Your choice regarding cookies: We use cookies when you use this Website. These may be 'session' cookies, meaning they delete themselves when you leave the Website, or 'persistent' cookies which do not delete themselves and help us recognize you when you return so we can provide a tailored service. However, you can block our usage by adjusting your browser settings to refuse cookies.

SUMMARY

- RiverFront places a high probability on a debt ceiling ‘solution’, whether an actual deal or a temporary suspension.

- Even in a US technical default, the Fed and Treasury have measures they can take to mitigate a lasting default scenario.

- Our risk management process allows us to be nimble with regard to portfolio construction, should our probabilities of default significantly deteriorate.

“It’s like déjà vu, all over again!”

baseball legend Yogi Berra

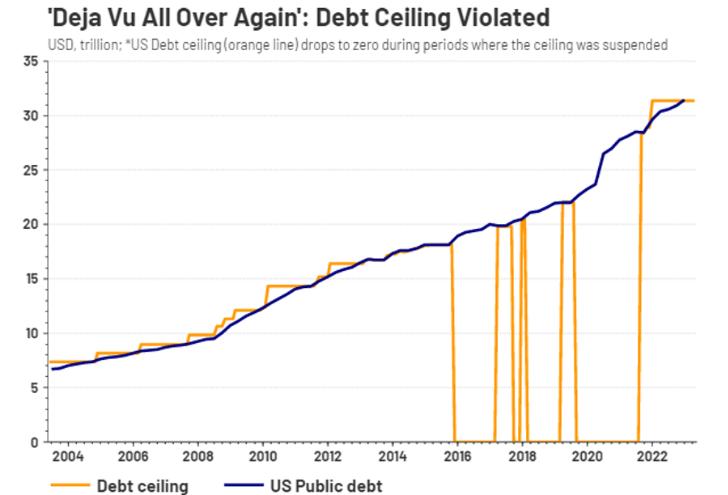

Americans find themselves at the precipice of another US government default, due to political disagreements around the self-imposed debt limit. If this scenario seems familiar, that’s probably because it’s happened before. A lot. According to the US Treasury, since 1960 Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the ‘debt ceiling,’ a limit imposed by Congress on the amount of debt that the U.S. Federal government can have outstanding. This includes seven extensions (i.e., ‘kicking the can’ to a later negotiation) during the Obama and Trump presidencies alone (see chart below, orange vertical lines). The most memorable recent debt ‘debacle’ was in 2011, when the impasse was resolved by raising the ceiling only 2 days before the ‘X-Date’ – the date the money runs out.

Highest Probability Outcome: Congress ‘Kicks the Can’ to a Later Date

Despite all this drama, the US has never actually failed lastingly to make principal or interest payments on its debt. In our view, the highest probability outcome this time is a ‘déjà vu’ scenario, with our policymakers once again either squeaking out a ceiling raise compromise in the 11th hour before the X-date (which Treasury officials have said is likely to be in early June) or a ‘kick the can’ temporary suspension of the ceiling until at least the fall. RiverFront’s investment team places a roughly 90% probability of a near-term ‘solution’, whether a temporary suspension of the ceiling or an actual deal.

At the end of day, we think politicians of all persuasions are in the self-preservation business, and for them there’s little upside to being branded as the policymakers who caused a delay in Social Security or Medicare payments or caused a rating agency to downgrade US debt on their watch… especially with a Presidential election cycle starting next year.

Public Negotiation 101: Prepare for Scare Tactics and Brinksmanship

In many ways, 2011 is a useful analog for today: both feature a Democratic President with a divided Congress, combined with an uncertain economic outlook and a cyclical bear market in stocks. In 2011, the issue was resolved by an 11th-hour compromise with a $2.1T increase in the ceiling. This increase was offset by more than $900B in deficit reduction measures with a mandate to find more savings in order to avoid sequestration (automatic spending cuts via the withdrawal of certain government programs).

But will this time be different? We believe US politics are more fractured today than in 2011. This slightly increases the probability of default, in our opinion, from tiny to merely low (<10%). The US economy is in a different place today as well, with inflation debt-to-GDP much higher than in ‘11…perhaps increasing the economic fallout in a default scenario, and potentially limiting the Fed’s ability to help offset it via lowering interest rates. However, some things don’t change…including tactics during a highly public political negotiation. These include scare tactics and brinksmanship, with supposed ‘hard lines’ drawn by both sides.

While debt ceiling negotiations are likely to remain heated right up until the 11th hour, it is important to recognize that this is a negotiation, and classic public negotiation tactics should be expected. We would expect both sides to take an extreme initial position, emphasize the 'sense of urgency', magnify the consequences of not getting their way and occasionally 'walk away from the table' to make a point. The intense spotlight also presents an opportunity for those at the political extremes to have a 'soapbox' for their own agendas, which may not be reflective of either party's negotiating objectives. While some statements regarding the state of the negotiations may be accurate, we also recognize the incentives and take these with a grain of salt.

To Think the Unthinkable: What Might Happen in a Default Scenario?

First, we'd like to discuss the type of technical default we'd likely experience in a country with the size and economic prowess of America, in comparison to the historical precedent of defaults in small, less productive emerging market countries. While a US technical default would be embarrassing and costly, we find it hard to believe that a country with the world’s largest economy and reserve currency will stay in technical default for very long.

But since US default has never happened before, it’s hard to say definitively what it would look like. Several things would likely happen in short order…none of them positive. This likely includes immediate credit downgrades, more tightening of liquidity and monetary conditions, leading to a much higher probability of an extended economic downturn. We would expect US dollar weakness along with elevated volatility in risk assets such as stocks. In 2011, the S&P 500 had a peak-to-trough drawdown of close to 20% before rebounding relatively quickly as a solution was reached. Interestingly, US government bond yields actually fell throughout this debacle, with 10-year Treasuries ironically assuming their classic flight-to-quality characteristics despite the ‘full faith and credit’ of the US government theoretically at risk. We think this episode speaks volumes about the differences between an emerging market default and what the US’s might look like.

Even in a technical default, the Treasury and Fed have some tools at their disposal to make sure foreign creditors, Social Security benefactors and others are not permanently impacted. For instance, according to a Wall Street Journal article, Fed Chair Jay Powell is on record back in 2013 suggesting that the Fed could buy back Treasuries at risk of default or allow banks to pledge defaulted Treasuries to the central bank to be made whole. There are other potential stop-gap measures, including possible Constitutional remedies, coin printing, delay of principal payments, and others. None of them are optimal, and some of them may have questionable legality. Treasury and Fed officials have been understandably vague about these, preferring a political solution to what in essence is a political problem.

Message of the Stock and Credit Markets Remain Constructive

Recent headlines have suggested some progress. Speaker of the House Kevin McCarthy managed to get a bill passed in the House that represents a concrete starting point for a counter by President Biden, who has cut his current trip to Asia short to focus on debt negotiations. If both parties can get close enough in principle to a compromise to agree to a temporary ceiling extension, a deal to raise the ceiling doesn’t have to be immediately signed. Such an extension, perhaps until fall or early 2024, would allow some breathing room for both sides to fine-tune and then ultimately present the final resolution as a ‘win’ to their constituency. Over the weekend, Biden and McCarthy talked via phone and struck an optimistic tone but still appear far apart, with talks in person resuming on Monday.

The stock and corporate bond markets have remained resolute in the face of this uncertainty, with relatively tight credit spreads and the S&P 500 trading near multi-month highs, well above the psychologically important 4,000 level. We believe this is due to a Fed on the brink of pausing rate hikes, solid employment and retail spending trends, and a Q1 earnings season that highlighted the resilience of the consumer and Corporate America’s pricing power. RiverFront’s investment team believes in the ‘message of markets’, and thus views market strength as one sign that the probability of debt ceiling-induced market dislocation is low.

Conclusions:

- RiverFront’s investment team places a high probability that the debt ceiling debacle will be averted at the last second, most likely with a temporary suspension to allow both sides longer to negotiate a more lasting solution.

- Even in a US ‘technical’ default, the Fed and Treasury have measures they can take to avoid a lasting default scenario. However, in any default situation, the US and global economies’ growth prospects will be damaged, in our view.

- Given the uncertain backdrop, RiverFront’s balanced portfolios are currently focused on security selection and yield generation, rather than making large allocation shifts relative to our policy benchmarks.

- Our investment team motto is ‘Process Over Prediction’; our process is to reassess our views as new information comes in and act accordingly, if necessary. Should our internal view of default risks increase significantly, our risk management process allows us to be nimble with regard to portfolio construction.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Download 05.23.2023 | Weekly View

Authored by

-

Chris Konstantinos CFA®

Managing Partner | Chief Investment Strategist