Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- Concentrated positions are associated with high portfolio risk.

- Covered call strategies can generate income to help diversify concentrated portfolios.

- Financial advice is key to solving issues like concentration.

A couple of months ago, we discussed in our Strategic View how more nuanced investment problems require equally nuanced investment solutions. That piece focused on income-oriented portfolios within a goals-based framework. This week, we are tackling another complex challenge: concentrated stock positions.

The Risk of Concentration

When a single stock becomes a large portion of a portfolio, the investor’s goals become inextricably tied to that stock’s performance. This ‘concentration’ risk manifests in two primary ways: elevated portfolio volatility and increased underperformance risk.

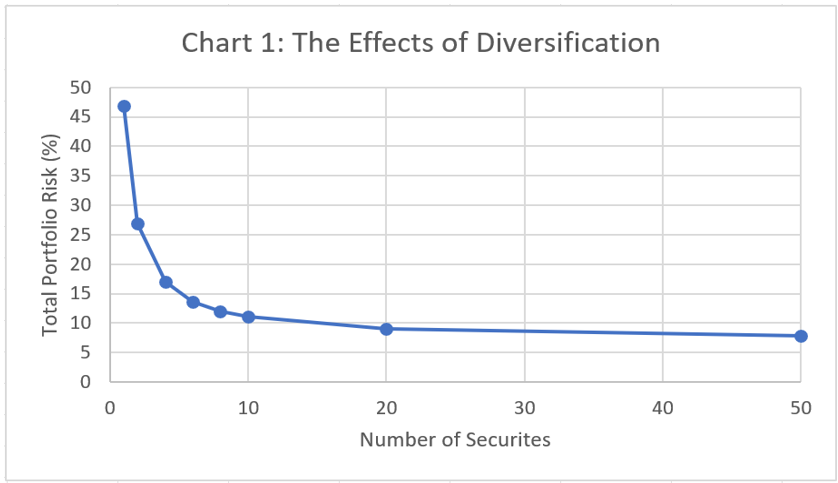

First touching on volatility risk, research by Edwin J. Elton and Martin J. Gruber in Risk Reduction and Portfolio Size: An Analytical Solution examined the relationship between the number of holdings and total portfolio risk. Chart 1 illustrates their findings.

According to the study, diversifying from a single concentrated position to a diversified basket of roughly twenty stocks reduces expected portfolio risk from just under 47% to under 9%, removing much of the idiosyncratic (company-specific) risk, though systematic market risk remains. Put more simply, a single stock portfolio is expected to have a much larger year-to-year variance in returns. This variance equates to large fluctuations in an investor’s wealth, when a single stock makes up a large portion of their portfolio.

Moving to underperformance risk, we must take a long-term view on our concentrated stock. If the goal is to hold this position for 20 or more years, we must consider both the risk of the stock having negative returns, as well as the opportunity cost of holding the stock instead of a more diversified portfolio. In fact, let’s step back in time twenty years or so years to 2005. At the time the largest companies in the S&P 500 were GE, Exxon Mobil, and Citi. The decade prior to 2005 was a good one for this trio, with an average total return of 20.5% per annum. This creates a nice parallel between these stocks and several modern-day growth stocks.

Now, let’s step forward through time. Due to GE splitting into three entities, we will set them aside. If we look at the returns of Exxon and Citi from the start of 2005 until today, we end up with a mixed bag. Exxon averaged an annualized return of 13.3%, while Citi’s annualized return was -5.6%. So, holding a concentrated position in one name would have most likely allowed an investor to reach their goals, while the other would have caused a loss of wealth. However, when we introduce the S&P 500 into the mix we begin to see the total risk. Over this same period, the S&P 500 averaged 17% per annum. Even the successful concentrated position was unable to keep up with the diversified basket. We can conclude from this anecdotal exercise that even if a stock has a strong bull run, its future returns are not guaranteed, especially when considering them relative to a diversified basket1.

The Added Complexity of Taxes and Emotions

Given the risks we have laid out, it may seem simple to say, “let’s trim or completely sell this concentrated position.” Unfortunately, taxes often create a major hurdle. For the vast majority of concentrated positions, the position became concentrated through outsized price appreciation, rather than an intentional purchase at that weight at the outset of investment. As a result, the cost basis is typically much lower than the current market value, meaning even a modest trim could trigger a significant capital gains tax liability.

Beyond taxes, concentrated positions often carry sentimental value. Most common paths to concentration - inheritance, long-term accumulation, or equity compensation - leave investors understandably uneasy about selling. Additionally, investors may worry that when they sell a concentrated position, they are missing out on the upside potential of that stock (“FOMO” as it is colloquially known). As such, having a diversification plan - and sticking to it - is important to help remove these emotions from the decision-making process.

