Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Investors are regularly inundated with scary headlines and dour forecasts that provide ample reasons to get out of the stock market. COVID-19 has been just that kind of catalyst. Combine that with a human’s natural ‘fight or flight’ instincts that kick-in when markets are volatile, and it is not unusual to find oneself holding too much cash after a big sell-off. Unfortunately, we believe few that find themselves in this position know what to do or have a plan for reinvestment. This week’s edition of the Weekly View is dedicated to the age-old question: ‘What do I do when I have too much cash on the sidelines?’

First: Swallow Your Pride

It is easy to celebrate successes; we believe that the best investors are those who know how to manage their mistakes. No one likes to admit that that they bought or sold for the wrong reasons, or that their hopes or worries were misguided. Many would prefer to stick with their decisions, even when the preponderance of evidence suggests otherwise. We believe investors need to get comfortable with the notion of ‘being wrong’ and moving on. If you sold stocks and the market did not go down, don’t beat yourself up over it. It is important not to compound a bad decision by failing to recognize when the facts change. In our view, ‘being wrong’ happens to all investors from time to time, but ‘staying wrong’ often makes the difference between investment success and failure.

Second: Determine Whether The Conditions Have Changed

If you sold stocks in 2020 because of COVID-19, it is important to recognize that the market will likely bottom well before macro-economic conditions improve. While no one can say for certain when the crisis will be behind us, we do recognize that a significant amount of ‘bad news’ may already be discounted into stock prices and an unprecedented amount of monetary and fiscal stimulus has already been implemented. For example, the Federal Reserve has lowered the Fed Funds Target Rate to 0%, restarted quantitative easing, and implemented large lending facilities to support market functioning. Congress has also passed the Coronavirus Aid, Relief, and Economic Security Act (CARES), which is the largest fiscal stimulus program in US history valued at $2.2 trillion. Monetary and fiscal policymakers across the globe have also enacted similar stimulus programs. According to Evercore ISI, nearly 300 stimulus measures have been announced in the past month around the world.

Third: Determine If Cash Undermines Long-Term Goals

In today’s low interest rate environment, large cash holdings could be an obstacle to funding future obligations, such as college or retirement. There is also a chance that long-term inflation rates rise with increased quantitative easing (QE) and generous fiscal stimulus programs; ultimately eroding purchasing power. When cash is accumulating to a reasonable level of interest in the bank or in a brokerage account, the long-term costs of sitting out can be less punitive. However, with short-term rates below inflation, cash on the sidelines provides negative real returns as it sits idle. If one needs their portfolio to grow, less risk-taking today could lead to greater risk taking tomorrow.

Fourth: Don’t Be ‘Penny-Wise And Pound-Foolish’

In our view, the longer an investor’s time horizon, the less important market entry points are. We believe the adage that successful investing is about ‘time in the market,’ NOT ‘timing the market’ holds merit for long-term investors for two reasons. First, over long-time horizons, the US stock market generally recovers its losses and continues to climb the ‘Wall of Worry’ (chart right).

Second, long-term investors benefit from a powerful force: compound interest. Compound interest allows a $100 investment growing at 10% annually to return more than 6 times an investor’s initial money after 20 years. We believe that investors who jump in and out of the market with significant amounts of their portfolios tend to be un-invested or underinvested more frequently and thus less likely to experience the full benefits of market recoveries or compound growth.

Fifth: Develop And Execute On A Plan

This is a critical part of our process at RiverFront. There are many reinvestment strategies that have shown historical efficacy. We believe that entry and exit strategies should be consistent with the investor’s goals and objectives and not solely dependent on one’s ability to accurately forecast market movements over short periods of time. Thus, when you deviate from your long-term goals, we think it is critical to have a plan for how you are going to return to them.

A Reinvestment Plan: Merging Into Traffic

Reinvesting into a market that could be rising can be similar to an activity that we are all familiar with: merging into moving traffic. For most of us, the action of merging requires little thought because it has become second nature. However, if we take a minute to examine it, we can identify three important steps that can be applied to the reinvestment process.

