Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

The US is Still the Economic ‘King of the Hill’

SUMMARY

- US has maintained its economic dominance over the past year.

- We think this will continue due to stimulus and vaccine availability.

- We remain overweight US stocks in our balanced portfolios.

At RiverFront we recognize that, while international markets are priced to deliver better long-term returns than the US, cheap prices are not a timing signal but rather a ‘condition’. The ‘condition’ of cheaper valuation, in our opinion, requires a ‘catalyst’ in order for this value to be realized in the market. Otherwise, a cheap asset class can be simply a ‘value trap’, frustrating investors waiting for fundamentals to turn. This is particularly poignant with regard to countries outside the US, many of which continue to struggle with fractured politics and rigid labor markets along with the corruption and opacity often found in emerging economies. These struggles have led international equities to consistently underperform the US over the last decade (chart, below).

Thus, asset allocators are constantly forced to weigh the lower valuations found overseas against the distinctly worse structural and cyclical fundamentals that exist outside of the US. Is now the time for international value to finally be realized? The weight of the evidence, in our opinion, still points to maintaining an overweight to US stocks for the time being.

US: Stronger Economically

First, there is no getting around the fact that the US economy was stronger heading into the pandemic and remains stronger coming out of it. US Manufacturing sentiment, as gauged by the ISM Manufacturing Index survey, just hit its highest levels in over 30 years (shown in the chart, left), fueling stronger corporate earnings revisions and stock prices, in our opinion. US housing, retail sales, and consumer sentiment also remains remarkably strong in the US.

We think this strength is likely to continue. The International Monetary Fund (IMF), for example, recently released their projected 2024 global GDP forecasts; interestingly enough, the US is the only large economy in the world in which their GDP estimate is actually higher post-pandemic than it was before (source; IMF World Economic Outlook, April 2021).

Why Is the US Stronger?

Flexible US labor markets and a focus on shareholder returns have led to both higher levels of productivity, as well as faster productivity gains over the last few decades. In addition to these structural advantages, we believe the US currently enjoys a number of cyclical advantages. These relate to the dramatic response of US policymakers to the pandemic in the form of monetary and fiscal stimulus. The stimulus has caused aggregate money supply to grow 25% year-over-year, as compared to ~10% in other developed economic blocs such as the Eurozone, Japan, and China (see chart, right).

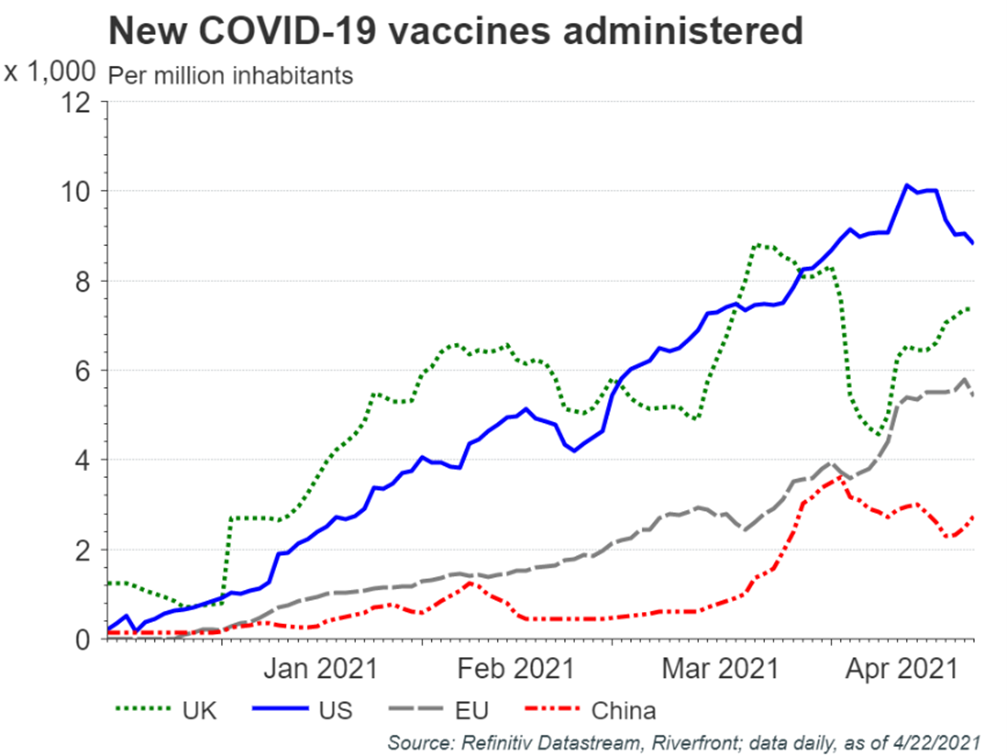

Another cyclical advantage, in our opinion, has been a more organized and widespread vaccine distribution network than much of the rest of the world (see chart, right). Broad vaccine distribution is allowing the US economy to recover more quickly and more sustainably, even as new variants threaten safety and economic growth in other parts of the world. We would note that large emerging economies such as India and Brazil are now seeing COVID-19 infection rates spike, a disturbing turn of events.

Potential Catalysts for Better International Performance

Our recently released long-term Capital Market Assumptions (CMA) analysis suggests that we expect developed international and emerging market equities to produce superior returns to the US over the next 7 years, in our base-case scenario. However, as we state above, unlocking this value will require catalysts. Potential catalysts include: a continuation of the global economic growth rebound, a continued move higher in global interest rates, a weakening of the US dollar, and/or any widespread improvements on vaccine distribution in large economic blocs such as the Eurozone and China.

CONCLUSION

With the weight of the evidence still pointing to the US as the ‘King of the Hill’ among global economies, RiverFront maintains an overweight to US stocks across our balanced asset allocation portfolios.

Download 04.27.2021 | Weekly View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist