Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Quarterly Review: 2020 Ends Positive on A Positive Note

SUMMARY

- The year finished strong as investors look ahead to a 2021 recovery.

- Previously lagging sectors, such as Energy and Financials, were the best performers, we believe, due to growing expectations for a full re-opening of the economy.

- As the rotation towards recovery plays continues, we have increased our exposure to economically sensitive areas such as emerging markets.

Finished the year strong:

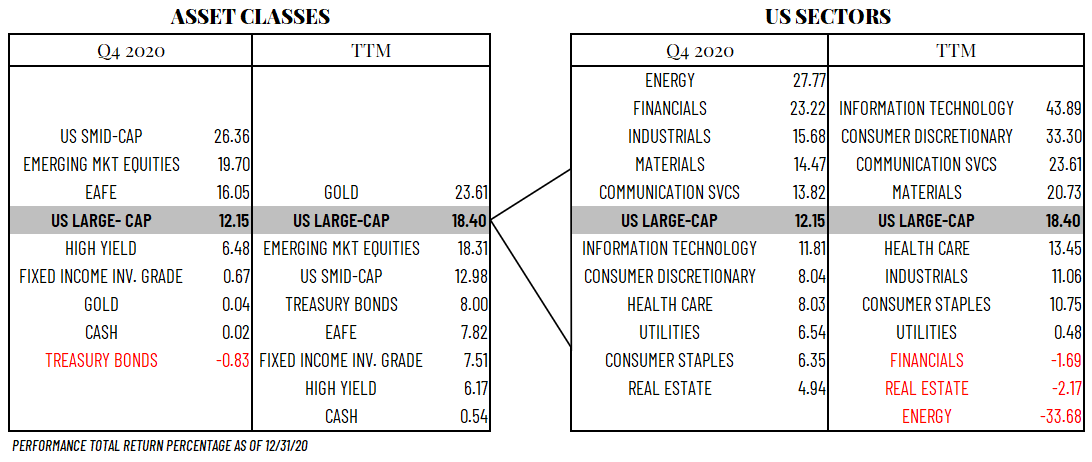

At the beginning of the fourth quarter, uncertainties surrounding the US elections, timing of vaccine approval, and above-average valuation levels left many investors questioning whether the rally off the March lows could be sustained. News of additional stimulus, improving economic metrics, and multiple vaccine approvals overshadowed those uncertainties. As a result, investors chose to focus on the road ahead rather than the rear-view mirror. Ultimately headlines gave way to recovering fundamentals, leading global equities higher. During Q4, the S&P 500 gained 12.15% and made a new high, but global equities also benefitted from regional economic turnarounds as Developed International equities rose 16.05% and Emerging Markets gained even more by increasing 19.70%. As the recovery theme gained traction, US small-cap equities were the best performing equity asset class compared to other major asset classes, rising 26.36% during the period. In a risk-on quarter, it isn’t surprising that fixed income instruments lagged equities. In the table below, the best performing fixed income asset class, Investment Grade Bonds, rose less than 1% in the fourth quarter.

The table below shows the performance of asset classes on the left and US equity sectors on the right. Returns for both the fourth quarter and the past 12 months (TTM) are shown. The table is anchored by US Large-Cap equities, which are shaded, and allows for easier comparison to see higher and lower relative performance by each asset classes and sector.

Performance: A Closer Look

The laggards became the leaders as investors shifted the focus from quarantine to reopening:

During the last quarter of the year, all eleven sectors in the S&P 500 turned in a positive performance. After the news of vaccine approvals came in November, those sectors and asset classes expected to benefit from the re-opening of the global economy were the strongest performers. Four of the five top-performing sectors during the quarter were cyclical segments of the market that lagged during the height of the pandemic shutdown. While still the worst performing sector over the past year, the Energy sector rose roughly 28% as reopening hopes fueled expectations for a resumption of oil demand. The second-best performing US sector, Financials, rose 23%. Rounding out the top five were Industrials, Materials, and Communications Services.

We are constructive on our outlook for 2021:

In RiverFront’s 2021 Outlook, the Base Case expectation for returns for the S&P 500 is a range of 8%-10%. At the time of this writing, our strategies remain overweight U.S. equities, but we continue to note the increasing attractiveness of international equities as well as their leverage to a falling dollar. Our Tactical Process guides our shorter horizon portfolio decisions. While our most recent analysis of the primary trend, as defined by the 200-day moving average for the S&P 500, is positive, the rate at which the trend is rising is unsustainable in our view. When combined with data suggesting extreme investor optimism, we would not be surprised to see the index move sideways or temporarily retrace some of those gains before moving higher.

We believe diversification and selection will be the keys to success this year:

As the rotation towards economically sensitive stocks continues, we have shifted some of our equity exposure to include a mix of what we believe to be stable earnings growers as well as cyclical stocks. As we move forward, a weaker dollar would likely cause us to continue shifting our strategies to be more levered to segments of the market that we think will benefit such as international equities. Within international, we believe emerging Asian economies will prove more resilient to COVID-19 and thus, have increased our exposure to emerging markets in our longer horizon portfolios.