Using Covered Calls: The Skinny

We would like to briefly provide a very high-level explanation of covered calls before providing a deeper dive. In the simplest terms, a covered call swaps a stock's future upside for income today. This can be attractive to an investor that has a concentrated position and the need for income or diversification. With any covered call strategy, there is a risk that an investor must sell their stock (and incur capital gains), though certain strategies can mitigate this risk. If this sounds intriguing, your financial advisor can discuss this further with you, as options can sound complicated at first blush. We will now do a deeper dive into the mechanisms of how they work.

Covered Calls: A Deeper Dive

Providing a little more color to our above comments, a covered call is when the holder of a stock ‘writes,’ or sells, call options on that stock. These call options give the buyer of that option the right (but not the obligation) to ‘call,’ or purchase, a security at a pre-specified price (known as the ‘strike price’) before the option’s expiration date.

This means when an investor initiates a covered call position, they are sacrificing future upside on the stock above the strike price. In return for limiting their upside, they receive income at the initiation of the option. In other words, a covered call strategy can transform the total return expectations for an individual stock by capping the price appreciation opportunities, while increasing the income generated by the position. It is important to note that covered calls do not eliminate the downside risk of owning the underlying stock; the investor remains fully exposed to declines in the stock’s price, less the income received. Additionally, there is always a risk that the security on which the call is written will be purchased by holder of the option. While this risk is able to be mitigated through purchasing an identical option to the one they sold (“buying to close”), this transaction will reduce portfolio income and may require cash deposits to cover the cost of the transaction. Even with this mitigation, risk of the stock being purchased cannot be eliminated.

The income generated by covered calls can then serve as a tool for gradual diversification. Each income payment can be reinvested into a diversified basket of stocks or an ETF, creating a systematic dollar-cost-averaging stream. While this method of diversification tends to be gradual, it can fit well within a 10–15-year timeline (or longer, depending on the investor’s preferences), with the options income providing some volatility dampening in the interim.

For investors willing to trim their concentrated position directly, options income can also help offset the resulting capital gains taxes. That is, the income from the covered call strategy can be earmarked for tax liabilities, and a corresponding portion of the concentrated position sold at year-end so that the income covers the incremental tax obligation.

Adjusting the Pace of Transition

One of the key features of a covered call strategy is the ability to adjust the strike price relative to the current market price, which controls the aggressiveness of the transition:

- Strikes closer to the market price (“closer to the money”) generally produce higher premium income, offer less upside capture, and increase the probability that the stock will be “called away”. This approach may suit investors willing to accept a larger near-term tax burden in exchange for a faster transition.

- Strikes further from the market price (“further from the money”) generally produce lower premium income, preserve more upside participation, and reduce the probability of being “called away”. This approach may appeal to investors who prefer a more gradual transition or who want to retain more exposure to the stock’s potential appreciation.

Regardless of which approach is chosen, it is important that the diversifying investments complement (rather than replicate) the exposures of the concentrated position. For example, if the concentrated position is in the technology sector, the diversifiers should lean toward other sectors or styles to help avoid inadvertently doubling down on the same risk factors to which tech is exposed.

Risk Management of Covered Calls

Covered call strategies require frequent monitoring and a thorough understanding of options markets. Without active management, there is a risk of unintended assignment, meaning the stock could be called away at an inopportune time, potentially creating adverse tax consequences. While proper risk management can significantly reduce the likelihood of unintended assignment, it cannot eliminate this risk entirely. Additionally, in rapidly rising markets, a covered call strategy will underperform an uncovered position because the stock’s upside is capped at the strike price. Investors should also consider the transaction costs associated with writing and managing options positions, as well as the tax treatment of options premiums, which may differ from the treatment of long-term capital gains.

The Value of Advice: Complex Problems Require Custom Solutions

Concentrated positions create undue idiosyncratic risk. In our view, thoughtful diversification can help reduce this risk and increase the likelihood of an investor reaching their long-term goals. Covered call strategies provide one potential avenue opportunity to generate income to help fund the diversification process over time.

Echoing our conclusion from our earlier Strategic View, when facing complex financial issues, the importance of financial advice cannot be overstated. Without a financial advisor, identifying, quantifying and addressing these problems can be difficult. An experienced advisor can draw on a range of tools and strategies to craft a solution tailored to each client’s unique circumstances, risk tolerance, and objectives.

At RiverFront, we offer both model and custom portfolio solutions to support financial advisors and their clients in addressing complex issues. For concentrated positions specifically, our model portfolios offer diversified exposures, while in certain instances we are also able to employ covered call strategies designed to facilitate a transition away from concentration.

1 Stocks mentioned are for illustrative purposes and not intended as recommendations. You cannot invest directly in an index.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 05.12.2026 | Strategic View

Authored by

-

Dan Zolet CFA®

Associate Portfolio Manager