Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- We believe the Fed will be resolute in confronting inflation…

- …and thus believe the bond market’s recent opinion change in the future path of interest rates is too extreme.

- Until yields reach higher levels, we are cautious around securities with interest rate sensitivity.

Even in normal times, we do not envy the Federal Reserve’s job of trying to balance the sometimes-contradictory goals of full employment and price stability. Since Chairman Jay Powell’s every utterance is scrutinized, one can appreciate the Fed’s communication dilemma as it stands today; lean too ‘dovish’, and inflation expectations may become unmoored, threating long-term price stability. Lean too ‘hawkish’ with higher interest rates…and threaten to exacerbate a ‘run’ on the banks and push the US economy into recession. Powell and the Fed are attempting to ‘tap dance on a tightrope,’ perfectly balancing the need for price stability with financial stability. Scarcely two weeks after guiding the public towards the possibility of a 50bp (0.5%) interest rate hike due to persistent inflation, the Fed was forced by the banking crisis (see last week’s Weekly View) to recalibrate towards a smaller hike and a less hawkish message in the Federal Open Market Committee (FOMC) meeting last week.

At that meeting, the Fed raised its fed funds target range by 25 basis points to 4.75-5.00% and left its median year-end rate projection at 5.125%. Bond yields plunged during the Q&A after Powell admitted that a pause in rate hikes was considered in the meeting and investors noted the shift in wording of the Fed’s statement where ‘may’ and ‘some’ replaced ‘ongoing’ in reference to rate hikes. The futures market now expects rate cuts to come as soon as the Fed’s July meeting, pricing over a 54% chance of a 25-bps cut.

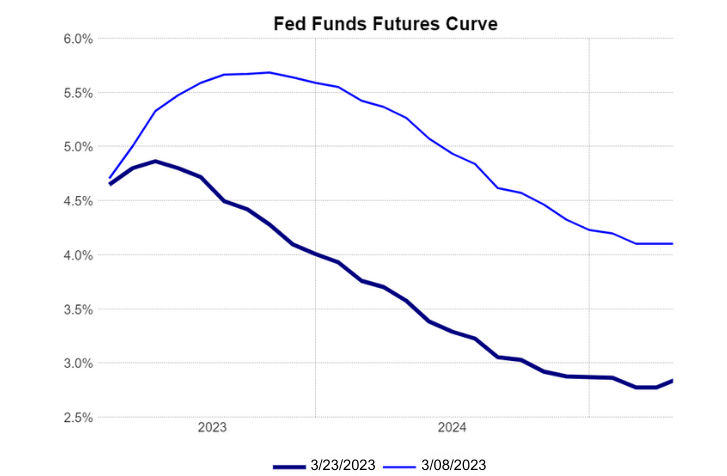

While we acknowledge this change of tone and that the probability of recession has risen, we believe the bond market’s substantial recent opinion change in the future path of interest rates is too extreme (see fed funds futures chart below).

This Fed tap dance naturally lends itself to misunderstanding and confusion with regards to future Fed policy. This is shown not only in the stock market’s recent intra-day volatility, but particularly in the disconnect between official Fed guidance – the median forecast in the infamous ‘dot plot’ of Fed interest rate projections – and the bond market’s implied path of future interest rates. We think the bond market is currently underestimating the Fed’s resolve around controlling inflation. Thus, we plan on remaining underweight interest rate sensitivity in the fixed income side of our asset allocation portfolios until yields reach higher levels.

Fed In Tap-Dance Mode…But Likely To Err On Side Of Inflation Control

Powell reiterated both the FOMC’s 2% inflation target and that participants don’t see rate cuts in 2023. When push comes to shove, we believe this Fed will ultimately prioritize price stability, and thus the interest rate path from here may be higher than the market is currently pricing in. The chart above of the fed fund futures curve (where today's interest rate expectations are represented by the dark blue line) depicts how much those expectations have dropped since the start of the banking crisis rate on March 8th (lighter blue line). Instead of lowering Fed Funds, we think the Fed will choose to support financial stability by continuing to use its balance sheet to create liquidity for banks and depositors.