- Get Started: When you are merging onto the interstate you start the process immediately by getting up to speed. You don’t stop on the entrance ramp to wait for an opening because if you did you would lose all of your momentum (and your nerve). Likewise, when reinvesting cash, we believe investors should also start the process sooner rather than later. We believe that stocks will generally be higher than current levels 12-18 months from now. Therefore, we recommend that long-term investors with time horizons greater than 5 years, begin putting some of their excess cash to work as soon as possible. In the current market sell-off, we are concerned about slower earnings growth in the quarters ahead, but we believe that the market will likely look through those earnings once there are increasing signs that the world is getting COVID-19 under control.

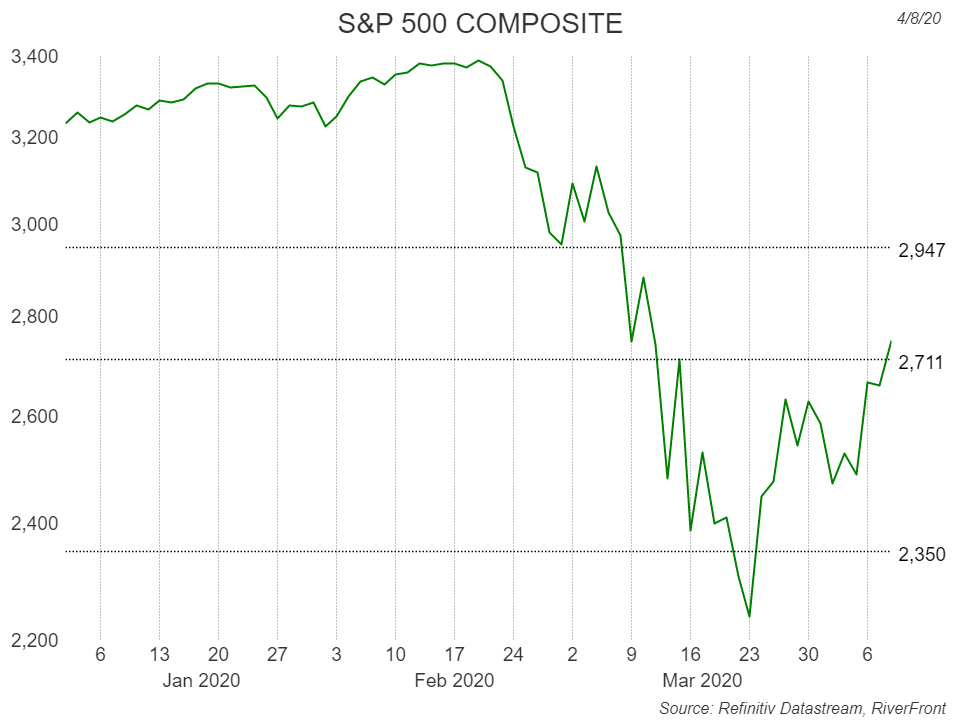

- Reinvest some Opportunistically: When merging onto the highway, gaps in the traffic will appear as you get up to speed. These gaps provide opportunities to merge more quickly. From a reinvestment perspective, investors can designate a portion of their cash to take advantage of opportunities that may arise as a result of market volatility. In fact, after more than a 20% bounce from the March 2020 lows, it would be surprising if we did not experience some pullback or digestion period in coming months. Should that occur, some investors may want to accelerate their purchases, taking advantage of that weakness. Even so, at or around the 2350 level on the S&P 500 might be an attractive opportunistic entry point. Others may want greater evidence that the COVID-19 crisis is behind us and therefore prefer to be opportunistic ‘on strength.’ We believe that the market may be putting virus fears behind it if the S&P 500 holds and eclipses important resistance levels like 2711 and 2947.

- Complete Gradually: Gradually the merger lane comes to an end, and the driver must complete the merge. Reinvestment windows also come to an end because investors risk missing out on the ‘power of compound interest’ if they fail to reinvest in a timely manner. To offset the risk of bad timing, investors can use a dollar-cost- average approach to gradually reinvest on a series of dates over a defined time period. Three to six months is probably the appropriate time period for a long-term investor to complete their cash reinvestment period, in our view.

Portfolio Implications:

RiverFront’s balanced portfolios are currently positioned slightly defensively as the portfolio’s equity weightings are 3-6% below their composite benchmarks. Our portfolio management teams continue to monitor COVID-19 developments and meet regularly to construct and implement de-risking and re-risking plans.

Download 04.13.2020 | Weekly View

Authored by

-

Doug Sandler CFA®

Vice Chairman