Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

The NFL season is now underway, and after the first month of games, some teams have thrown in the towel and are playing for next year’s top draft pick. Others are ‘pretenders’ who win more often than they lose but will falter when times become difficult. Finally, the ‘contenders’ are executing their game plan flawlessly and preparing themselves each week with the goal of winning the Super Bowl. Currently, we view the US stock market as a ‘contender,’ as the weight of evidence from our three tactical rules has improved each quarter. Entering the fourth quarter, we believe the ‘three rules’ (as defined below) are further aided by a macroeconomic backdrop that consists of monetary easing, signs of trade resolution/ceasefire, and a strong US labor market.

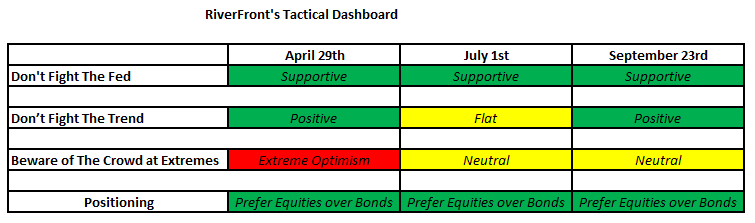

RiverFront’s three tactical rules of Don’t Fight the Fed, Don’t Fight the Trend, and Beware of the Crowd at Extremes have changed since our last update. Below you will find a summary chart highlighting changes in the three rules since our July 1st, Weekly View:

Don't Fight The Fed:

We believe investors should not go against the policy guidance of central bankers in the US or abroad.

The current policy stance in the US is ‘supportive’, in our view as the Fed has reduced interest rates by 25 basis points at each of its last two meetings. The rate cuts now have the fed funds target at between 1.75% and 2.00%. By lowering interest rates, the Fed has enticed homeowners to refinance their homes, which potentially increases disposable income as monthly mortgage payments decrease. Lower interest rates are also beneficial to corporations that have debt because it allows them to pay down debt faster, increase dividends, or reinvest. The impact of this low rate environment is apparent in the Chicago Fed’s National Financial Conditions Index, which now shows financial conditions close to the loosest they have been since 1971; indicating a willingness for financial institutions to lend to borrowers. Overseas, the European Central Bank (ECB) has restarted quantitative easing in Europe by printing €20 billion per month to stimulate their slowing economy (See our Weekly View from 9/16/19). The Bank of Japan (BOJ) has also committed to additional easing, which is expected to come in October. We believe global central banks are currently supportive and on the investor’s side.

Don’t Fight The Trend:

We believe investors should determine the direction and strength of the trend and adjust their investment decisions accordingly.

Currently the US primary trend, which we define as the S&P 500’s 200-day moving average (the average closing price of the S&P500 over the last 200 trading days), is rising at an annualized 11.3% rate. This is a significant improvement from the flat trend that we observed during our July 1st update. The strengthening trend is notable given the nagging backdrop of a trade war that has already resulted in several tariff increases. Currently, some signs of a cease-fire in US/China trade tensions have pushed the S&P 500 near an all-time high level. If trade negotiations deteriorate, we think the trend will likely weaken, but the strength of the trend makes it unlikely, in our view, that the S&P 500 would fall much below the current 200-day moving average of 2826 (as of 9/23).

The international primary trend, which we define as MSCI All Country World ex-US index’s (ACWX) 200-day moving average, is also strengthening. The international trend is rising at a lower 4.6% annualized rate but has less support than the S&P 500 and will turn down quickly if the improvement does not continue, in our view. Importantly, the international trend is more vulnerable to trade discussions and Brexit, in our view, which could go either way over the next three months.

Beware Of The Crowd Extremes:

Analyze sentiment by determining if it sustainable at current levels. If sentiment is identified to be unsustainable, then as investors we believe we must be willing to lean in the other direction and be prepared to act aggressively once the condition changes.

Ned Davis Research’s (NDR) Weekly Crowd Sentiment Poll (see chart below) currently sits right in the middle of neutral after reaching ‘extreme optimism’ in July and then falling slightly into ‘extreme pessimism’ in August. Sentiment is supported by a strong labor market, as unemployment sits at a low 3.7% and higher labor turnover (people quitting their jobs) indicates that employees are comfortable quitting their jobs before having found an alternative or have found new employment. Ultimately, when the labor market is strong there is a cascading affect through the rest of the economy, in our view. Given the strong labor backdrop, markets have been able to better weather negative headlines. For example, the S&P 500’s trading range has been contained to 2850 - 3027. We believe that sentiment going forward will continue to be driven by monetary policy decisions, global trade, and geopolitics.

The Final Verdict:

We believe the Fed and central banks around the world are signaling that they will do whatever is needed to continue the expansion. Central bankers’ willingness to aid the expansion creates a supportive backdrop for equity performance around the world. In the US, we view rising price trends and sentiment that is not overly optimistic as additional positives in the near-term. If our three tactical rules remain at current levels, we believe that the risk positioning in our portfolios is appropriate. If the trend improves, and the Fed and sentiment remain unchanged, we will look to add additional equity exposure to the portfolios.

Download 09.24.2019 | Weekly View

Authored by

-

Kevin Nicholson CFA®

Global Fixed Income CIO | Partner