into account when analyzing a potentially disruptive technology like AI. It is here where we are forced to temper our enthusiasm a bit; in all three of our cases, labor force participation drops in the near term due to the disruptive AI forces of labor substitution, especially for entry-level knowledge workers.

A 2025 UPenn/Wharton study suggests that for more than a quarter of U.S. employment, AI could perform between 90% and 99% of the work required with minimal oversight. Perhaps not surprisingly given this conclusion, Goldman Sachs estimates that AI could expose some 300 million jobs to automation over time.

We believe there is a long-term silver lining for workers as it relates to AI, however. In past eras of productivity breakthroughs such as the US Industrial Revolution (1790-1920), negative near-term effects on unemployment eventually were dwarfed by new job creation, often in fields and disciplines heretofore unknown to society. In fact, we believe this emergence of new occupations is one of the main drivers of long-term employment gains. To this point, a MIT study from 2018 cited that 60% of today's U.S. occupations did not even exist in 1940 . We suspect AI will be no different in the long-run; however, across our roughly 5-to-7-year forecast horizon, we believe the net effect to employment will be neutral to slightly negative in our Base Case.

CHART 2: Adoption Rate of AI Faster Than the PC or the Internet

Changes in Productivity: Positive - AI adoption growing quickly in high relative labor cost industries. First, in order for productivity to be meaningful, we believe usage of AI must be fairly widespread. On this front, there is encouraging news: early indications of AI usage suggest lightning-fast adoption. Research conducted in September 2024 by the St. Louis Fed suggests that AI has already reached faster adoption levels at this point than either the Internet or the personal computer (PC) at similar points in their gestation (Chart 2, above).

This increases AI’s ability to have a meaningful positive impact on productivity over time. Encouragingly, adoption appears to be happening fastest in industries with high relative labor costs – including software development, digital content creation, consulting, and legal and financial services. This suggests to us that AI adoption has the potential to be a real productivity enhancer at the corporate level.

But just how much productivity growth should we assume? A literature review of credible AI research over the last few years from academia, consulting, think tanks and investment banks suggests a wide range of views and estimates, from minimal (barely above zero) to game changing (over +1% increase in productivity per year for the next decade.

CHART 3: We Are Optimistic About AI's Productivity Boost

With all prerequisite humility, RiverFront’s ‘House View’ is a bit more positive than consensus; we expect AI to improve US productivity between +0.5%-1.0% a year in our Base Case, with a central tendency of about 0.6% per year (see Chart 3, right). That represents a significant improvement for a total US productivity growth trend that’s currently running around +1.5-2% annually. Holding capital and labor constant, this change in productivity could translate directly to a similar gain in GDP growth.

When you combine the somewhat offsetting effects of both productivity gains and downward pressure on the labor force, our Base Case is that AI could boost US GDP by roughly between a quarter-point and half-point a year above its’ current trend over the next 5-to-7-years. This is a boost we’d term ‘significant’ but not necessarily ‘revolutionary.’

AI’s Impact on Inflation - Eventually Disinflationary in All Three Cases

However, the effects of AI don’t just stop at economic growth; our belief is that this technology will also have significant effects on inflation as well, and thus Fed policy. If AI technology increases productivity, some of that benefit will be passed on to consumers. Offsetting this will be considerable increases in the cost of electricity, already being seen in areas where data centers are concentrated. Power companies will have to invest heavily in new production and regulated utilities are usually allowed to pass that cost to consumers. A shortage of workers and explosive demand will raise prices in the construction industry. On balance we think the disinflationary forces will eventually win out.

Regarding employment, while AI will create jobs over time, we think it will be disruptive to employment, and will increase unemployment initially, as discussed above. Therefore, there is a credible scenario that both sides of the Fed’s mandate will argue for lower interest rates, and that inflation hawks on the Fed will not have a case to make against a Trump-appointed Fed chairman determined to lower rates. Should this occur, it will be fuel to increase corporate earnings and stock prices in our view.

CONCLUSION: AI Will Be a Positive US Growth Driver Going Forward

As investors, we are optimistic about the potential for AI adoption to lead to a pronounced increase in productivity. We are confident that the race to adopt AI means that spending on building AI architecture and infrastructure will not slow down in 2026… and probably not for several years. This is reflected in the relatively high collective probability we place on an outcome somewhere between our Base and Bull Case over the next 5-to-7 years (Table 1, page 1).

We have less clarity on the pace and success of adoption, but early signs are encouraging for those industries where it is most suitable. In addition to developing AI, technology companies are one of the biggest users, making the sector continue to look attractive in our opinion. Given the uncertainty of how AI demand will play out, the huge commitment the big technology companies are making, the current optimism built into their share prices, and the future potential of AI, we believe investors should expect significant price swings.

We will try to navigate these swings as best we can, maintain our optimism as long as we feel it is warranted, and at the same time prepare our clients emotionally for this volatility. Investing in AI will not be for the faint of heart…but it is likely to remain lucrative for the time being.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 11.11.2025 | Strategic View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist

-

Rod Smyth

Vice Chairman