Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

The dangers to both public health and the economy are intertwined with COVID-19 and so it continues to dominate our internal debate. Since the current situation is unprecedented in our lifetime, our investment team is humble about what we don’t know, open to revising our forecasts, and calmly gathering information in order to dimension the likely paths of economies and markets from here. Below we set out 3 scenarios and establish our current base case. Given the importance of remaining open to change, we want to communicate that we recognize the downside potential of the pessimistic case and our risk management plans reflect that.

This past week, we have seen both the scale and challenges of COVID-19 worsen in Western countries and continue to improve in Asia. We have also seen policymakers reflect an understanding of the dangers to citizens and the economy in both announced response measures and in their commitment to do whatever it takes to get ahead of the problem.

Thus far, investors, trying to gauge the scale of the problem, have judged that the response is not yet sufficient – last week global stocks fell another 13% and corporate bond yields rose, reflecting increased fears of defaults and downgrades. Ed Hyman of Evercore ISI (a forecaster with access to weekly proprietary survey data), is suggesting a decline in GDP of 5% or more from Q1. That is twice the decline experienced in the 4th quarter of 2008. While his forecast is more dire than many of his peers, as a ballpark estimate it does not seem unreasonable to us. We therefore recognize how negative the data will be in the coming months.

Our Base Case: A U-Shaped Economic Path

In our view, how the 3rd and 4th quarters play out will be more important than the 2nd quarter for stock prices and will be a function of the success of virus containment and the size of the policy response. Our working assumption is that the authorities in Europe and the US are currently behind but catching up quickly. In terms of the economic trajectory, think about a ‘U’ shape, but one that is not perfectly symmetrical. Instead, we believe we are likely to see weaker economic data, then a period of weak but static activity, followed by a gradual recovery. Our base case assumes the magnitude and severity of the decline is mitigated by massive government spending and financial injections to “buy time” and keep households and businesses afloat during the stay-at-home period. Furthermore, our base case assumes that effective quarantining and social distancing by households reduces the pressure of the virus on our healthcare system, but also elongates the economic bottoming.

We believe our balanced portfolios are positioned cautiously, with the team looking for the right time to add to stocks if either:

a. Greater value emerges due to further price declines, and/or

b. We can start to quantify the magnitude of the downturn and the adequacy of the response. There is low visibility of both at present.

Following the very sharp declines since the peak just one month ago, we believe current levels of both risk assets (stocks and corporate bonds) and safer assets (Treasury bonds) reflect a fair amount of bad news. We are factoring in a further 10-20% downside if the situation deteriorates faster than the policy response. Thus, while we expect stocks will be higher than current levels 12-18 months from now, short-term risk remains high enough to keep our cautious positioning. We also recognize that when visibility of better times becomes clearer, stocks will turn up sharply and it will be difficult to perfectly time the bottom. We expect continued significant daily and weekly swings in prices while the outcome is so uncertain.

The Pessimistic Case: A L-Shaped Economic Path

In this scenario investors, the COVID-19 response team, and policymakers have not yet appreciated or can’t get ahead of the magnitude and duration of the problem. We believe that about 20% of the economy has seen revenue collapse and, in some cases, ceased altogether and most businesses have seen a sharp decline in revenue, thus time is critical. In terms of the economic trajectory, think about an ‘L’ shape, where the length of the period of reduced activity is protracted as virus containment does not mirror the experience in Asia and rather takes longer than investors currently imagine. The challenge for countries such as the US as it relates to COVID-19 is the cultural importance placed on individual freedom of choice. Some other cultures have historically placed a greater emphasis on the wellbeing of the group versus individual freedoms, making it easier to manage situations that require large scale cooperation. This scenario assumes the virus containment trajectory will not mirror that in Japan, Korea, or China.

In the pessimistic case, we believe stocks are likely to decline 20% and potentially more from current levels. Corporate bond yields will rise further anticipating a higher level of defaults. In this environment it is too early to assess where an eventual recovery might take stocks and bonds in 12-18 months.

The Optimistic Case: V-Shaped Economic Path

This is the scenario whereby fears of the magnitude of the virus prove to be overdone, the stay-at-home period is measured in weeks not months, and the policy response proves to be more than adequate. In terms of the economic trajectory think more about a ‘V’ shape: a sharp, 1-2 quarter economic shock, followed by a speedy recovery as activity returns to more normal levels. After a 30% decline in stocks, a successful process of virus containment and policy response allows the lows to be around current levels. In an optimistic scenario, stocks quickly recover more than half their losses and return to February 2020 levels over the next 12-18 months. We view this as the least likely scenario currently.