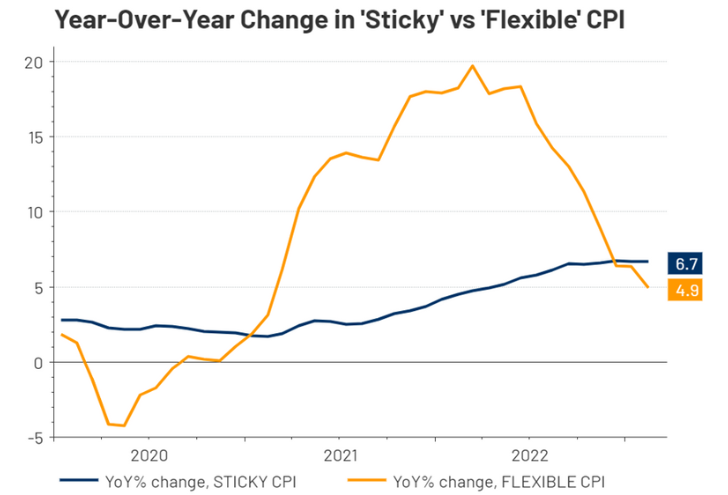

One important reason we think the bond market is underestimating the Fed’s resolve is the stubborn persistence of what the Fed refers to as ‘sticky-price inflation’, which makes up the majority of consumer spending (see chart, left). While more ‘flexible’ indicators such as fuel have corrected (orange line), stickier items such as rents, health care and education costs are still at elevated levels and not dropping as the Fed would prefer (blue line).

Portfolio Positioning - What Signals We Are Watching

With regard to overall stock weightings in our portfolios, we remain generally neutral relative to our policy targets. Given the uncertain economic outlook, we are favoring strong cash flow business models and carrying a slightly elevated level of cash for additional flexibility. This is our attempt to respect both the low visibility into the future state of the economy as well as the relatively resilient message of the stock market thus far. When visibility is this low, we think being neutral and nimble in our positioning is the prudent stance.

From a risk management perspective, we continue to monitor 1) the ‘message of the market’ (Technical Update section, below) 2) signals of stress coming from the credit and commodity markets, and 3) changes in the size of the Fed balance sheet.

From a credit & commodity perspective, neither market is showing signs of stress to us. For example, credit default swaps (CDS – the price of hedging default risk) for high yield bonds was virtually unchanged at +528 bps over the last week, still below what we view as the ‘cautionary zone’ of +600 bps. A move of CDS meaningfully above the +600 level may signal trouble for the sector and for overall risk-taking, in our opinion. Commodity prices generally remain depressed relative to 2022 levels. This suggests to us that global industrial growth continues to struggle, though flash Purchasing Managers’ Index (PMI) for March released on Thursday, indicated that services businesses in both the US and Europe were both in expansion and improving.

The Fed’s balance sheet is beginning to decline after a substantial recent increase. According to Fed data quoted by Bloomberg, two of the main Fed banking backstop facilities remained elevated, a sign that banks continue to feel stress from deposit outflow. These borrowings, however, did drop slightly from the week before, suggesting the ‘bank run’ we discussed in the Weekly View last week has not gotten worse.

Technical Update: Not Much Changed From Last Week…Stocks Remain Resilient Thus Far

Our technical view on markets has not changed much from our discussion in last week’s Weekly View. Despite the massive amount of intraday volatility in the stock market, the S&P 500 remains not far from its 200-day moving average at approximately 3940 and above what we view as important technical support at 3800 (see chart right). We continue to be impressed with the market’s resiliency in the face of a banking crisis.

The ‘Golden Cross’, a positive technical condition we have mentioned before– where the 50-day moving average has risen above the 200-day – is still in effect. Crowd sentiment has also continued to move deeper into pessimistic levels on both the shorter and longer-term time frames. This is usually viewed as a contrarian indicator where pessimistic readings are usually interpreted as positive for future market returns. However, we would have preferred that sentiment hadn’t fallen so far so quickly, as it calls into question the durability of the currently fragile recent uptrend. We expect the market to be range-bound for the time being, with a likely ‘decision box’ between 3800-4200, placing increased importance on either a break below or above these levels. We believe it will be difficult for the S&P 500 to rally substantially higher from current levels with the current financial headwinds and their impact on the economy.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 03.27.2023 | Weekly View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist