Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- Housing boomed during the pandemic, but we believe prices have now peaked.

- We think a repeat of the 2008 house price bust is unlikely…

- …due to favorable supply demand conditions.

What a Difference a Year Makes

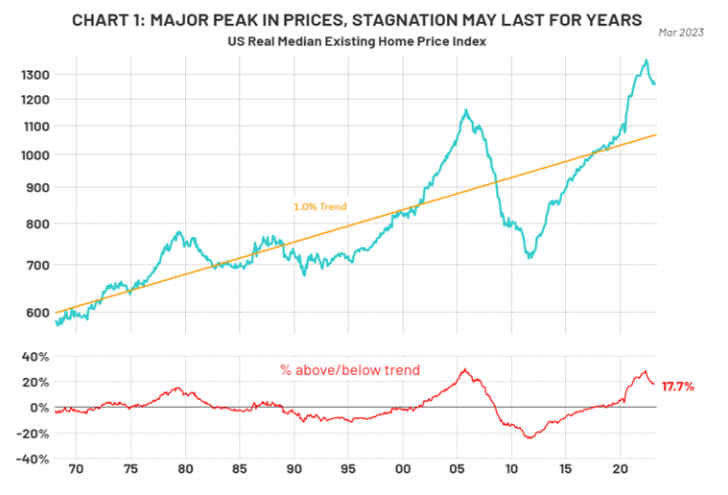

A year ago, we wrote about the housing market. At that time, it was still ‘hot’. House prices were close to record levels above their long-term trend (see Chart 1, below), and homes were selling above asking and getting snapped up in days. We suggested that the rise in interest rates would change that environment…and it has. We also said that a housing bust was unlikely, and we still hold that view. Our outlook is for prices to ‘rust’, i.e., go through a long period of stagnation, not ‘bust’ like they did in 2008/2009.

While house prices are greatly influenced by local supply demand issues, as Chart 1 below shows, house prices nationally rose to more than 20% above trend in 2022 driven, we believe, largely by the collapse of mortgage rates. They now seem to have peaked and started falling. This begs the question of whether they will follow the pattern of the 2007 to 2011 price collapse. We will outline the reasons why we think a major decline is unlikely this time.

Housing affordability measures US income and interest rates to determine if a median-income family could qualify for a mortgage on a median-priced home (see chart, next page). To interpret the indices, a value of 100 means that a family with the US median income has exactly enough to qualify for a traditional 30-year fixed-rate mortgage on a median-priced home. An index above 100 signifies that a family earning the median income has more than enough to qualify for a mortgage loan on a median-priced home, assuming a 20% down payment. Home buyers are being forced to scale back on the purchase price relative to a year ago due to higher interest rates increasing the overall monthly payments.

The combination of 'above trend' home prices and falling affordability might suggest…that prices could decline more rapidly, but there are some structural factors that we believe will support home prices.

Rust, not Bust: There is a Shortage of Supply

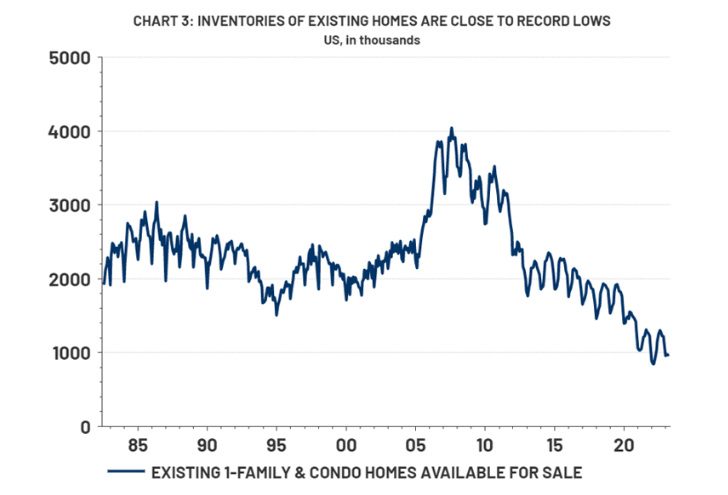

The first structural factor is a shortage of supply, especially for existing homes. Many homeowners refinanced their mortgages as rates fell to record low levels. This means they are unaffected by the rise in rates as long as they don’t sell. There are also fewer forced sellers, as low interest payments mean household debt service, as a percentage of disposable income, has fallen from a 40-year high of 18% in 2007 to a below average rate of 14.5% today. Chart three (right) shows the stark contrast between today’s housing supply and that which was available during the housing crisis. During the crisis there were 10-12 months of available supply of existing homes, today there is less than 3.

…And Millennials (The Boomers Kids) are Now Forming Households

The second structural factor that may lead to a ‘rust, not bust’ dynamic is on the demand side; the ‘millennial’ generation are now in their household formation years. The oldest millennials are turning 40 and the youngest are turning 26. According to the US Census Bureau there are 71 million millennials, and they make up 21% of the US population and 35% of the workforce. Millennials are getting married later but now household formation is picking up, providing a source of structural demand. Chart 4 (below) shows an acceleration in the pace of household formation since about 2017. This more closely reflects the pace when the millennials’ parents -the ‘baby boomers’- were forming households. As such, we expect it to last a long time. In addition, buyers are likely to spend more on homes and less on other things in our view, due to the pandemic’s shift to flexible schedules and the need for more space.

When you combine these factors, the likelihood of a sustained period of house price stagnation seems high, but a collapse in house prices seems unlikely.

Some Final Advice

Buying a home is more than a pure financial decision. Unlike a stock portfolio which is purely an investment, you get to live in your house and there are all kinds of intangible emotional factors involved in buying a home. Since we all need somewhere to live, the choices are buying or renting, and owning a home just feels different, in our view. Owning a home also allows you to add value to your home by improving it. The advantage of renting is flexibility, and a lack of repair costs but rents are also rising rapidly. Generally, the longer you plan to live in a home, the more advantageous it is to buy.

Given our views on home prices, we suggest the decision be based on personal preferences, not on the expectation of further significant price increases in the next few years. As our chart on page one shows, home prices only increase on a trend basis of 1% over inflation and have big price swings. This suggests that the main financial advantage of home ownership is the ‘forced savings’ process of increasing your ownership stake by paying off a mortgage over time.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.