Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

Housing is an Important Key to Economic Growth… Fortunately it is Getting Back on Track

SUMMARY

- The housing market is healthy, which we see as a tailwind for the economy and stock market.

- We believe favorable demographics, low interest rates, and increased workplace flexibility should keep the demand for homes high.

- RiverFront continues to favor equities over bonds and finds some housing-related stock themes attractive.

There are few things more important to the American psyche and the American economy than a healthy housing market. We believe a healthy housing market signifies consumer confidence, catalyzes economic growth, and creates high-paying jobs. Here is why:

- Consumer Confidence: In our view, a home purchase is the ultimate sign of consumer confidence. We believe homebuyers only buy homes when they feel that their job is secure, their prospects for the future are positive, their personal balance sheets are relatively strong, and banks are willing to lend.

- Catalyst: A home purchase is often an economic accelerator. The purchase of a home is typically followed by additional purchases such as furniture, floor coverings, home goods, and lawn and garden equipment.

- Creator: Home construction and home remodeling create jobs and can help bridge the income divide. According to the Bureau of Labor Statistics (BLS), there are roughly 7.4 million construction-related jobs in the US and many of these jobs are high-paying. As of January 2021, the average hourly rate for a construction worker is over $32, which equates to approximately $60,000 to $65,000 per year (assuming a 40-hour workweek). Wages can be higher in the fastest growing areas of the country and for the more skilled positions such as carpentry, electrical, project management, and equipment operation. This makes home construction one of the few industries where workers can earn an above average income without a college degree.

The Opportunity: Pent-up Demand for Homes

Over the long-term, the demand for housing is driven by factors including demographics (household formation), interest rates, the state of the economy, and other exogenous factors. The demand for homes has recently accelerated, and we believe that demand will remain strong for the foreseeable future for the following reasons.

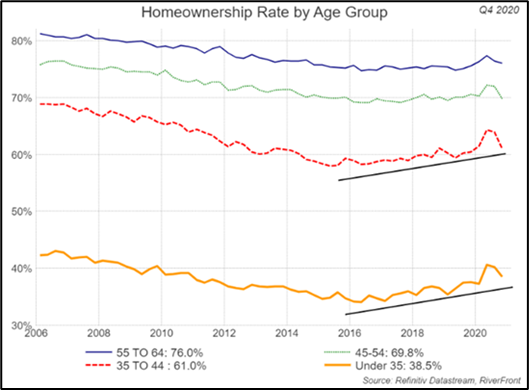

Demographics: A new generation of homebuyers is descending on the housing market in force: The Millennials. Nielsen Media Research defines Millennials as those born between 1981 and 1996, meaning they are somewhere between 24 and 40 years of age. From the chart on the right, one can see home ownership beginning to increase in the Under 35 category (bottom solid line) and the 35 to 44 category (dotted line). From this data it would appear that the Millennials are not permanent renters, but homebuyers that were delayed by high levels of student debt and the subsequent recession that followed the Financial Crisis. This may explain why home ownership has declined since 2005 from 69% to 66% (US Census Bureau). Interestingly, the generation following the Millennials (Gen Z) may be even more enthusiastic about home ownership than the Millennials. A recent poll by Freddie Mac found that 86% of those aged 14-23 intended to purchase a home someday. These positive demographics will cause homeownership levels to increase in coming years perhaps even eclipsing the 2005 highs, in our view.

Economy and Interest Rates: We believe that the economy and interest rates are supportive of continued housing strength. In our opinion, the economy can only get better from here as vaccines get distributed and businesses re-open. Interest rates also remain relatively low and although rates have risen recently, nationwide mortgage rates for a 30-year conforming mortgage are around 3 to 3.5%, well-below historical averages.

Exogenous Factors: With many people likely to continue to work from home, the desire to live in as nice an environment as possible will continue to grow well beyond COVID-19, supporting both housing demand and remodeling. Thus, while some of these exogenous factors like COVID-19 itself may fade, we believe that many will remain and create enduring demand for housing.

The Problem: Housing is in Short Supply

Today, there is only a 4-month supply of homes available, which is near the all-time lows in the late 1990s/early 2000s (right chart). This level of inventory is well below the long-term average of 6 months. Supply indicates how long current inventory would last if no new homes were built.

Currently there is a combination of decreased availability from existing homes and a lack of availability for new construction. According to Realtor.com, 2012-2019 experienced sustained levels of underbuilding leaving a gap of 3.84 million new homes.

A 2018 Freddie Mac report estimated that the demand for new homes in the US was approximately 1.6 million per year. This is comprised of about 300,000 homes to replace homes that have deteriorated, 1.1 million homes needed by new households, 100,000 as second homes and 120,000 to be in inventory.

Conclusion

The housing market can be an important precursor of future economic activity. Today, the US housing market is healthy. January new home sales were up 19% year/year (US Census Bureau), January existing home sales were up nearly 24% year/year (National Association of Realtors) and home prices were up 10% in 2020 (S&P CoreLogic Case-Shiller). We expect the housing market to remain healthy as demand remains strong and supply remains tight.

In our opinion, a healthy housing market is supportive of increased earnings, a stronger economy and higher stock prices. This is one of the reasons we currently favor stocks over bonds in our Advantage portfolios. Sectors and industries that we believe will benefit the most from housing strength include consumer discretionary, banking, engineering and construction, home improvement, and building materials.

Download 03.08.2021 | Weekly View

Authored by

-

Doug Sandler CFA®

Vice Chairman