Current Portfolio Positioning: Cautious about stocks with a strong preference for the US over the Eurozone

The degree to which we have taken defensive measures in our balanced portfolios varies with their mandate and targeted timeframe. Our shorter investment horizon portfolios (5-7 years and shorter) are positioned most cautiously.

Selection is another important aspect of our positioning. All our portfolios have a strong preference for US stocks over other developed markets. In simple terms, we believe that while the efforts of the US to manage the public health crisis are no better, the US track record of dealing with economic crises since the 1980s has been significantly better than Europe or Japan. This applies to both policymakers and businesses. US companies dominate the successful 21st century business models that we believe will weather the current situation better and come out stronger. These businesses have revenue streams that will be less impacted by the stay-at-home recession and workforces that can work remotely more easily.

Rapid Response by the Fed…but European Central Bank slower to act

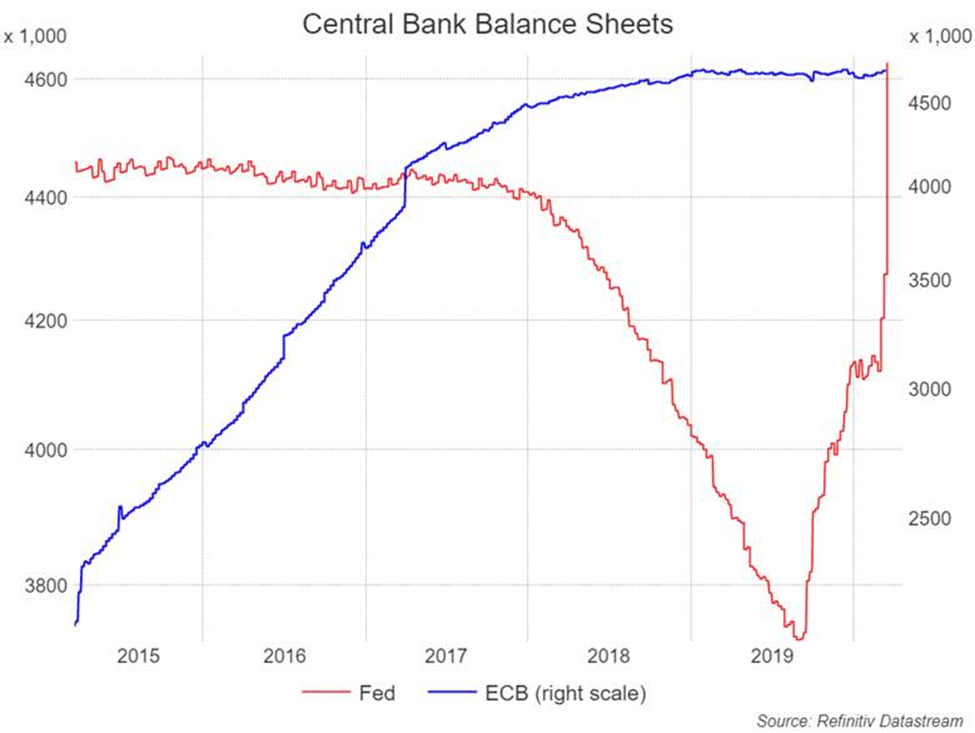

Agreeing on and implementing Government crisis support programs is challenging in any democracy, especially large economies like the US and the eurozone. We already see a faster response from the US in both fiscal and monetary policy than the eurozone, as in prior crises. The Federal Reserve led the world in creative monetary policy following the 2008 financial crisis and our chart right shows how much more quickly the Federal Reserve has reacted in recent weeks compared to the European Central Bank (ECB). The Fed had allowed its balance sheet to gradually decline (as the bonds it purchased matured) until last summer when economic activity started slowing and the Fed started ramping it back up. Its massive expansion in the last few weeks shows an acute awareness of the challenges to liquidity and economic activity brought on by COVID-19 and the action to back it up.

Download 03.23.2020 | Weekly View

Authored by

-

Rod Smyth

Vice Chairman